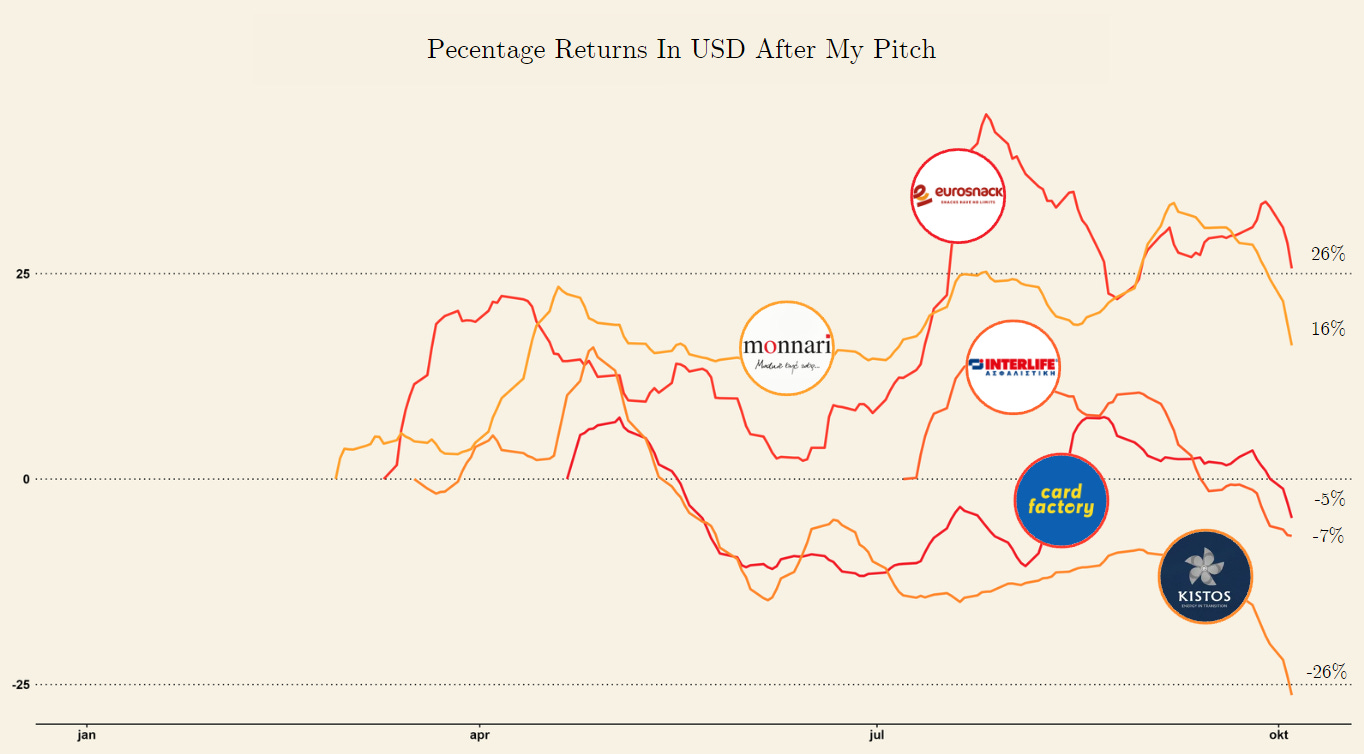

H1 2023 and Me

H1 2023 Stocks Update

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

Intro

As the dust settles on the half-yearly financial reports for 2023 from companies worldwide, it's time for a concise update on the five stocks I've pitched since I started my SubStack this year. While most of these companies have roughly performed in line with my expectations, the markets haven't been as forgiving. However, I firmly believe that despite recent setbacks, the foundations of my investment theses remain robust, and in some cases, the prospects have grown even more enticing. Hence, for anyone who has followed these stocks or might even own them, I thought a short update on all of them would be warranted.

The format will proceed as follows: I will begin by briefly summarizing my previous thesis. Next, for each of the five stocks, I will provide key events from the year-to-date chart. Finally, I will offer commentary on how these events relate to my thesis.

