Decoding Success: Analyzing Smoak Capital's Investment Pitches

Unveiling the Strategies Behind Smoak Capital's 5 year 48% CAGR

Introducing Daniel Smoak

In my journey to become a better investor, I enjoy studying the strategies of greats like Buffett and Greenblatt, among others. However, their management of much larger pools of capital has narrowed their investable universe and muted their returns. While delving into their past is essential for those managing smaller (private) funds, I believe it's equally important to examine practitioners currently succeeding with smaller capital pools.

One such individual is Daniel Smoak (@Dsmoak98), the founder of Smoak Capital. Daniel has achieved remarkably impressive returns. Since its inception on 7/1/18 until 6/30/23, Smoak Capital has generated a return of 612%, annualizing to 48%! If this isn’t reason enough to study someone's investment approach, Daniel has also publicly shared numerous pitches, making it easier to understand the mindset of such an incredibly skilled capital allocator.

In today's post, I delve into the past pitches and ideas shared by Daniel in his letters or other mediums to extract valuable insights. My focus is on summarizing his pitches, deciphering the rationale behind Daniel's choices of companies, and revisiting these pitches with the latest financial and stock price developments. Finally, I conclude with a comprehensive analysis, synthesizing the gathered information and tying together the key takeaways from Daniel's investment approach.

From my research, I have identified 16 unique ideas shared by Daniel that we can analyze

Table of contents

-Hemacare (OTC:HEMA)(2017 - pitch)

-Heritage Global (OTC:HGBL) (2018 - pitch)

-Xpel (TSXV:DAP.U/OTC:XPLT)(2018 - letter)

-LGL Group (NYSE:LGL)(2019 - letter)

-Tornado Global Hydrovacs (TSXV:TGH.V)(2019 - letter)

-Nocopi Technologies (OTC:NNUP)(2020 - letter)

-Collector’s Universe (NASDAQ:CLCT)(2020- letter)

-Dusk (ASX:DSK) (2021 - pitch)

-FitLife Brands (OTC:FTLF)(2021 - pitch)

-Azeus Systems Holdings (SGX:BBW)(2021 - letter)

-Four Corners Inc. (OTC:FCNE)(2021 - letter)

-ECIP Banks (Citizens Bancshares (OTC:CZBS), M&F Bancorp (OTC:MFBP), and others)(2022- letter)

-Cryosite (ASX:CTE)(2022 pitch)

-Medical Facilities Corp. (TSX:DR)(2023-letter)

-Hammond Manufacturing (TSX:HMM.A)(2023 - letter)

-Goodheart-Willcox (OTC:GWOX) (2023 - letter)

-Tying it all togetherNote: For the stock price and valuation, I mostly use the price for January of the next year for pitches from annual letters or from the next month if they were full-length pitches. This likely underestimates Daniel's returns, given he likely bought most of the stock well before pitching the public on them. Hence, the return you see is more akin to what you would experience by blindly copying Daniel. This is further amplified by the fact that we do not know when he sold; hence, I consider the full trajectory of the companies after his pitch. Daniel holding periods are likely shorter and his returns greater than shown in this article.

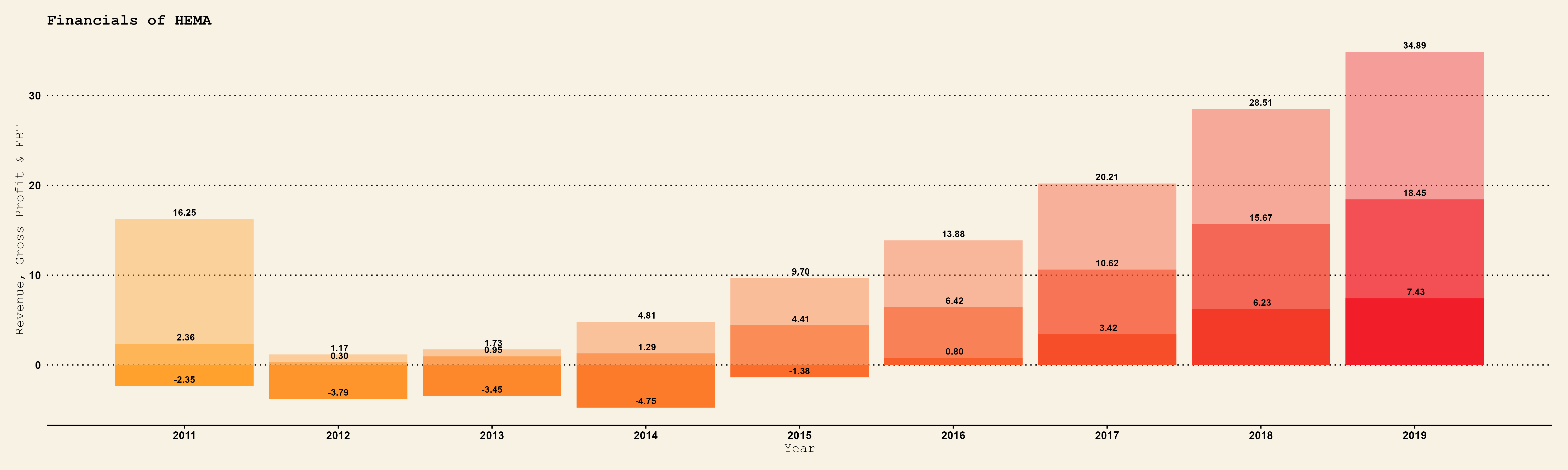

Hemacare (OTC:HEMA)

Full length pitch form 2017

Valuation at time of the pitch:

Stock Price: $1

Market Cap: $11.7M

P/E: N/A

P/S: ~1.4

Pitch Summary

HemaCare, a blood products and services company, underwent significant changes under new management since 2013. They refocused their business to cater to biotech companies and research organizations, shedding less promising aspects of their operations and concentrating on their bioresearch products division. Although this division was still incurring losses, it was experiencing rapid growth.

Daniel highlighted that HemaCare holds a unique position in the market, offering comprehensive support for process development, clinical trials, and commercialization - a capability unmatched by competitors. Moreover, he pointed out the favorable industry trends driving the growth of the bioresearch segment.

With a strong balance sheet and nearing profitability, Daniel emphasized the substantial upside potential for HemaCare if it sustains its growth trajectory.

What happened next

As Daniel emphasized in his pitch, if HemaCare sustained its impressive growth, there would be substantial upside. Indeed, the company experienced rapid growth and an inflection toward profitability throughout the full year of 2017. The market took notice, and by mid-2018, the stock had already increased tenfold. However, this wasn't the end of the story; HemaCare continued to grow, and the market substantially rerated the business.

At the time of Daniel's pitch, the company traded at 1.4 times price to sales, a valuation metric that the market quickly began to rate higher over the following year. The final chapter to this success story is that HemaCare was acquired by Charles River Laboratories International, a pharmaceutical company, for $380 million in cash. This acquisition equated to a valuation of approximately 10 times sales and a price-earnings ratio of over 50.

