Andrew Austin the next Outsider

Kistos investment pitch

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

In this article, I will focus on Kistos, a company with a notable chairman and capital allocator, Andrew Austin. Initially, I came across this company through a pitch on the Value Investors Club and after conducting further research, I found the assets to be cheap and the management to be excellent. Austin had previously led Rockrose, an oil and gas investment vehicle that achieved an impressive 42x return in just 4.5 years. These factors encouraged me to make one of my first ever large investments.

Last year, during the European gas crisis, Kistos experienced a surge in sentiment, but the tide has since turned. The normalization of gas prices during a warm winter season has led to Kistos hitting a 52-week low recently. In addition, the company has been subjected to windfall taxes, non-renewal of their control over some gas fields in the Netherlands, and a lack of deals has further soured sentiment. Despite these challenges, Kistos managed to earn significant profits last year, and the company now has net cash to deploy. Therefore, I believe that it is a great time for investors to revisit and reassess the potential of Kistos.

It is important to note that I am not an expert in the Oil & Gas investment sector. Therefore, I strongly encourage readers to conduct their own valuation of Kistos' current asset base. Instead, this article will focus on what I believe is the company's true margin of safety - an exceptional management team led by Andrew Austin. I will provide a brief history of the two public entities led by Austin, namely Rockrose and Kistos. Then, I will apply the principle identified by William N. Thorndike in his book, "The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success," to Andrew Austin.

Rockrose & Kistos

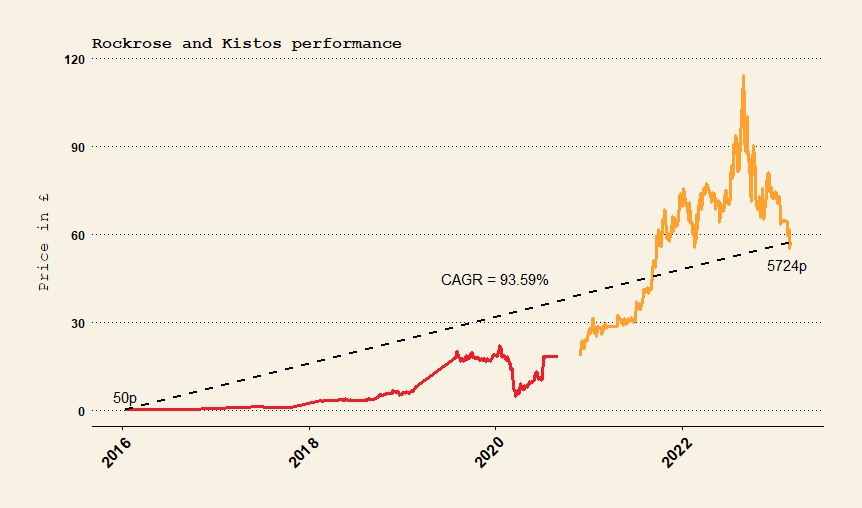

Andrew Austin and his team made their public market debut in January 2016 with the listing of RockRose Energy PLC for 50p on the AIM market in London. What unfolded in the next 4.5 years is one the most epic stunts in capital allocation history ever achieved. Rockrose stock was a 42 bagger in these short 4.5 years. Below the history of Rockrose is shown.

Rockrose was founded by Andrew Austin with the aim of acquiring and developing unloved and undervalued oil and gas assets in the North Sea. The company's name was inspired by the Rockrose plant, which is known for its ability to thrive in harsh environments with limited resources. During the covid pandemic with demand for oil & gas cratering Rockrose stock fell to £5, however, Andrew Austin still managed to sell the whole company for £18.50/share. This sale netted Andrew Austin £66m (pre-tax).

Kistos was listed as a SPAC just two months after the cash payment for Rockrose, to capitalize on the misallocations in the North Sea oil and gas sector. This quick listing was a record, according to Andrew Austin himself. It is evident that Austin is truly passionate about running oil and gas companies, despite having made enough money to live a comfortable life on a Greek island surrounded by real rockroses. Instead, he chose to take immediate action and listed a new company, Kistos, which is Greek for Rockrose. Kistos has delivered excellent returns so far, with the European gas crisis contributing to its success, but the windfall taxes and extremely warm winter have dampened its further rise. If an investor had participated in the IPOs of both Rockrose at 50p and Kistos and rolled over their proceeds, they would have enjoyed a near 120x return over seven years, or a 93% CAGR (not counting large special dividends).

How does Andrew Austin manage to achieve such excellent returns? I like the summary provide by Royal Dutch is the previously mentioned VIC write up (they refer to graph 1):

“There is a lot to study here. One can perhaps summarise it as AA being a much smaller, nimbler and shrewder operator, constantly picking off assets from counterparties with:

larger and lazier balance sheets,

older technology and seismic information, and / or

stale/no knowledge on the latest tax, environmental regulation, the shifting political landscape and the opportunities embedded therein.