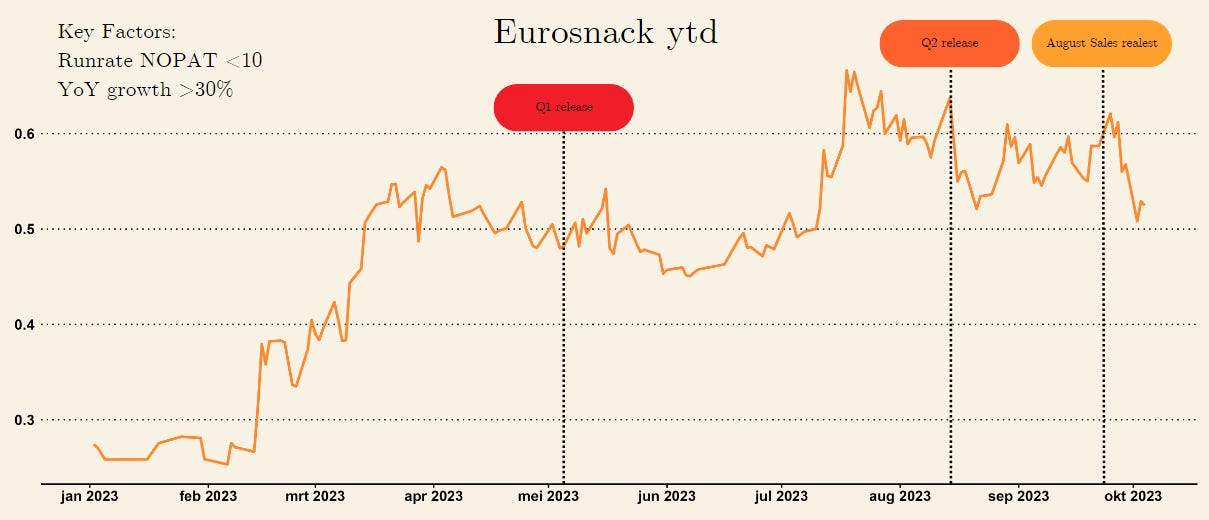

Eurosnack S.A.

Thesis recap

Let's begin with the standout performer year to date, Eurosnack S.A. This Polish company specializes in the production and distribution of salty snacks and biscuits. My initial pitch for Eurosnack was straightforward: it was (and still is) undervalued, considering its impressive growth trajectory. I believed that its margins were temporarily compressed due to short-term cost inflation, and there were additional opportunities for margin expansion as the company continued to scale.

Key events and thoughts

A strong Q1 report.

An exceptional Q2 report, marked by significant margin expansion and growth.

August 2023 witnessed record-breaking monthly sales.

As stated in my summary, the key factors of my Eurosnack thesis were continued growth and margin expansion. Both of these elements are tracking nicely. Q1 2023 had 35% YoY growth, although it was slightly behind Q4 2022. The real juice in the story comes when we consider that Q2 had a 47% YoY growth as well as gross margin recovering sharply back to 52% from the lows of 47% the previous year. This combined growth and margin expansion led to a record quarter for Eurosnack, where they produced 3 million PLN in profits for the quarter. It should be noted that this quarter was used by some people to sell larger positions in this illiquid stock, resulting in a huge drop on a day when the company reported an absolute record quarter, and the stock is still below the price level from the reporting date. Given that they are still growing quarter on quarter, I think it is quite reasonable to assume a run rate 12m NOPAT is possible. Adding in some minor dilution, we are trading at a sub run rate PE of 10 now, with the company executing on all cylinders.

Furthermore, we had a record quarter for August, where the company had 14.5 million+ PLN in revenue for the month. This is significantly higher than the previous highest month, which was March this year at slightly less than 13 million for that month. This is also nice to see, as although the company was growing, it had a hard time beating December 2022's 12 million+ in revenue. With August finally easily getting away from the 12 million in revenue mark, I am now still quite comfortable with future growth. With the first 8 months of revenue being reported, we know the company has earned 93.5 million PLN in revenue for those months. My estimate is that the full-year revenue will fall in the 138 million to 150 million range. This does mean my original write-up was a bit ambitious in projecting 150 million in revenue for 2023, as that is now the very high end of the range I think we can expect this year.

In short, I think the thesis is tracking incredibly nicely, and I might look to add in the future, as I believe recent price developments don't match the underlying business results.