The incredible combination of growth and market rerating would have delivered a remarkable 26x return for those who followed Daniel into this investment. Over the short period from Daniel's initial pitch at the start of 2017 until the buyout at the end of 2019, this equated to a CAGR of over 200%.

My Learnings

The success story of HemaCare is indeed impressive and can feel daunting. Daniel's accuracy in identifying key aspects of the pitch, such as the company's path to profitability, its business quality, sustained growth, and subsequent stock rerating, highlights powerful engines for shareholder value creation. However, uncovering such opportunities requires diligence.

Daniel sheds light on why HemaCare's transformation remained undiscovered for so long. The company had been a "dark stock" for five years at the time of his pitch, meaning it didn't report to either the SEC or OTC. Additionally, being relatively small, HemaCare wasn't considered worthwhile for most investors to study.

When I encounter a small company with impressive growth potential that has yet to enter the discovery cycle, I make sure to conduct a much deeper analysis.

Heritage Global (OTC:HGBL)

Pitched in end of year 2018 letter

Valuation at time of the pitch:

Stock Price: 0.46

Market Cap: $13.7M

P/E: 4(trailing 9 months) 3.1(estimated 2018)

Pitch Summary

Daniel presented Heritage Global, an asset liquidation service company, as significantly undervalued compared to its true worth. He attributed this undervaluation to the company's unconventional history and lackluster recent performance. However, Daniel highlighted that the company had shown consistent growth, with particularly impressive results in the two quarters leading up to the pitch results that had gone largely unnoticed by the market.

Heritage also benefited from being led by two industry experts, the Dove brothers, who assumed management in 2015 and steadily improved the business while increasing their own stake from 16% to 40%

Despite the inherent variability in revenues within their industry, Daniel pointed out that the current trends were highly favorable. Heritage Global had generated approximately $3.3 million in earnings for the first nine months of 2018, with management expecting this strong performance to persist. Remarkably, this meant the company was trading at only 3-4 times its potential earnings for 2018, indicating substantial upside potential.

What happened next

Once again, Daniel was spot-on in identifying a undervalued company with a much brighter future than its past. With earnings before taxes (EBT) amounting to $3.85 million in 2018, aligning precisely with Daniel's forecast of a price-earning ratio of 3-4, the company began to chart an impressive trajectory. As Heritage Global continued to deliver robust results in 2019, the stock underwent a significant rerating, doubling in value over the course of the year.

The real breakthrough occurred in 2020, when the company's performance surpassed expectations, driving the stock to unprecedented heights that have yet to be surpassed. Whether or not Daniel exited his position, his initial investment would have yielded a remarkable return, potentially reaching a notable 6x.

What's particularly noteworthy from this pitch is the remarkable undervaluation of the stock relative to its future earnings potential. At the time of Daniel's pitch, the market cap was just under $14 million. However, from 2019 to 2021, Heritage Global earned a total of $16.4 million before taxes—exceeding its market cap in just four years.

Furthermore, recent years have seen even more impressive results, with Heritage Global earning nearly the entirety of its 2018 market cap in both 2022 and 2023. This underscores the remarkable growth trajectory and potential that Daniel had astutely identified in his pitch.

My Learnings

In hindsight, Heritage appears to have been a no-compromise investment. It was remarkably inexpensive based on earnings, benefited from the ownership and operational leadership of two proven industry experts—the Dove brothers—resulting in significant shareholder alignment, and consistently improved under their guidance.

Once more, the transformation of Heritage was well underway, yet largely overlooked by the market. I believe that analyzing changes in CEO or control, alongside subsequent improvements in the business, should indeed play a more significant role in my investment analysis moving forward.

Xpel (TSXV:DAP.U/OTC:XPLT)

Pitched in end of year 2018 letter

Valuation at time of the pitch:

Stock price: 5.4

Market Cap: 149

P/E: 17

P/S: 1.6

Pitch Summary

Xpel is a manufacturer and distributor of paint protection film(PPF), window tint film, and other related products primarily for the auto market. Xpel is one of a few leading players in the PPF market and has developed a competitive advantage by forming close relationships with installers with top-notch training programs, superior pattern cutting software, and helping installers win business through online leads or marketing materials/promotional work for their install shop. Xpel has a stellar management team who understands the global PPF market very well and are heavily invested in the company alongside shareholders. Management has grown the value of the company at an impressive rate of the past 5-10 years and Daniel believe growth will likely continue. He believe Xpel’s stock is undervalued relative to how high quality of a business it is and their future growth prospects.

What happened next

As Daniel predicted, growth did continues at Xpel and how… Revenues from the end of 2018 till 2023 quadrupled. This also led to margin expansion form 10 to 15%. Xpel returned 8.5x since Daniel pitch this mean that actually most of the return came just form the growth and improvement in bottom line, with rerating playing a much smaller role.

This is also due to a recent drop in stock price after a Q3 earnings miss and increased worry for part of the investor base about exposure the Tesla, which has hinted at wanting to inhouse a similar technology.

My Learnings

Daniel's investment in Xpel exemplifies a masterclass in assessing both the quality of a business and the extent of its growth runway. What's particularly insightful is that while Heritage's margin of safety lay in its low earnings multiple, Xpel traded at a price-earnings ratio of 17x around the time of Daniel's pitch. This demonstrates Daniel's adaptability and willingness to overlook a deep value multiple if he perceives a company to possess exceptional quality and substantial growth potential.

In hindsight, even a price-earnings ratio of 17x for Xpel appears cheap, given its current earnings compared to the market cap at the time of the pitch, resulting in a meager price-earnings ratio of 2. This underscores just how undervalued the company was back then, provided one understood its trajectory.

