Decoding Success: Jeremy Raper [Part 2]

5 new deep dives in to Jeremy Raper's Memo's

Introducing Jeremy Raper

Welcome back to the Decoding Success series. Today we're diving into part 2 of our deep dive on Jeremy Raper, the legendary investor behind Raper Capital who achieved a staggering 130x return on his portfolio over 11 years

If you miss some background, I recommend starting with part 1 of this series, where I explored Jeremy's background in more detail.

This article follows the same structure as previous Decoding Success pieces: I'll summarize the key elements of his investment pitches, provide a post-mortem analysis of what happened after the pitches, and share my key takeaways.

Quick note: This is a longer piece, so I recommend reading it in the app or on the web rather than in your email for the best experience.

All pitches, I will cover on the blog in the coming weeks.

📖 Covered in Part 1

Elizabeth Arden – Short – June 2014

Aeropostale – Short – July 2014

GT Advanced Technology – Short – October 2014

Quicksilver Corp – Short – December 2014

Tuesday Morning – Short – February 2015

Chegg – Short – July 2014 (Selected "mistake pitch")

📍 Covered in This Article (Part 2)

Avolon – Long – March 2015

Afren Plc – Short – March 2015

Aercap – Long – October 2015

Peabody Energy – Short – March 2016

Universal Entertainment – Long – May 2016

🔮 Coming in Future Articles

Toshiba Corp – Short – June 2016

Sharp Corporation – Short – July 2017

Japan Display – Short – July 2017

Rezidor – Long – January 2018

Maxwell Technologies – Short – February 2019

Nio – Short – March 2019

Hexo – Short – October 2019

K+S Aktiengesellschaft – Short – November 2019

Tupperware bonds – Short – February 2020

Endor – Long – May 2020

Metlifecare NZ – Long – May 2020

Haier equity arb – Spread – December 2020

Automated Banking Services – Long – January 2021

Harbor Diversified – Long – February 2021

Hunter Douglas – Long – April 2021

Cardno – Long – September 2021

FAR Limited – Long – February 2022

Shell Midstream – Long – June 2022

Twitter #1 – Long – July 2022

Twitter #2 – Long – September 2022

Danakali – Long – October 2022

Montero Mining – Long – February 2024Avolon - Long - March 2015

Valuation at the time of the pitch:

Stock Price: $20

Market Cap: $1.572 billion

P/B: 0.72

Pitch Summary

JR pitched going long Avolon, an aircraft leasing company headquartered in Ireland, because he believed that at $20 per share, there was a significant margin of safety. He estimated the assets were worth around $28 per share. These assets consisted of the youngest fleet in the aircraft leasing space, which in his view might even justify a premium valuation. Furthermore, AVOL traded at a discount to peers across most valuation metrics.

Avolon had IPO’d in December 2014, and JR argued that part of the undervaluation stemmed from the company being under-covered and underappreciated by the market. The clearest sign of this was the known understatement of the fleet’s book value. Adjusting for this, the book value would rise from the reported 1618mm to 2186mm. At the time of the pitch, that meant the stock was trading at just 0.72 times adjusted book value, which JR considered too cheap for a business consistently generating returns on equity in the low to mid-teens.

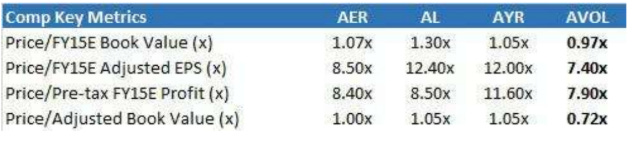

Compared to competitors, AVOL stood out with its younger, less risky fleet. Among the comps JR highlighted, AL was the best comparable, trading at a premium to book due to its similar fleet profile. AER and AYR, on the other hand, had older fleets and carried more risk.

JR noted that if AVOL were simply to trade at 1x adjusted book value, essentially at replacement cost, that would imply a stock price of $28, or around 40 percent upside. Given the company’s quality, solid management, and the discount to fair value, JR believed the downside was well protected.

What happened next

AVOL traded up about 20 to 25 percent in the months following JR’s pitch. The situation became even more favorable when Bohai Leasing announced a deal to acquire AVOL at $31 per share, a premium above JR’s estimate of fair value. This validated JR’s thesis and his adjustments to book value, as an industry player effectively confirmed his valuation by stepping in with a bid.