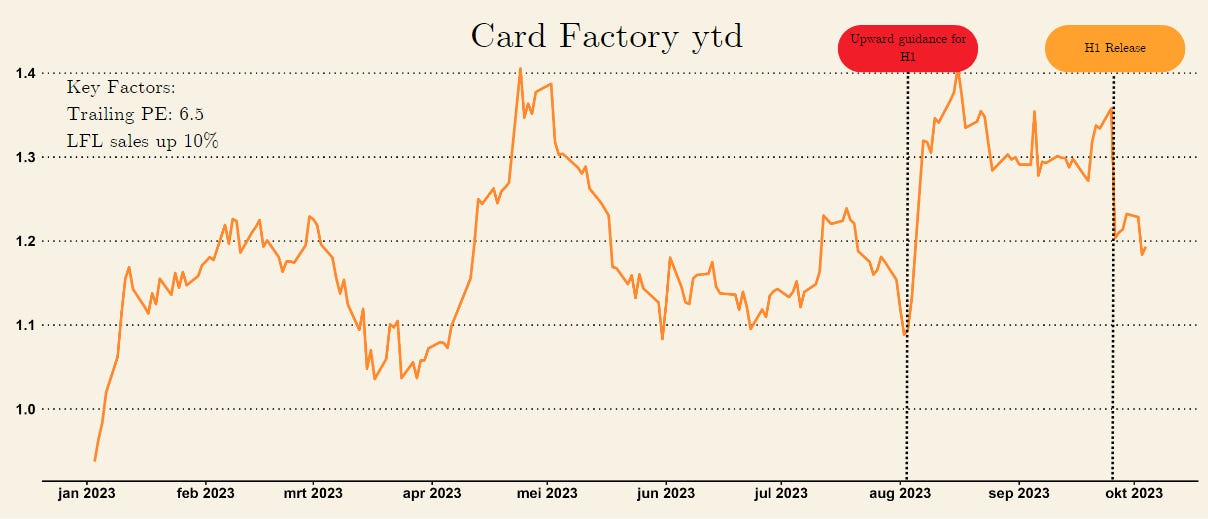

Card Factory PLC

Moving on to Card Factory, a specialty retailer based in the UK known for its wide range of greeting cards and gifts. Card Factory's vertically integrated model has consistently delivered exceptional value for money, earning it the title of the #1 value-for-money retailer in the UK for several years. I firmly believe that the stock is currently trading at an extremely attractive valuation, with a price-to-earnings ratio of just 7x based on trailing earnings. Additionally, the company's low-risk, low-capital growth plan, coupled with diminishing competition, makes it a highly compelling investment opportunity.

Key events and thoughts

An upward revision of guidance for H1.

An outstanding H1 report, featuring a remarkable 10%+ year-over-year increase in like-for-like sales.

A major shareholder selling shares.

Anticipated resumption of dividends, scheduled for January next year.

Card Factory PLC, similar to Eurosnack, reported an excellent first half (H1) performance. However, the stock subsequently traded down upon the release of the report. Card Factory reported an 11.5% year-over-year (YoY) growth for H1, which included a 10% increase in like-for-like (LFL) sales in their retail stores, and notably, a 13.1% LFL growth in the gifting category, one of their major strategic initiatives. So, why is the stock down? While we can't know for sure if it's the sole reason, the largest shareholder, Teleios Capital Partners LLC, has been selling their shares quite indiscriminately. After the report, shareholders were notified that Teleios reduced their share holdings from 14.9% to 11.7%. Teleios has been selling for some time, also divesting 5% of their shares in the past to JP Morgan.

Now, let's return to the results. I believe we can see that the new management is simply better at retailing (which is very challenging) compared to the previous management. We can observe some of the key initiatives coming into action, with the gifting category showing robust growth, and cards now accounting for less than 50% of the revenue. Furthermore, a new partnership was trialed with Matlan in the UK for 20 stores, with an additional 200 stores set to roll out by the end of the year. Management is clearly executing on their previously set goals of increasing the share of gifts and forming more partnerships. The financials also support this. Normalized EBIT was up 27% for H1, and NOPAT (Net Operating Profit After Tax) increased by 66% to reach 19.2 million. The trailing price-to-earnings ratio (P/E) of Card Factory is now 7. Given that I expect the second half (H2) this year to also perform significantly better than H2 last year, we are likely trading at roughly 6 times the end-of-year earnings.