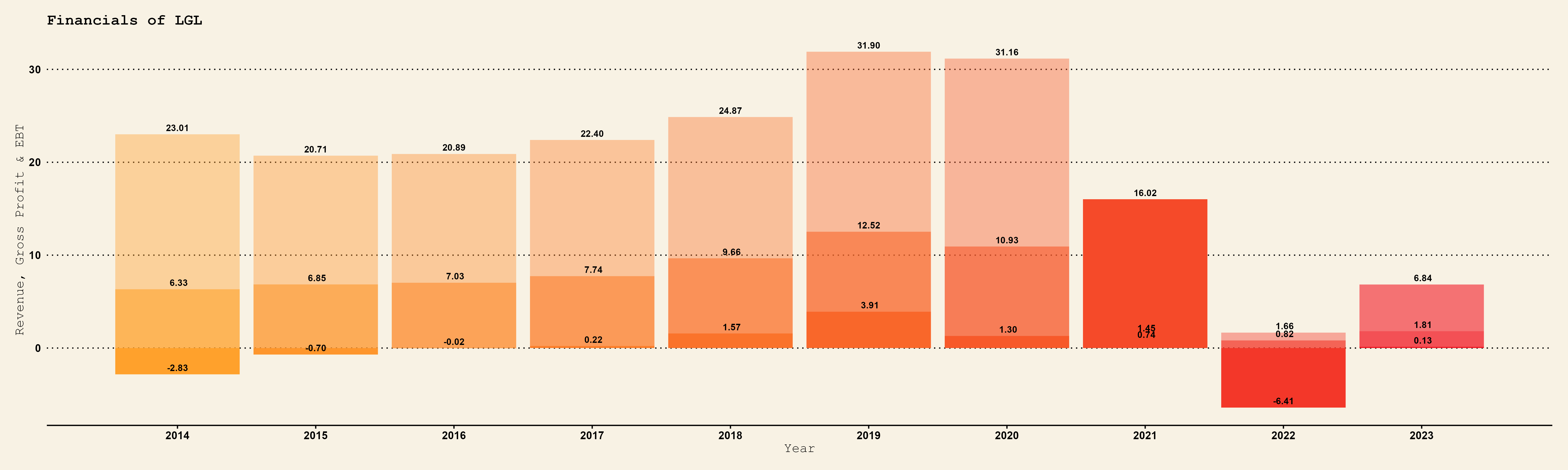

LGL Group (NYSE:LGL)

Pitched in year end letter 2019

Valuation at time of the pitch:

Stock price: 14.75

Market Cap: 76.8m

P/E: 11.82 (but less than 10x Daniel’s estimated earnings)

P/S: 2.5

Pitch Summary

LGL Group specializes in supplying precision-grade instruments to the aerospace and defense sector. A significant event preceding Daniel's pitch was the emergence of a sophisticated investor who became a major shareholder a few years earlier. This investor facilitated the appointment of a new management team, redirecting the company's focus towards the aerospace and defense business, while moving away from its previous ventures in non-defense electronics for internet communications. Since this strategic shift, the company has maintained modest growth and profitability.

Recently, there has been a notable uptick in both the pace and scale of customer orders, signaling a promising outlook for the next few years. Additionally, LGL Group boasts a robust balance sheet. Remarkably, the stock is currently trading at less than 10 times Daniel's estimate of 2020 earnings, indicating substantial potential for growth.

What happened next

At first glance, this investment might appear to be the first clear miss in Daniel's history of public pitches. However, upon closer inspection, this isn't the case. Keen-eyed readers will have already noticed the significant decline in both financial performance and stock prices, which seems unnatural even for a business in decline. And they would be correct, as LGL spun off part of its business in order to unlock shareholder value.

The spun-off company, M-tron Industries, saw its stock more than triple after the spin-off. The combined market cap of the two companies is $146 million, roughly double the value of LGL when Daniel pitched it.

Interestingly, Daniel's estimated 10x 2020 earnings did turn out to be a real miss, with LGL reporting numbers for 2020 that were much worse than expected. This also didn’t help the stock prices, which started tanking during the pandemic. I am not sure if Daniel held onto the stock after it failed to meet his expectations, but it shows that smart management/mayor shareholders can always unlock shareholder value with the right capital allocation.

My Learnings

Although Daniel may not have enjoyed the full ride on this stock, it demonstrates that his analysis was spot-on regarding the key factors driving its success. Particularly, the involvement of a savvy major shareholder poised to unlock the inherent value in the business played a pivotal role.

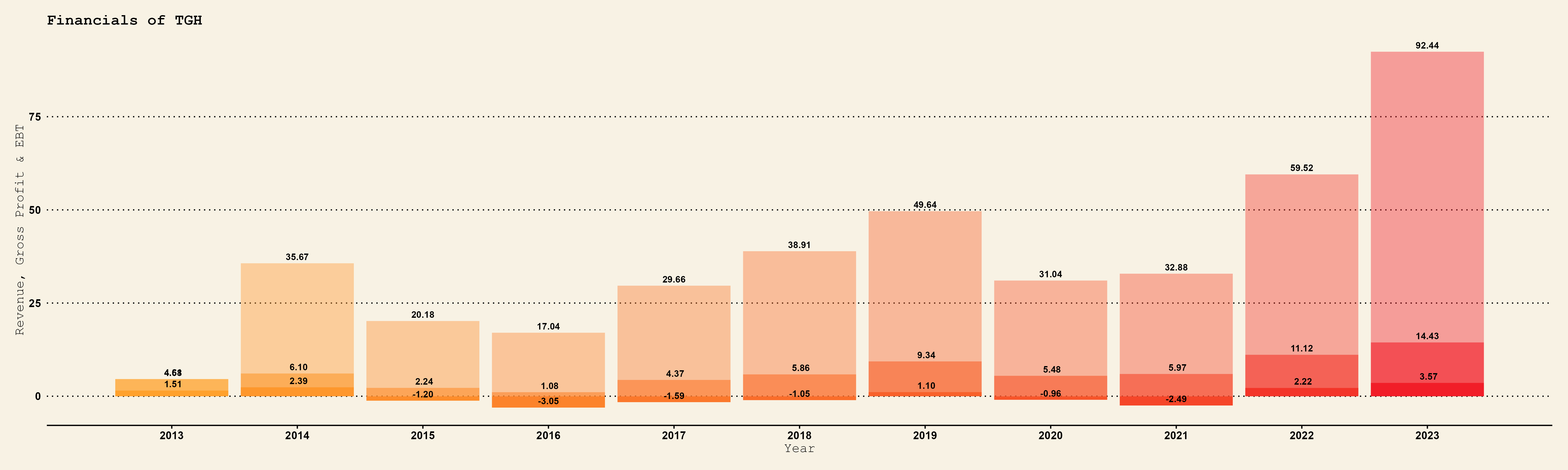

Tornado Global Hydrovacs (TSXV:TGH.V)

Pitched in year end 2019 letter

Valuation at time of the pitch:

Stock price: 0.20

Market Cap: 25.35 (canadian)

P/E: N/A

P/S: 0.41

Pitch Summary

Tornado Global Hydrovacs specializes in manufacturing hydro vacuum trucks catering to commercial, municipal excavation, and oil & gas markets. Historically reliant on sales to oil & gas customers in Western Canada, the company underwent strategic initiatives around the time of the pitch. These initiatives aimed to promote safe utility digging practices and incentivize operators to prioritize efficiency in time and cost.

As a result, there had been a notable shift in adoption within the excavation market, signaling potential growth opportunities, according to Daniel. If the strong growth trend continued, driven by increasing demand from their commercial and municipal customer base, Tornado Global Hydrovacs stood to experience considerable revenue and earnings growth.

What happened next

The pandemic dealt a severe blow to Tornado shortly after Daniel's pitch, with a significant decline in both top and bottom lines, leading to a halving of the stock price. However, starting in 2021, as the worst fears of the pandemic subsided and the market regained momentum, the stock began to recover.