My Learnings

This was a clean and compelling pitch where JR focused on the quality of both the company and its underlying assets, recognizing a clear disconnect between accounting numbers and economic reality. Being able to identify these kinds of accounting misrepresentations can be one of the most powerful tools in an investor’s arsenal.

Afren Plc - Short - March 2015

Valuation at the time of the pitch:

Stock Price: 6.6 GBP

Market Cap: 74 GBP ($112)

P/B: N/A

Pitch Summary

Jeremy pitched Afren PLC, a West Africa-focused oil and gas exploration and production company, after it had already defaulted on a debt payment and announced plans for a likely highly dilutive equity offering. Despite these developments, the equity still had a notable market cap, and the borrow cost (at just 11 percent) was relatively cheap given the severity of the situation.

Afren had once been a stock market success story, rising from a penny stock in 2005 to a peak valuation of around 1.8 billion GBP just a year before JR’s pitch. This rise was driven by their producing oilfields in West Africa and Kurdistan. However, things took a sharp turn for the worse in 2015. Oil prices fell significantly, and major corporate governance issues emerged. The previous CEO and COO were found to have skimmed millions from the company and accepted various bribes. These issues quickly escalated into a full-blown crisis when Afren wrote down 80 percent of its 2C reserves in Kurdistan—from 1.2 billion barrels to just 250 million.

The final blow came when Afren announced that it was considering a financial restructuring after struggling to make a $50 million debt amortization on its first-lien bonds. While the company received multiple extensions, it ultimately defaulted on another interest payment by the end of March, just a week before JR’s article.

JR then analyzed what a restructured Afren might look like. At the time, the capital structure was as follows:

$220 million in cash

$310 million in first-lien debt

$860 million in second-lien debt

$112 million in market cap

This implied an enterprise value of around $1.08 billion. However, since the bonds were trading at a discount, the actual market EV was closer to $550 million, already hinting that the equity was significantly overvalued, making up about 20 percent of EV.

But the bigger issue was that Afren didn’t just need to refinance its existing debt—it also needed substantial new capital to fund ongoing cash burn in a low oil price environment, and to cover mandatory development capex in Nigeria to avoid losing licenses. JR estimated this shortfall to be between $350 and $450 million.

This meant that the restructuring would not only need to equitize the second-lien debt, but also raise significant new cash. Some second-lien holders had indicated a willingness to provide that additional capital. So, in the expected restructuring, bondholders would convert $860 million of debt into equity and inject another $350 million, resulting in around $1.2 billion in new equity.

Afren’s book value had previously been $1.98 billion, but that was before oil prices collapsed and Kurdistan reserves were written down. JR estimated the adjusted book value to be closer to $920 million. Using common sense, if debt holders were contributing around $1.2 billion in total value, there would likely be little or no room left for existing equity holders.

JR’s best-case scenario for current shareholders was that they might retain 1 percent of the restructured equity. Even if that traded at an aggressive 2 times book value, it would imply a remaining market cap of just $18 million—a downside of 85 percent. But JR expected the outcome to be even worse, and so he shorted the stock.

What happened next

Afren did propose a restructuring in which current equity holders would retain 11 percent of the new entity, but the deal failed to gain shareholder support. In July, trading in the shares was suspended due to the company’s failure to provide updated financial guidance. By August, Afren entered administration and the shares were delisted. Within just five months, the stock had gone to zero, delivering an excellent IRR for JR.

My Learnings

This was a great example of thoughtful restructuring analysis, a topic I’m not deeply familiar with. It was valuable to see how someone with a credit-focused background approaches distressed equity. Watching how JR mapped out the capital structure and anticipated the equity wipeout based on who would control the new entity was a masterclass in thinking like a creditor.

Aercap - Long - October 2015

Valuation at the time of the pitch:

Stock Price: $39.3

Market Cap: $8.1b

P/ad-B: 0.7

Pitch Summary

JR pitched going long Aercap (AER), another aircraft leasing company, after coming across it during his research into AVOL, which, as we know, was acquired shortly after JR’s pitch. His investment thesis for AER was based on similar arguments:

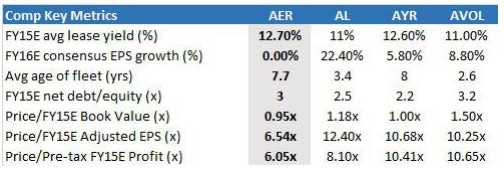

Compared to banks, AER produced better returns on equity while being less leveraged. That, in JR's view, should justify a premium to book value.