In my opinion, this is an incredibly attractive valuation for the number #1 value retailer in the UK, especially considering their effective strategy that management is clearly executing. Furthermore I think the reusmtion of the dividend after January next year should help is a nice catalyst for the stock. However, similar to Eurosnack, I believe recent price movements do not accurately reflect the strong underlying business fundamentals. Nevertheless, I probably won't add more to my Card Factory position as it's already my largest holding.

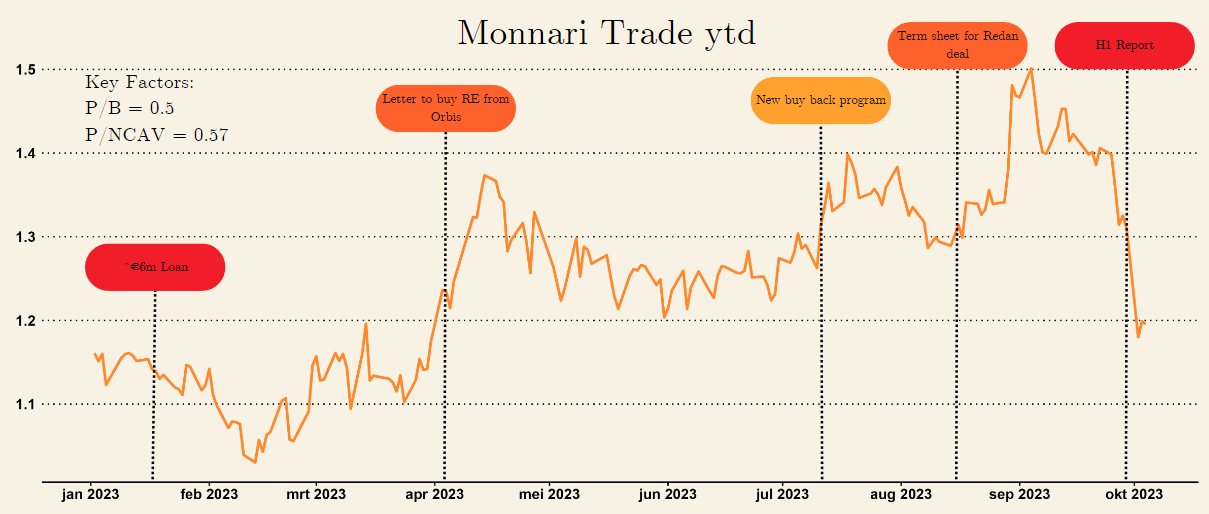

Monnari Trade S.A.

Monnari Trade S.A. holds the distinction of being the first stock I ever publicly pitched. Monnari Trade is a fashion retailer in Poland, primarily catering to women of middle age and older. Since 2015, the company has made significant investments in real estate. Following the sale of non-core real estate assets, the company now boasts a substantial cash reserve and retains valuable remaining real estate holdings.

When we incorporate the value of these remaining non-core real estate assets into the company's current assets, Monnari Trade is trading at an attractive 40% discount to its net current asset value. This is particularly compelling considering that the core business continues to generate earnings. Furthermore, the fact that the founder and CEO owns a significant portion of the company's stock and demonstrates a commitment to deploying capital judiciously adds to the attractiveness of this investment opportunity. In my opinion, this makes Monnari Trade one of the most compelling net-nets in the world.

Key events and thoughts

Signing a letter of intent to purchase a property from Orbis for 18 million PLN.

6 million euro loan to a real estate developer.

Commencing a new buyback program.

Signing a term sheet to acquire two brands from Redan for 9 million PLN.

A lecluster H1 report for the core clothing business.

I've done a decent-length update on Monnari Trade that covers the first three points, so all I'll do is comment shortly on the last two developments as they were subsequent to my previous update

As I mentioned in my previous update, the CEO of Monnari believes that synergies can be unlocked by acquiring other clothing companies. Quite shortly after my last update, the company announced their first target. They are set to take over two brands, Top Secret & DryWash, from another struggling publicly traded Polish company, Redan S.A. ($RDN.WSE). As part of the proposed deal, Redan will continue to handle the logistics for the TopSecret brand and take over the logistics of Monnari Trade's eCommerce operations.