Daniel's thesis was largely vindicated in the last two years following the pandemic. Revenues and bottom line both saw growth in 2022 and 2023 compared to pre-COVID levels. Revenues nearly doubled, and with some operating leverage, net income tripled during this period.

My Learnings

Once again, it's difficult to ascertain whether Daniel remained in this position as the pandemic struck and other opportunities arose. However, this pitch vividly demonstrates that if your analysis proves correct in the medium to long term, volatility can indeed work in your favor.

Moreover, this pitch serves as another testament to Daniel's exceptional ability to identify when a company's future prospects outshine its past performance, and the substantial rewards that can be reaped from such insights.

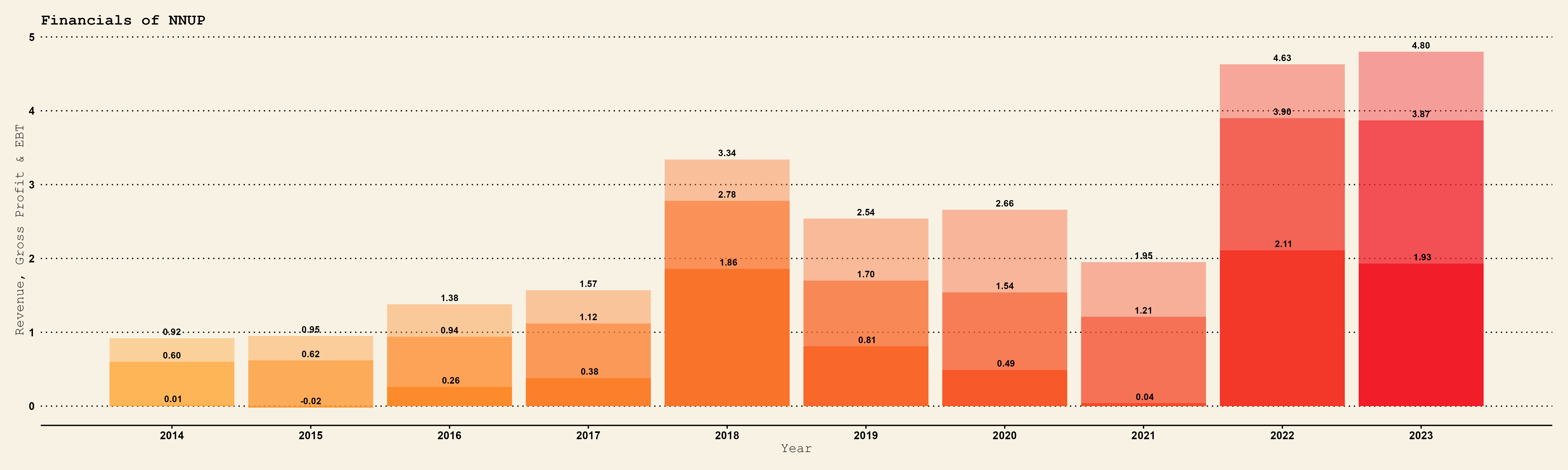

Nocopi Technologies (OTC:NNUP)

Pitched in year end 2020 letter

Valuation at time of the pitch:

Stock price: 1.49

Market Cap: 10.04m

P/E: 8

P/S: 2.21

Pitch Summary

Nocopi Technologies is a niche manufacturer specializing in specialty inks, primarily for the emerging segment of children’s coloring books. Its largest customer, Bendon Publishing, licenses Nocopi’s innovative 'mess-free' ink technology, paying royalties based on sales of their 'Imagine Ink' branded books, while also purchasing ink directly from Nocopi. Both revenue streams boast high margins, with royalties exceeding 80% and specialty inks around 65%.

Bendon’s 'Imagine Ink' product line has seen impressive growth, likely exceeding 30% annually, and enjoys widespread adoption through retail giants like Wal-Mart. Additionally, Bendon secures licenses from leading children’s brands such as Disney, Marvel, and Nickelodeon. In essence, Nocopi holds crucial intellectual property for one of the top products in a rapidly expanding consumer category. Despite significant customer concentration with Bendon, Daniel asserted that Nocopi maintains a strong negotiating position due to its superior technology and patent protections.

Daniel noted Nocopi’s prudent financial management and strong cash generation, coupled with a debt-free balance sheet and favorable long-term licensing agreements. He believed there were multiple levers available for further growth. Remarkably, at the time of the pitch, the stock was trading at only 5-6 times Daniel's estimated Free Cash Flow, underscoring its attractive valuation.

What happened next

Nocopi had a relatively lackluster performance in 2021, which resulted in the share price remaining relatively flat for the first two years after the pitch. However, Daniel's prediction of continued growth and strong margins due to Nocopi's bargaining power has become increasingly evident more recently. Once again, much-improved business results have been observed for one of Daniel's companies.

My Learnings

I think my learnings here are similar to those for Tornado: if your insight are correct in term of quality and improved future prospect, short term volatility should not bother the well-informed investor.

Collector’s Universe (NASDAQ:CLCT)

Pitched in tear end 2020 letter

Valuation at time of the pitch:

Stock price: 76

Market Cap: 691

P/E: 12

P/S: 7.6

Pitch Summary

Collector’s Universe specializes in grading and authenticating trading cards, collectible coins, autographs, and other memorabilia. Particularly, its trading card grading division, PSA, experienced a remarkable surge in demand throughout 2020, driven by the accelerated growth of the trading card market during the pandemic. With a decades-long reputation as the largest and most respected grading company in the industry, PSA enjoys significant pricing power and sustained demand, evidenced by a continuously growing backlog.

Despite the stock's nearly 300% surge in 2020, preliminary results from the latest quarter show a 70% year-over-year increase in revenue and operating income of $15 million. This may suggest that the stock is still undervalued, trading at just 12 times operating income.

The heightened demand in the trading card market has attracted attention from various businesses and investors, including a group led by the owner of the NY Mets. This group reached an agreement with Collector’s Universe’s board and management to take the company private at a price that many investors, including Daniel, deemed unfair to shareholders. The initial offer was rejected by shareholders on 1/19/21, prompting an increase of 22% in the offer. Daniel believed that the company was worth easily more than $100 a share and hoped that other shareholders would also be willing to fight for fair value.

What happened next

Very little happened after Daniel's pitch, and the buying party made one more offer at $92 a share, which was ultimately accepted. Therefore, Daniel didn’t achieve his target of above $100 per share. However, there are certainly worse outcomes than making a very quick 20% return on your investment.

My Learnings

Given that this pitch didn't fully play out, it's challenging to draw extensive lessons from it. However, Daniel's insight regarding the substantial potential remaining in this investment was certainly accurate, and he was at least rewarded for his assessment, even if it was not to the fullest extent.