AER, despite being the best operator in the aircraft leasing space, was trading cheaper than peers.

The company traded at a steep discount to its adjusted book value, providing downside protection.

JR framed the first point as "corporate finance 101." He asked: what if AER were a bank or another financial services company? Valuing a well-capitalized bank is relatively straightforward. If a bank has a Core Tier 1 capital ratio over 10 percent, analysts typically assess its return on equity and compare that to its cost of equity. According to textbook finance, if a business earns a return on equity above its cost of capital, it should trade above book value.

AER had generated a 13.3 percent ROE through the cycle—suggesting, by those standards, that it should trade at a premium to book. While lessors like AER do have more concentrated asset exposure than most banks, they also use much less leverage. JR calculated AER’s Core Tier 1 ratio at 17.5 percent, significantly higher than typical banks. So AER offered stronger returns with less risk—yet it traded at a discount. That didn’t make sense to JR.

Beyond the broader point about leasing companies being undervalued compared to other financial firms, JR particularly liked that AER was the largest and arguably best-in-class operator in the sector. It had scale advantages, yet was priced as if it were one of the worst operators. That, to JR, seemed like a clear mispricing.

There was one more source of undervaluation. AER’s book value was understated relative to third-party appraisals of its aircraft fleet. Adjusting for those, AER was trading at just 0.71 times book value, creating what JR saw as a large margin of safety. He referenced his recent AVOL pitch, where the company was eventually acquired at 1.13 times book value, supporting the logic that aircraft fleets deserved fair value recognition.

What happened next

AER traded up moderately after JR’s pitch, reaching a pre-COVID peak of around $60—a roughly 50 percent gain. But JR actually held on through the COVID crash, as he later discussed on the Business Brew podcast. The pandemic hit airlines and leasing companies hard, and AER’s stock dropped so sharply that JR said he couldn’t even exit the position without selling at around 20 percent of book value.

Instead, JR doubled down and bought more shares near the bottom, which boosted his returns. However, in hindsight, he acknowledged the position was too large and the risk-adjusted return poor. He eventually exited the investment after the stock recovered, particularly when the company announced it would acquire a major competitor. JR disliked the deal and had lost faith in AER’s underwriting quality.

Interestingly, the stock continued to perform well after he exited. The integration of the acquisition went better than expected, and leasing companies benefited greatly from aircraft delivery delays at Boeing and Airbus post-COVID. The stock ended up doubling again from where JR likely sold.

My Learnings

Hearing JR discuss Aercap and his experience during the pandemic on the Business Brew podcast was very insightful. He admitted to holding the stock too long and in too large a size. While he had initially believed that AER, as the biggest player, could have better underwriting discipline, he later realized that being the largest player forces you to lease to nearly everyone, making that edge difficult to sustain.

There are important lessons here about sizing, thesis drift, and reacting to a market shock. JR knew the business well, but I’m not convinced it was the best buy during the COVID crash. He may have been influenced by endowment bias, doubling down on a stock he already owned, instead of reallocating capital to potentially better post-COVID recovery opportunities.

Peabody Energy - Short - March 2016

Valuation at the time of the pitch:

Stock Price: $6.4

Market Cap: $121mm

EV/EBITDA: 25x

Pitch Summary

Peabody Energy (BTU), a major U.S. coal miner, was a classic Jeremy Raper short:

The company operated in a structurally challenged industry.

It had an overleveraged balance sheet, and a clear credit-driven catalyst.

Credit markets were pricing in near-total loss for all classes of debt, yet the equity still carried a sizable market cap and was borrowable.

Coal companies had already been hit hard by 2015, with three major bankruptcies rocking the industry. Peabody had managed to survive, but JR took one look at the capital structure and concluded the equity was also headed to zero. He believed the pricing disconnect between the credit and equity markets was one of the most egregious he'd ever seen.

BTU had the following debt stack:

$2.2 billion in first lien debt trading at 37 cents on the dollar

$1 billion in second lien notes trading at 8 cents

$3 billion in unsecured notes trading between 5 to 7 cents

$700 million in convertible notes trading at just 1 cent

Despite this, the equity still carried a $121 million market cap. That implied a total enterprise value of $8.7 billion—assuming all debt would be repaid in full. But credit markets clearly disagreed. Based on where the debt was trading, the market was valuing the entire capital structure at just $2.2 billion. The implication was clear: the equity was worthless.