Point of note (after a warm up period) is the acquisition at step 3. Firstly, he acquires a company by paying £8m and announces immediately thereafter a cash balance of $127m. Secondly, to exacerbate the absurdity of the situation further at step 5 we see him return £1.50/share taking everyone out at cost - and some at profit - as if it were a casual bridge loan that was required to acquire a $127m cash balance at a discount.

An attempt to explain it: he re-optimised abandonment and environmental liabilities that were kept too stringent and/or stale by the sellers in light of recent regulatory developments. Additional small cost/high IRR infill drilling would allow for these liabilities to be pushed backward and thus lowering their PVs. Also, regulation had changed, e.g. sometimes keeping an existing platform would have become a preferable outcome compared to fully removing it as say marine growth has embedded it ecologically, etcetera. The compounding of the above lead to significant value creation.

We asked him how he won the bidding process for Marathon Oil UK (step 9, at the time owned by US listed MRO) given it was a larger asset attracting more bidding attention. AA said he was not the highest bidder, but he was the only bidder to seriously take on the UK defined benefit pension obligations, which he sharpened his pencil on via consulting with local pension/insurance specialists. He sold the DBOs later for a profit.

There are more twists and turns in Rockrose that reflect positively on Kistos, but hopefully the above provides enough to illustrate the capital allocation skills, execution quality and focus on shareholder returns of AA.”

For my fellow energy tourist I will explain the accounting of what happened at step 3 (buying something for £8m and then reporting a cash balance of £127m) a little more as the abandonment/decommissioning liabilities are an important part of Andrew Austin's capital allocation. Warren Buffet had a float, John Malone figured out you can use debt to shield earnings from taxes and use EBITDA to do acquisitions. Andrew Austin has a superior knowledge of these decommissioning liabilities as a superior form of leverage compared to bank debt. Rockrose used almost no debt instead leveraging the company to these decommissioning liabilities.

Decommission liabilities are the estimated costs associated with permanently shutting down an oil or gas well, discounted to the present. These costs may be assigned to the operator of the field who is responsible for the actual capital expenditure needed to wind down the field, or to the local government if the field is self-operated.

If the remaining cash flows from the field's remaining life are not sufficient to cover the cost of decommissioning, a company will be required to post restricted cash as collateral. However, increasing the future cash flows of a field or decreasing the cost of decommissioning can unlock this restricted cash, as the future cash flows will then cover the decommissioning costs.

Here is a simple example: let's say you have an unloved late stage asset with the following properties:

The well will keep producing till 2026

Total Assets: £210

Estimated future cash flow: £110

Restricted cash: £100

Liabilities: £200

Cost of decommissioning: £200

Equity: £10

The value we might want to pay for this should be around the equity value of £10. However, now consider that after we take control of the asset, we re-evaluate the current operating strategy and decide to do some capex for an infill drilling campaign. This will extend the useful life of the asset and increase future cash flows by let's say £50m. By extending the useful life of the asset to 2031, this already decreases the value of the decommissioning liability on the balance sheet, as it is pushed back in time and hence discounted more. However, most models use 3% cost inflation in decommissioning and then discount the value back at around 4%, so this decrease is somewhat minimal at 1% per year. If we now also manage to change the decommissioning plan to keep the platform in place, because it is now embedded in marine biology, for example, this further reduces the cost. Down to let's say £150m. The asset now looks completely different after spending, for example, £20m on the infill drilling campaign.

The well will keep producing till 2031

Total Assets: £260

Estimated future cash flow: £160

Cash: £100

Restricted cash: £0

Liabilities: £170

Cost of decommissioning: £150

Cost of infill drilling: £20

Equity: £90

I hope this extreme example illustrates how attractive decommissioning liabilities are as an alternative form of leverage. The people who own these liabilities, such as the government or your operating partner in the field, are also incentivized to decrease the cost of the liability and increase the cash flows.

Your partner, along with you, wants to optimize the economic value of the well over time. Similarly, governments are interested in maximizing the earnings from wells, as they earn taxes on these operations. They just want to ensure compliance with decommissioning regulations, but they have no imperative for the cost to be high.

It's like your bank working together with you to refund you 50% of your loan and having the cash available for reinvestment directly.

There are many more interesting capital allocation decisions within Rockrose/Kistos, such as the recent purchase in the great Lagan area. The purchase amount had to be paid during the summer, but the effective date was the first of January. By the time Kistos had to pay for the deal, the cash built up inside the asset had already paid for a large part of the purchase price. It should be clear to any onlooker that Andrew Austin has a hyper-financialized mind and is extremely driven to create shareholder value.