Dusk (ASX:DSK)

Full length pitch February 2021

Valuation at time of the pitch:

Stock price: 2.62

Market Cap: 163

P/E: 9.26

P/S: 1.37

Pitch Summary

Dusk is a vertically-integrated home fragrance specialty retailer based in Australia, currently trading at a deep value price of only 3-4 times EV/EBIT. Despite this undervaluation, the company offers significant potential for growth, boasting a proven business model, strong management, and a positive organizational culture. Additionally, Dusk demonstrates very attractive unit economics.

Daniel believes that the timing of the IPO, limited financial data availability on financial platforms, and relative lack of investor attention have contributed to the mispricing of Dusk's stock.

While selling candles and diffusers may not initially seem like a lucrative business, Dusk's impressive economics and operational execution since the business was reorganized in 2015 speak for themselves. The company has achieved a multi-year track record of steady like-for-like store sales growth, with a compound annual growth rate (CAGR) of approximately 9-10% since 2017. Dusk also boasts a loyal and expanding customer base, with over 56% of revenues derived from paying loyalty program members, which have grown at a CAGR of 16% from FY18-20. Furthermore, the company is seeing expanding operating margins and free cash flow.

What happened next

This marks the first clear loser among all of Daniel’s pitches. While he understood that he was buying into peak earnings due to the demand surge for Dusk's home-centered products during the COVID lockdowns, he believed the market was overestimating how much Dusk's demand would drop post-pandemic. However, despite demand staying higher than expected post-pandemic, labor inflation ate up most of Dusk’s profits.

Despite achieving 30% more revenue, Dusk managed to generate less profit in the last twelve months than in fiscal year 2021. Furthermore, the business that appeared poised for growth also failed to expand in the post-pandemic normalization period. Therefore, for once, Daniel missed the short-term future of a company, resulting in his first outright money-losing pitch.

My Learnings

I believe this pitch exemplifies the difficulty in accurately estimating where a company, that is realistically facing decline, will end up. To truly extract value from a declining company, management must be extremely shrewd at managing costs and maximizing returns on capital where possible. Perhaps, it is indeed better to focus on improving businesses rather than trying to navigate the complexities of declining ones.

FitLife Brands (OTC:FTLF)

Full length pitch September 2021

Valuation at time of the pitch:

Stock price: 47.5

Market Cap: 59.2

P/E: 5.82

P/S: 2.14

Pitch Summary

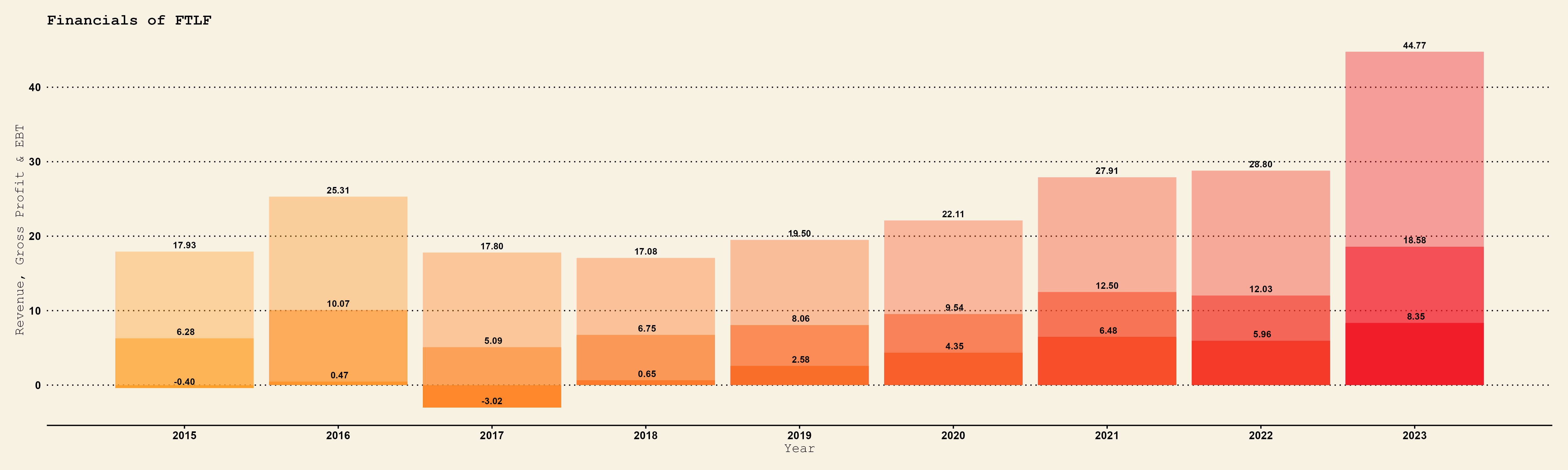

FitLife, a nutritional supplements company, underwent a dramatic turnaround from the brink of bankruptcy with a market cap of just $2.5 million at the end of 2017 to achieving nearly triple that amount in annual free cash flow by September 2021. Led by CEO Dayton Judd, the management team orchestrated an impressive revival, delivering substantial shareholder value through strategic cost reductions, a focus on core high-margin products, the development of a thriving e-commerce channel, and astute capital allocation decisions.

Despite the stock witnessing a staggering 20-fold increase since its near-bankruptcy phase, Daniel remains bullish on FitLife's prospects, believing that the business is currently performing stronger than ever. He asserts that FitLife is easily worth 10-12 times its estimated 2021 free cash flow, representing a potential upside of 40-65%. Moreover, Daniel highlights that the existing business trades at a significant discount, with an enterprise value to expected free cash flow ratio of just 7x, despite the presence of a proven management team with exceptional capital allocation skills.

This management team successfully transformed a $2.5 million company into one valued at $50 million in just 3.5 years, boasting a cash reserve exceeding $8 million, zero debt, and an annual free cash flow of $7-8 million, all contributing to further building shareholder value.