The currently proposed deal is valued at just 9 million PLN, while Redan has recorded revenues of 96.5 million, 94.3 million, and 81.55 million for the last three full years, and was just below breaking even last year. Although we might need to account for the value inherent in the logistic agreement, the transaction appears to be valued at a fraction of Redan's sales, something like 1/10th. Furthermore, TopSecret also focuses on women's fashion and is headquartered in Lodz. Therefore, consolidating offices and other potential synergies seem like readily achievable benefits.

We are still awaiting the finalization of the deal, but if it is anything close to the proposed terms, I believe it could be very value accretive for Monnari investors.

Secondly, the H1 result did disappoint a bit. Although the company recorded a healthy enough operating profit at the capital group level of 5 million PLN for the first half-year, this did disappoint as the core business put up decent growth at 10% vs. clothing inflation of 7% in Poland and great 60% gross margins. This did not translate into meaningful profit for the core business as SG&A was up a staggering 25%. Cost control at an operating level is core for the core business to inflect and unlock the true value of Monnari; however, this clearly didn’t pan out in H1. Let’s wait and see if the deal with Redan goes through and if they manage to realize some synergies.

Lastly, the report reported 3.8 million in revenue from renting out the commercial spaces in the Geyers Gardens, their real estate project. So for the full year, this would be roughly 7.6 million in rental revenue. The Geyer’s Gardens and other investments in real estate are currently marked on the books at 75 million PLN. So, this implies a rental yield of 10%. This seems very high, especially once we consider that a significant part of the Geyer’s Gardens isn't rented out.

As the picture above shows, some of the large commercial spaces in the Gardens are still available for rent. This should significantly add to the amount of rent collected once tenants are found. Furthermore, the report also states that some of the office space located on the second floor of the project is still available for rent. Lastly, the plot of land around the property the company sold will be filled with apartments. I am not a real estate expert, but bringing more customers closer should enhance the value of a property significantly. So, at the current 10%+ rental yield to book value, the properties seem extremely undervalued on the books, given that rents have all the reason to keep increasing significantly.

In short, I was a bit disappointed with the performance of the core clothing business, yet Monnari is still undervalued on an asset basis with the CEO deploying cash in interesting ways. Especially the Redan deal can be a huge catalyst for the company.