Andrew Austin an true outsider

In his book, "The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success," William Thorndike analyzes the management and investment styles of eight exceptional CEOs who consistently delivered outstanding results for their companies and shareholders. Through his research, Thorndike extracted common lessons and qualities that set these CEOs apart from their peers. In this context, I will overlay these qualities on Andrew Austin, the CEO of Kistos, to see how he measures up against this group of exceptional leaders.

Let’s walk through the common qualities of these CEO’s as identified and described by William Thorndike and see if Andrew Austin shares these tendencies.

Always do the Math

“The outsider CEOs always started by asking what the return was. Every investment project generates a return, and the math is really just fifth-grade arithmetic, but these CEOs did it consistently, used conservative assumptions, and only went forward with projects that offered compelling returns.”

AA and his team pass the first easily. It is clear that they are great and underwriting the future returns of late stage assets in the North Sea. AA has stated in multiple interviews.

“We are not famous for overpaying”

It is clear to me they will only pull the trigger if they believe the return to be adequate, otherwise they will just return capital to shareholders.

The Denominator matters

“These CEOs shared an intense focus on maximizing value per share. To do this, they didn’t simply focus on the numerator, total company value, which can be grown by any number of means, including overpaying for acquisitions or funding internal capital projects that don’t make economic sense. They also focused intently on managing the denominator through the careful financing of investment projects and opportunistic share repurchases.”

Again AA passes this test with flying colors, he has used shares to do acquisition in the past and it has always been very value accretive on a per share basis. Due to his own high inside ownership and his fiduciary duty to his partners I think he is hyper focused on per share value. This is in sharp contrast to most oil & gas CEO who like growing the company at any cost. Mainly to make sure their own salary is secure and grows with the size of the operations. (hint hint Serica).

A feisty independence

“The outsider CEOs were master delegators, running highly decentralized organizations and pushing operating decisions down to the lowest, most local levels in their organizations. They did not, however, delegate capital allocation decisions. As Charlie Munger described it to me, their companies were “an odd blend of decentralized operations and highly centralized capital allocation,” and this mix of loose and tight, of delegation and hierarchy, proved to be a very powerful counter to the institutional imperative.”

Rockrose and now Kistos owned many minority stakes in fields where they were not the operator themselves. The companies are really just a small group in an office making smart decisions around capital expenditure in the O&G industry. It is clear they make smart decisions to help partners optimize the value of assets but day to day operations are not the main concern. Again another clear pass.

Charisma Is overrated

“The outsider CEOs were also distinctly unpromotional and spent considerably less time on investor relations than their peers. They did not offer earnings guidance or participate in Wall Street conferences. As a group, they were not extroverted or overly charismatic.”

I think this is the least important element of the checklist. For one I find both John Malone and Buffett extremely charismatic. I think Andrew would not stand out in the list though. From the interviews he has done he appears very likable and down to earth to me. A bit less polish then one would expect from a CEO maybe. For example in an interview with Malcolm Gladwell of Core Finance in September 2019 he showed up in a shirt that barely fitted and people were quick to point this out to him.

Both Rockrose & Kistos again conventional wisdom only publish reports only twice a year. So they are not big on reporting to Wall Street so they do fit inside that camp. The only thing they guide is next year daly production rate. This is expected of O&G companies and does not strike me as promotional in the least. So again a check.

A Crocodile-Like Temperament That Mixes Patience With Occasional Bold Action

“Armed with their return calculations, all (with the notable exception of John Malone, who was constantly buying cable companies in pursuit of scale) were willing to wait long periods of time (in the case of Dick Smith at General Cinema, an entire decade) for the right opportunity to emerge. Interestingly, as we’ve seen, this penchant for empiricism and analysis did not result in timidity. Just the opposite, actually: on the rare occasions when they found projects with compelling returns, they could act with boldness and blinding speed. Eachmade at least one acquisition or investment that equaled 25 percent or more of their firm’s enterprise value.”

We have not seen a very long period of in-action yet by AA, with people now expecting almost two deals a year from him. I think we are currently witnessing the long period without a deal from him. However, I think this is highlighted by William this is a positive. The gas prices peaked last year this means the most deals available last year were unattractive if gas prices fell sharply (and they did). Andrew did try to merge Kistos & Serica, this deal was attractive because Serica was extremely over capitalized and had a lot of cash on its balance sheet.

Unlocking this cash was valuable irrespective of the gas prices.

Doing big acquisition is the name of the game for AA with 25% acquisition being an almost yearly occurrence for AA. He also bought back 20% of the company at once in 2018. He is really not scared to make big moves. I think if the prices were right he would move to buy all of Shell or Exxon Mobil.

The consistent application of a rational, Analytical Approach to Decisions Large and Small.