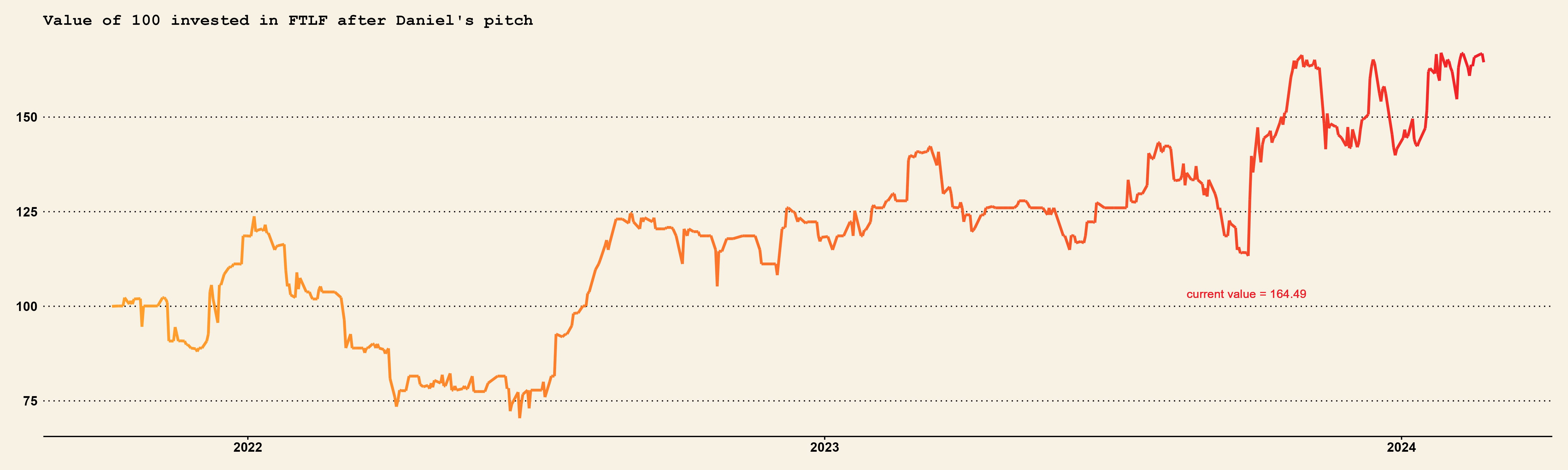

What happened next

FitLife experienced a successful full year in 2021, but like many stocks, it was not immune to the general market drawdown of 2022. Subsequently, there was a slowdown in growth, which dampened profitability for the company in 2022. However, by mid-2023, the stock had rebounded, recording a 25% increase.

As results continued to improve, the share price followed suit. Currently, the stock is trading at approximately 12.5 times earnings before taxes (EBT), roughly in line with Daniel's estimated value for the company.

Given the exceptional execution of the management team and FitLife's impressive returns on equity, there's a possibility that the stock is still undervalued at its current price.

My Learnings

I believe Fitlife is another exemplary case of possessing a long-term vision for the company's trajectory, bolstered by excellent management execution.

Azeus Systems Holdings (SGX:BBW)

Pitched in the year end 2021 letter

Valuation at time of the pitch:

Stock price: 7.9

Market Cap: 237

P/E: 112

P/S: 8

Pitch Summary

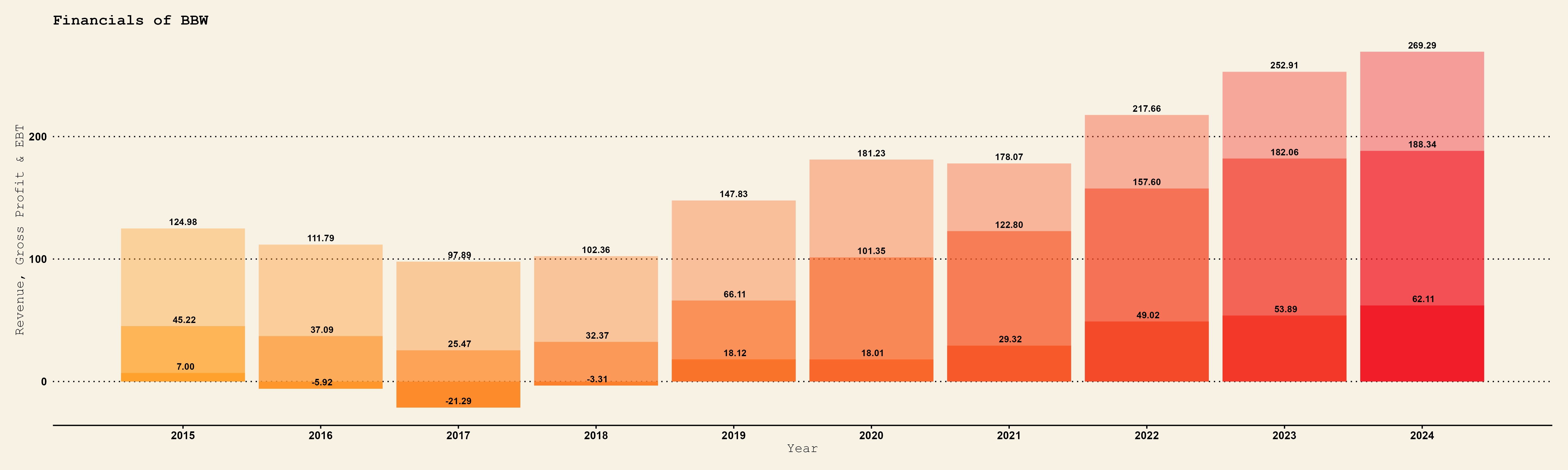

Azeus Systems Holdings, headquartered in Singapore, has undergone a remarkable transformation from an IT services provider to a leading player in the rapidly expanding Enterprise SaaS market. Leveraging years of experience in working on large-scale projects with national governments, Azeus has cultivated a reputation for managing complex projects and developing software while maintaining the highest standards of cybersecurity.

Several years ago, Azeus launched Convene, a board portal software solution that capitalizes on its accumulated experience and expertise. Convene assists organizations worldwide in conducting and managing board meetings efficiently and securely, whether in-person or virtually. Despite its exceptional qualities as a sticky Enterprise SaaS business—including negative churn, over 90% gross margins, and highly attractive returns on incremental capital—Convene has remained somewhat obscured from investors due to its integration with the legacy IT services segment.

Over the past five years, Convene has exhibited impressive growth, with annual revenues soaring from under $1 million USD in FY16 to nearly $15 million USD in FY21. Despite these promising prospects, Azeus trades at only 7 times EV/TTM Revenues, even when assuming the IT services business holds no value. Comparable top-tier Enterprise SaaS companies, albeit larger, command much higher multiples, with median multiples around 10 times at the time of Daniel's analysis. Consequently, Daniel believed that Azeus represented an undervalued opportunity in the market.

What happened next

Azeus Systems has continued to grow at a healthy pace since Daniel's pitch, with margins also expanding. However, the stock price has not reacted significantly to these positive developments.

My Learnings

Although the setup has not worked out yet, I do appreciate this type of pitch where a very valuable asset is obscured by a legacy business. On the other hand, I am a bit skeptical of the prices people assign to high-quality assets these days.

Four Corners Inc. (OTC:FCNE)

Pitched in the year end 2021 letter

Valuation at time of the pitch:

Stock price: 2.22

Market Cap: 24m

P/E: 7

P/S: n/a

Pitch Summary

Four Corners Inc. stands as the largest distributor of bingo and charitable gaming supplies in Texas, boasting a profitable business model that generates substantial cash flow while requiring minimal invested capital. Remarkably, the company distributes nearly all of its free cash flow (FCF) via quarterly dividends, yielding nearly 11% at the time of analysis.