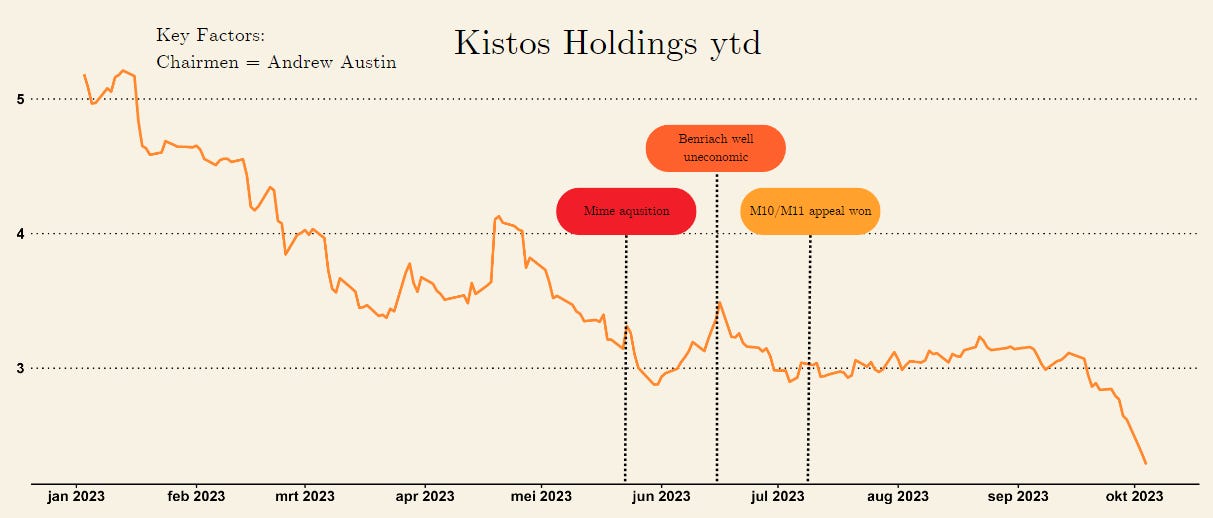

Kistos Holdings PLC

Kistos Holding PLC, a North Sea oil and gas producer operating in the UK, Netherlands, and Norway. My thesis primarily revolves around the exceptional capital allocation skills of the company's chairman, Andrew Austin. Coupled with the fact that the company appears to be undervalued based on its assets, I believe it remains highly attractive.

Kistos's ability to generate consistent cash flow and its excellent management team make it a compelling platform for creating value. The company excels in acquiring and optimizing small assets in the North Sea, making it an attractive opportunity for investors.

Key events and thoughts

Ongoing tax uncertainty in the UK and the Netherlands.

Halfing of gas prices.

Mime deal and entrance into Norway.

Reinstatement of M10/M11 license, with Kistos planning to conduct test drilling.

Benriach exploration found to be uneconomical.

Kistos' stock has taken a significant hit this year, primarily due to a combination of falling gas prices and unfavorable tax changes. Meanwhile, the company has successfully completed a new acquisition – they purchased Mime, marking their entry into Norway. This deal was structured in a manner consistent with Andrew Austin's approach, with Kistos providing no upfront cash payment. Instead, they issued a set of warrants to the equity holder and assumed Mime's debt.

While, in terms of raw value, it appears that Kistos secured a favorable deal, there are two other noteworthy aspects to consider. Firstly, the entry into Norway was achieved at a relatively low cost. Andrew has always emphasized the expense of entering the Norwegian market, which deterred previous attempts. Now, with Mime as a platform, Kistos can pursue future acquisitions in Norway more efficiently. Secondly, this acquisition extends Kistos' production profile significantly. For instance, if the Q10-A Orion oil field in the Netherlands doesn't receive approval, Kistos' production profile for 2024 and beyond would have been considerably smaller.

Interestingly, the M10/M11 license was reinstated after Kistos appealed the Dutch government's decision not to extend their license. This reinstatement adds a substantial 2C resource to the company. However, I remain cautious about the chances of these fields being developed. Despite Kistos' plans to drill appraisal wells, there have already been complaints from local residents. Furthermore, the entire island north of these gas fields is designated as a nature reserve, further complicating any development plans.

Lastly, the Benriach exploration well has been completed but has proven to be subeconomic. This was always a long shot, and it's important to note that Kistos is not primarily an exploration company. Nevertheless, it would have been beneficial to secure another decent-sized UK asset for investment purposes, especially to take advantage of the investment allowance.

Kistos is a stock that is currently trading lower than its summer 2021 levels, despite what I believe to be excellent management execution. The decline in Kistos' stock price can be attributed primarily to factors within their control, such as changes in tax regulations and a decrease in gas prices. However, as Andrew has pointed out, the company's potential for earnings seems promising from this point onward. If oil and gas prices fall, the UK windfall taxes are likely to be removed, and if prices rise, well, the company stands to benefit. In my opinion, Andrew and the entire Kistos team consistently demonstrate their expertise as some of the best deal makers in the UK. Given the current stock prices, it appears that nearly all the negative factors have already been factored into the stock's valuation.