Even more compelling was the catalyst. Peabody was already in breach of its covenants. It was levered 6x to the first lien debt, while the covenant allowed only 4.5x. Of the $450 million in cash interest the company was paying annually, only 16 percent went to the first lien holders. JR pointed out that these creditors had no incentive to waive their rights, especially when most of the interest payments were benefitting subordinated debt holders. He expected this misalignment to drive the first lien lenders to push the company into bankruptcy quickly.

What happened next

JR’s thesis played out almost immediately. His write-up was released in March 2016, and by April, Peabody filed for bankruptcy. The stock collapsed from around $6 to $2 before being delisted. The equity went to zero, just as predicted.

Peabody eventually emerged from bankruptcy in 2017 with a clean balance sheet. But legacy equity holders received nothing. However, buyers of the deeply discounted second lien debt likely made a significant return through the restructuring.

My Learnings

This was another highly instructive case of practical restructuring analysis. JR showed how to bridge credit market signals with equity valuation, and how to use misaligned incentives between creditor classes as a forward-looking catalyst. If you want to get sharper on distressed situations or bankruptcy prediction, this is a great pitch to study.

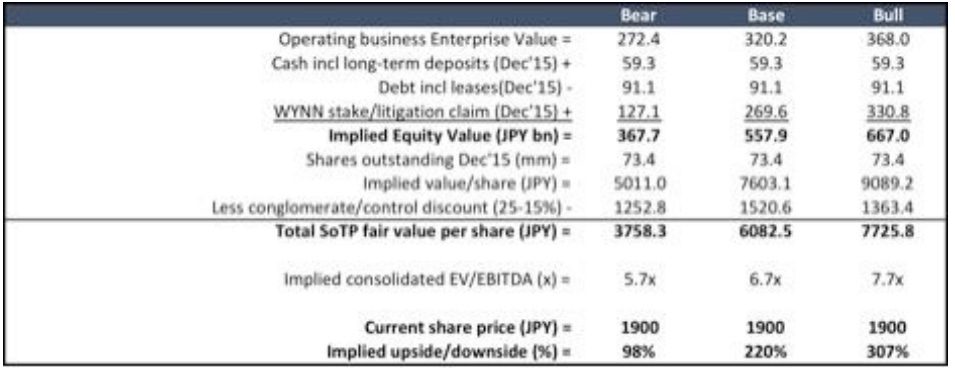

Universal Entertainment - Long - May 2016

Valuation at the time of the pitch:

Stock Price: $1900 JPY/share

Market Cap: $1.2B JPY

EV/EBITDA: 11x

Pitch Summary

JR pitched going long Universal Entertainment (6425.T), a Japanese manufacturer of pachinko and pachislot machines, because it was trading below even his conservative bear-case sum-of-the-parts (SoTP) valuation—implying a 100% upside in the worst case, with potential to multi-bag in more optimistic scenarios.

The thesis focused on breaking UE down into three parts:

The pachinko/pachislot business

The Wynn stake and associated litigation

The Manila Bay Resorts (MBR) casino project in the Philippines

1. Pachinko/Pachislot Business

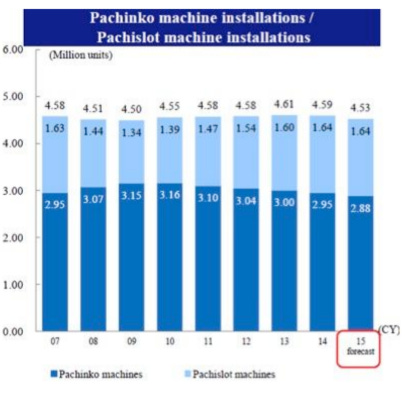

UE is an OEM for pachinko machines, a segment JR argued was not as bad a business as often perceived. His key points:

The industry had consolidated to 4–5 major players, supporting rational competition and operating margins above 15%.

While total installed machines were stable, pachislot machines (more similar to Western slot machines) were gaining share—UE was disproportionately exposed to this trend.

Players constantly demanded new games, creating historically high turnover rates of installed machines (close to 100% in some years). At the time of JR’s pitch, turnover was cyclically low (around 60%) due to regulatory changes.

Despite this downturn, UE still generated around ¥15 billion in stable annual FCF. JR valued this segment at 10–12x FCF, implying a value of ¥140–168 billion—more than the company’s entire market cap at the time.