“These executives were capital surgeons, consistently directing available capital toward the most efficient, highest-returning projects. Over long periods of time, this discipline had an enormous impact on shareholder value through the steady accretion of value-enhancing decisions and (equally important) the avoidance of value-destroying ones. This unorthodox mind-set, in itself, proved to be a substantial and sustainable competitive advantage for their companies.”

Although I believe this point to be a bit of a repeat of point 1, it again clearly applies. The team is laser focused on making rational large acquisitions and after that they are hyper focused on the detail of optimizing their output with the help of small projects like infill drilling. Clear check.

A Long-Term perspective

“Although frugal by nature, the outsider CEOs were also willing to invest in their businesses to build long-term value. To do this, they needed to ignore the quarterly earnings treadmill and tune out Wall Street analysts and the cacophony of cable shows like Squawk Box and Mad Money, with their relentless emphasis on short-term thinking.”

Although Andrew Austin sold Rockrose after only 4.5 years this was never his plan. He has always stated that the goal of the company is to deliver value to shareholders long term by growing the company and returning cash to shareholders not by flipping the company to someone else. The sell decision was really forced by the covid panic.

I think it is quite clear that Andrew Austin is focused on the actual value of the company and not on reported earnings. The company has always spent the money required to optimize assets and does not pull back because of market sentiment. The whole idea of Rockrose was to buy unloved assets and invest in them. So I think it is clear Andrew Austin passes this test with flying colors as well.

A Shared world view

William N. Thorndike also provides a great table called "A Shared Worldview" below, summarizing some of the behaviors of outsiders. I have added Andrew Austin to this table.

Let's quickly walk through the elements of the table as they apply to Andrew Austin:

First-time CEO

I gave Andrew Austin a check mark, even though in a fundamental sense, this is not true. Andrew Austin was also the CEO of Igas (which he also founded) before he started Rockrose. However, I believe this point is much more about the outsider not being hired gun CEOs before, and this certainly applies to Andrew Austin.

Dividends

Rockrose paid multiple special dividends. It’s important to note that the UK does not double tax dividends like most countries, and hence they are much less disadvantaged compared to other countries around the world. Andrew Austin has stated that Rockrose/Kistos is about generating cash return for shareholders, but he will do it how and when it is most optimal. So, we will not see a consistent dividend that will become untouchable and hurt capital allocation, like is often the case.

Buyback 30%+

Again, this is not completely true. However, during his Rockrose period, AA initiated two large buybacks - that of the B-shares and 20% of all shares in 2018. This does not add up to 30%+ yet. However, I believe that if AA's tenure was as long as that of most of the outsiders, he would easily buyback 30%+ of the share capital, hence the check

Acquisition 25%+ of market cap

This is the bread and butter of Andrew Austin and does not require much further discussion.

Decentralized organization structure

As stated earlier, Kistos and Rockrose do not operate the field in which they share an interest. Hence, headquarters does not interfere with operations much.

Wall street guidance

This I have also discussed before AA only guides production quotes on current assets on nothing else.

Idiosyncratic metric

This one is a bit more interesting then the other points. In the 2019 interim results the following note was added by the directors of Rockrose:

“The Directors are of the opinion that the following constitutes the Company’s key performance indicators:

▪ Revenue

▪ Lifting cost per barrel of oil

▪ Barrels of oil equivalent produced per day (boepd)

▪ Booked reserves

▪ Date and amount of decommissioning”

Clearly the last point is incredibly idiosyncratic compared to a normal oil & gas company, showing how laser focused the company is on optimizing these late stage assets.

Tax focus

Rockrose received money back from the UK government every year that Andrew Austin was in charge. So the man is incredibly good at untangling the complex web of investment allowances, subsidies for decommissioning, and tax loss carry forwards. In the Kistos period, he has not had as much ability to shield earnings from taxes. However, it is clear that Andrew Austin has an incredible tax focus.

Concluding remarks

I hope this article convinced you that Andrew Austin is atleast a contender to be an outsider and got some people a little interested in studying Kistos as a stock. I think Andrew Austin passes all the tests William N. Thorndike has put it in his book to consider someone an outsider. For further knowledge on Kistos I recommend people to read the initial write-up by Royal Dutch on VIC I mentioned before as well as some of the analysis by Carlos M on twitter. I also strongly recommend people to listen to some of the past interviews with Andrew Austin.

VIC article: https://valueinvestorsclub.com/idea/Kistos_PLC/3149318537#messages

Carlos M on twitter:

Interview with Andrew Austin:

I enjoyed your note, thanks for sharing it and Jon for highlighting it.

You may be interested in this podcast interview I did with AA last year.

https://open.spotify.com/episode/5znEsu4QsDqaFqBNgy2yYk

Interesting company. I'm really enjoying your write-ups Iggy. Keep them coming.