Despite paying out the majority of its earnings, Four Corners has achieved remarkable growth in revenues and earnings before interest and taxes (EBIT), surging by 27.5% and 158% respectively since 2017. This showcases the company's robust operating leverage and effective business execution. However, despite these positive financial indicators, the market valuation has become disconnected from the financial performance. Shares of Four Corners are trading at only 7 times earnings excluding cash, with an enticing 11% dividend yield.

Given the strength and trajectory of the business since 2017, Daniel believes that shares present an attractive risk/reward opportunity. If shares were to re-rate to a more conservative 7% dividend yield, which is plausible, the stock could potentially see a near-term upside of over 50%.

What happened next

I couldn’t find financials for FCNE anymore, sorry.

Four Corners was bought out in 2023 for roughly 5-6 times EBIT. This seems absurdly cheap. Due to the company no longer being private, I cannot find much more information on the situation. From Daniel’s twitter commentary, I presume he didn’t hold a position anymore when the company was bought.

My Learnings

I do not have information on the corporate governance practices at Four Corners, so it is challenging to make a judgment call on whether investors could have foreseen what would happen with the asset sale at what seems like an absurdly low price. But it does underscore that it matters what mangements/board you trust with your money.

ECIP Banks (Citizens Bancshares (OTC:CZBS), M&F Bancorp (OTC:MFBP), and others)(2022- letter)

Pitched in the year end 2022 letter

Valuation at time of the pitch:

Stock price: N/A

Market Cap: N/A

P/E: N/A

P/S: N/A

Pitch Summary

In early 2022, Daniel came across an extraordinary special situation involving a group of small banks, some of which were publicly traded, set to receive substantial capital injections under the Emergency Capital Investment Program (ECIP) initiated by the US Treasury. These banks were slated to receive new, non-dilutive capital at highly favorable terms—up to 2-3 times their existing equity—in the form of non-cumulative, perpetual preferred stock with a nominal 2% annual rate and a grace period of two years before any payments were due. Remarkably, despite the banks publicly announcing this significant capital infusion, along with its advantageous terms, through press releases as early as late 2021, their stocks saw minimal movement.

Recognizing this unprecedented opportunity, Daniel meticulously researched all publicly traded ECIP recipient banks and identified those offering the best risk-to-reward profiles. Subsequently, he made a strategic decision to include a basket of these banks as a significant portion of the portfolio, confident in the potential upside they presented.

What happened next

I think this is one of the most unique trades and situations in financial history. And people like Daniel, who were smart enough to buy the shares during 2022, were handsomely rewarded, with the share prices of some of these ECIP banks quadrupling over the year. Investors started to realize how this cheap capital injection would boost the banks' earnings and enhance the all-important return on equity (ROE) of these smaller banks.

My Learnings

Although I assume this exact situation will never repeat itself, I think there are many things people can learn from this trade. Firstly, the importance of the cost of capital in banking and how reducing this can lead to enormous returns.

Secondly, I believe this situation was uniquely overlooked, but it was obvious to people who understood banking that it should generate value. So, look for understandable, large, and unique changes.

Cryosite (ASX:CTE)

Full length pitch february 2022

Valuation at time of the pitch:

Stock price: 0.43 AUD

Market Cap: 20m AUD

P/E: 10.5

P/S: 1.8

Pitch Summary

Cryosite, a small Australian clinical trials logistics provider, has navigated a tumultuous history but is now gaining momentum with consistent growth and a clear focus on its most profitable segment. Under management's strategic direction, the company has taken decisive steps to prioritize its most attractive business segment—clinical trials logistics—which is beginning to yield positive results. Despite its past challenges, Cryosite now demonstrates strong free cash flow generation.

Shares of Cryosite are trading at just 1.8 times Daniel's estimate of 2022 clinical trials logistics revenue ($9 million) and 10 times his estimate for FY22 enterprise value/free cash flow ($1.8 million). This valuation represents a significant discount compared to peers, which have been acquired at multiples of 4-5 times revenues.

Overall, Daniel sees Cryosite as an undervalued opportunity in the market, given its improving performance, strategic focus, and attractive valuation relative to industry peers.

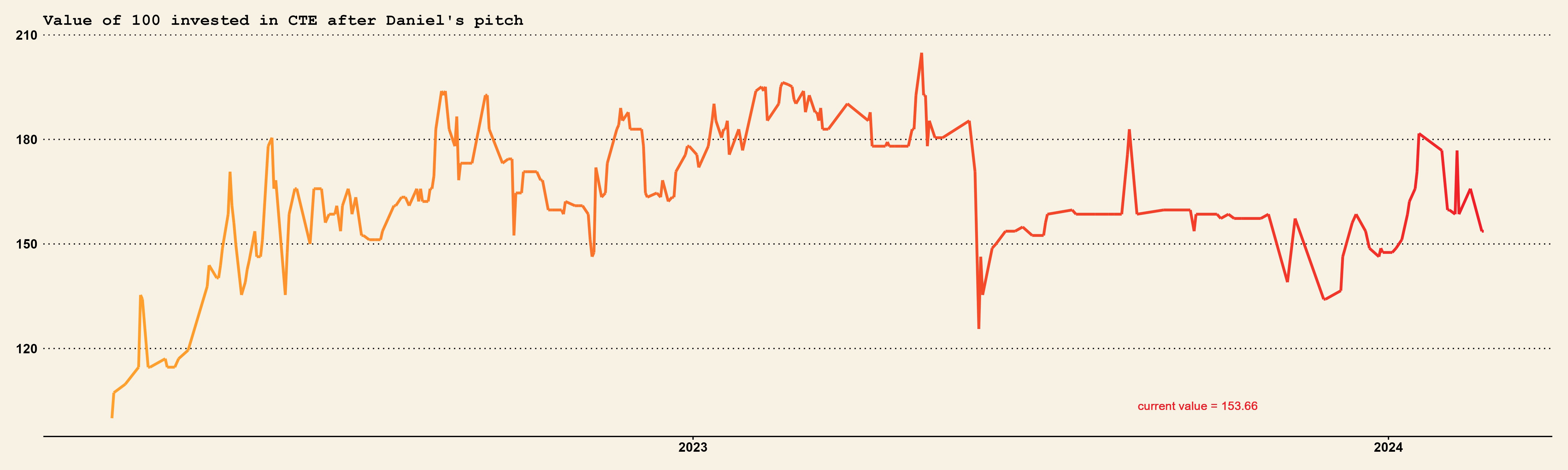

What happened next

Cryosite has continued its growth, albeit at a slower pace in recent years. The market does seem to have taken notice of the company's low valuation, increasing roughly 50% over the last two years, with some higher peak valuations in between.

My Learnings

I suspect Cryosite's results, although decent, might have even disappointed Daniel a bit. However, he likely still made money in this investment simply due to the undervaluation at the time he bought. I think this shows why investors appreciate a margin of safety.