2. The Wynn Stake and Litigation

UE had previously owned 20% of Wynn Resorts, but was forced to redeem its shares after Wynn’s board deemed its owner “unsuitable” due to allegations of bribing Philippine officials (related to the MBR license). Wynn redeemed the shares at $1.94 billion—around 30% below their market value—and paid with 10-year, 2% promissory notes instead of cash.

JR believed the worst-case scenario was clear: UE would keep the notes, receive minimal interest, and potentially recoup some legal costs. He estimated the value of this outcome at $1.16 billion (¥127 billion).

However, there was significant upside optionality from the litigation if UE could win a fair settlement—an option the market was giving almost zero value to at the time.

3. Manila Bay Resorts (MBR)

MBR was the wildcard and the likely key catalyst, positive or negative. The resort required over $2 billion in capex, forcing UE to borrow despite the cash flow from pachinko operations.

JR estimated that MBR would generate gross gaming revenue (GGR) of $1.08 billion by 2017. After paying a 25% regulatory royalty, that left $810 million. Hotel revenue could add another $114 million, bringing total revenue to ~$924 million. JR estimated 16% EBITDA margins, resulting in ~$148 million (¥16.3 billion) in EBITDA.

Applying a 9–11x EBITDA multiple, the casino would be worth ¥146–179 billion.

Sum-of-the-Parts Valuation

Putting it all together:

Even applying a significant conglomerate discount, the base-case valuation suggested a double, and more bullish cases implied much higher upside.

What happened next

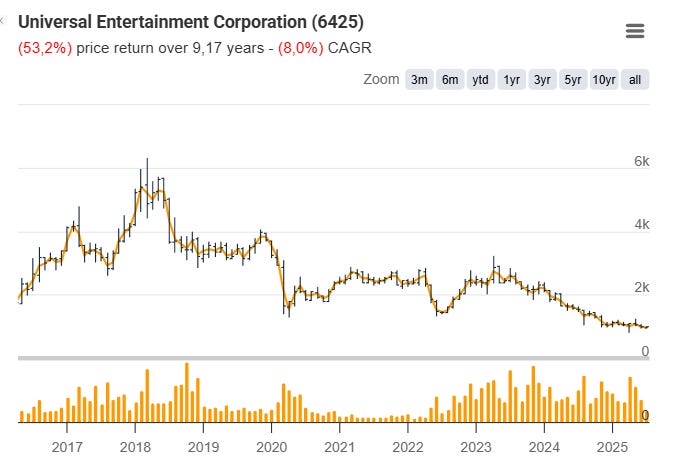

JR timed this one very well. The stock rallied hard after his pitch, hitting a high of ¥5,300—nearly a 3x from the time of publication. From 2017 to 2020, the stock consistently traded at levels that would have allowed for a double or better.

Some pieces of the thesis worked extremely well. UE won its litigation against Wynn in 2018 and was awarded $2.6 billion. MBR opened in 2016 and performed reasonably until COVID hit.

However, the pandemic crushed both of UE’s core businesses—pachinko and MBR—leading to a collapse in earnings and a brutal drawdown in the stock. It never fully recovered and now trades at just 0.2x book. Ironically, the same forgotten status JR initially exploited may now apply once again

My Learnings

This is a bit of a hard one for me as the stock work for some time to be ruined by covid, so it is hard to judge how accurate JR long term view of business quality was. I do think the pitch was a good example of a stock hated and forgotten by the market just spring-loaded with catalyst. I.e. the Wynn case and the opening of the resort. So I guess the learning is buy cheap and have many way to win.

Thanks for reading

Over the coming weeks, I’ll be publishing more articles covering the work of Jeremy Raper, breaking down his public investment memos one by one. If you enjoyed this piece and want to follow the rest of the series, make sure to subscribe so you don’t miss any updates.

If you’re eager for more right now, I recommend checking out the first article in the Decoding Success series, where I covered another exceptional investor, Daniel Smoak, who, like Jeremy, has delivered a CAGR in the 50% range.

That's amazing performance. Outside of NVidia not a single compnay on the Wilshere 5000 has generated even half that. In other words, the second best performing stock on the enitre US stock market, generated roughly 5,500% TR. Incidentally, it was a company called IES Solutions. In the UK, the best performer, Greatland Gold has done less than a fifth of JR