From this point on, I consider the pitches too recent to analyze their subsequent events or draw any conclusions from them. Therefore, only a summary of the pitches will be provided.

Medical Facilities Corp. (TSX:DR)

Pitched in the mid year 2023 letter

Valuation at time of the pitch:

Stock price: 8.3 CAD

Market Cap: 207 CAD

P/E: 22.4

P/S: 0.37

Pitch Summary

Medical Facilities Corp. presents a compelling yet overlooked investment opportunity marked by a positive shift in capital allocation and corporate strategy. Despite owning surgical hospitals and ambulatory surgical centers (ASCs) in the United States, the stock trades in Canada. Historically, the company paid a substantial annual dividend through monthly distributions, yielding between 6-8% and even exceeding 10% at times. This high dividend attracted a shareholder base primarily comprised of Canadian retail investors, leading to steady performance until 2019.

In 2019, subpar acquisitions financed by debt resulted in underperforming assets, forcing the company to slash its dividend by 75%. This action prompted the retail investor base, which largely held the stock for its dividend income, to sell their shares, causing a sharp decline of over 65% in just six months. Consequently, the stock became attractively priced both on an absolute basis and relative to peers.

To capitalize on this opportunity, Medical Facilities Corp. is divesting non-core assets, directing all excess free cash flow to share repurchases, and exploring the potential sale of some or all of its facilities. Simply selling the existing business at 8 times enterprise value to earnings before interest, taxes, depreciation, and amortization (EV/EBITDA) would yield a return of over 100%, highlighting the significant upside potential for shareholders.

Hammond Manufacturing (TSX:HMM.A)

Pitched in the year end 2023 letter

Valuation at time of the pitch:

Stock price: 8.16 CAD

Market Cap: 92.4m CAD

P/E: 5

P/S: 0.4

Pitch Summary

Hammond Manufacturing ("HMM") is a significantly undervalued and often misunderstood company, according to Daniel. Despite delivering robust top-line and bottom-line growth comparable to or even better than its larger peers over the past 6-7 years, HMM trades at an extreme discount. Despite achieving healthy double-digit compound annual growth rates (CAGR) of 11.2% for revenue and 15% for gross profit over the last 7 years, the stock trades at a mere 5 times earnings.

Daniel argues that HMM has consistently outperformed its more highly valued competitors for nearly a decade, possesses real estate assets worth the entire market capitalization, and yet still only trades at a price-to-earnings (PE) ratio of 5. Even if it were to trade at a 50% discount to its peers, HMM would still present an 80% upside, and at a 30% discount, it would offer a 130% upside potential.

Goodheart-Willcox (OTC:GWOX)

pitch in the year end 2023 letter

Valuation at time of the pitch:

Stock price: 331

Market Cap: 155m

P/E: 15

P/S: 3

Pitch Summary

Goodheart-Willcox, an educational products provider specializing in Career & Technical, Health, and Physical Education, has historically maintained strong customer relationships and market share across various CTE subjects. However, recent years have seen a remarkable but underappreciated transformation within the company.

Beginning in 2018, the company's digital revenues started gaining significant traction, a trend that has only accelerated post-pandemic. Digital revenues now constitute almost 40% of total revenues and continue to grow at a rate exceeding 35% annually. Operating margins have surged to 30% and are still climbing, while the company's cash reserves are rapidly increasing, despite a large special dividend paid at the end of 2021.

Despite these impressive developments, shares of Goodheart-Willcox trade at only 3 times enterprise value/free cash flow (EV/FCF) and offer a yield of 6-7%. This valuation is significantly below comparables, which trade at 12 times FCF or higher. Notably, HMHC, a prominent comparable, was acquired by Veritas for 12 times FCF in 2021, a valuation that many shareholders deemed low. Based on these comps, Goodheart-Willcox could be valued at over $760 per share, indicating substantial upside potential.

Tying it all together

If we look at Daniel’s pitches discussed in this article, the first thing that jumps out to me is his incredible hit rate combined with the tremendous success of his winners. Out of the 13 pitches I consider to have been out long enough to judge, I consider 10 winners, with Azeus Four Corners being roughly flat and Dusk the only clear loser. This is an incredible hit rate, even better than the infamous quote:

“Even the best investor is wrong 1 out of 3 times.”

What makes this story even more impressive is the magnitude of some of his wins. HemaCare (26x) and Xpel (8x) of course stand out, as well as Heritage Global (6x) and the ECIP banks trade, of which some became multi-baggers over a very short time frame.

By shedding some light on these pitches and combining it with Daniel’s statement on his website on his strategy, I hope we can shed some further insights into the alchemy of such great returns.

Looking at the 6 pillers of Daniel’s approach to managing money, we can see how these helped in his returns. I think casting a wide net combined with passion has allowed Daniel to discover stocks that tend to be overlooked by the wider investing audience, which results in more misunderstood or mispriced situations.

Something that was difficult for me to highlight while given short summaries is the obvious amount of due dilligence Daniel has done on all the stock he pitches. Therefore, I highly recommend that you read every single pitch. I think this level of dilligence is the reason why Daniel is so well equiped to understand that a company’s financials and how and why it may change for the better.

Finally, Daniel heralds his alignment with his investors; however, I believe this is also something he values while investing in companies. Many, if not all, of his pitches herald the role of the CEO or large shareholder as a pivotal part of the pitch. So, someone investing in Smoak Capital is not only aligned with Daniel but also with the operator of the companies they invest in.

Finally, Daniel runs a concentrated portfolio which allows him to really focus on his stocks and make the weight of the winners felt.

I think putting this all together, Daniel runs a “no compromises small-cap strategy” where he has a:

Concentrated portfolio of companies he knows really well,

With improving fundamentals,

Value multiples,

Aligned management.

The only compromises Daniel has made are the ones that the small-cap investor should be willing to make, such as limited liquidity, no coverage, or a stock being outside most people's investment mandates. Add to that Daniel’s incredible skills, and you get returns so good that someone decides to write an article about them.

Thanks for reading

This article took a bit more work than my average one so sharing it widely would be much appreciated. Furthermore, I did enjoy the format myself, and I am looking for new candidates to also do an overview of. The characteristics I am looking for are:

Above average returns over a multi-year period

Good breadth of pitches to analyze (5+)

Preferably value and smaller-cap focused, but might also be fun to branch out.

This was an awesome read. Would love to have a deeper dive into his actual process. I'm also interested in what the companies looked like in the past just based on financial statements. It seems that some looked good, others bad, but those that looked bad had some sort of change going on within the company

Great read! Thanks for sharing this work freely publicly!

I have 2 points about Azeus I wanted to mention

- ttm p/e is ca. 25 and not > 100

- 1 Billion HKD = 172 SGD contract over the next 5-10 years with 75% of that being high margin SaaS-revenue as catalyst. (current ttm earnings = 10 mill SGD)