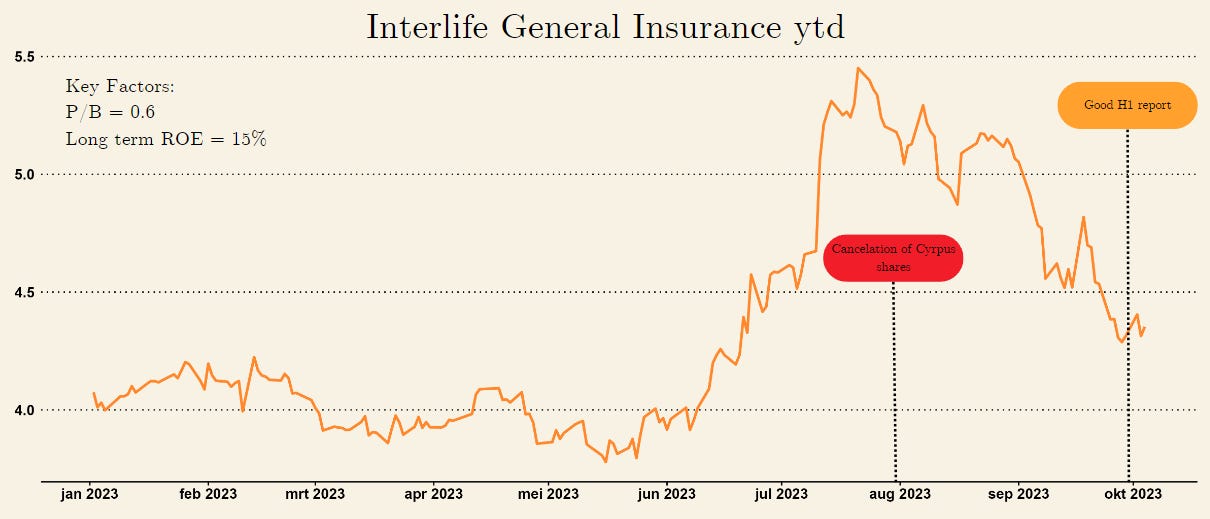

Interlife General Insurance S.A.

Finally, let's discuss Interlife General Insurance S.A., a Greek insurance company specializing in non-life insurance. My pitch centers around Interlife's remarkable historical performance, boasting one of the best combined ratios in the insurance industry. However, last year, their results were significantly impacted by inflation affecting underwriting and a substantial drop in the value of their bond portfolio due to a sharp increase in interest rates.

If the company can return to its historical underwriting excellence and benefit from an improved yield on its bond portfolio, I believe Interlife has the potential to trade at a remarkably low multiple of its normalized earnings power. Furthermore, considering its excellent track record of compounding value for shareholders, Interlife stands in a league of its own.

Key events and thoughts

Good H1

Natural disasters in Greece

Cancelation of the shares on the cyprus exchange

Last, but not least, is Interlife. The stock is flat on the year and down significantly since I wrote about it. However, H1 results were great and reflect well on my thesis. Firstly, we saw a strong return on the investment portfolio with $12 million in gains, compared to last year's $17 million in losses on the portfolio. Their combined ratio was also around 10%, which is already much better than last year's roughly 6%. I am still quite confident that the company can keep their combined ratio above 10%, moving toward their historic 15%, given their cost advantage over the competition. Earned premiums were slightly lower than I expected as the company had announced they grew written premiums by 15%. However, they ceded a little bit more to reinsurance than I expected, so net earned premiums were up roughly 11%. Basically, I think we can see once again that Interlife is an excellent insurance company. I think this first half-year shows that the company can keep delivering exceptional underwriting results while also generating significant earnings from their investment portfolio.

Another important event was the occurrence of multiple significant natural disasters in Greece over the summer, including large wildfires and flooding. The company does write some fire and natural disaster insurance. I don't think the tragic events in Greece over the summer will hurt Interlife too much, as the relevant lines of business are significant but not too large, and the areas that have been affected are economically less significant to Greece, so their share in premiums should also be lower. I think it's safe to say the underwriting ratio will be a bit worse for the second half of the year, but nothing to worry about.

Again, I believe my thesis is tracking very well, but the market is not reflecting it at its current price. Interlife is still a small position, but I am quite eager to expand its role in my portfolio given the disconnect between underlying business performance and market performance.

Update & Upcoming Articles

Thanks for reading this update. I am also looking forward to sharing pitches on new stocks, as I am not fully satisfied with my current backlog since I have written a decent amount on the same stock. However, with summer vacation, my graduation from my master's degree, and looking for my first full-time job, as well as a certain lack of great ideas, life just got a bit in the way.

I have, however, created some ideas for upcoming articles that I plan to release and will now share to hold myself accountable:

First, I'd like to write an article featuring stocks on my watchlist that are enticing me to conduct more in-depth research on certain names.

I've been working on an article discussing a pair of stocks (Lee Enterprises & Barnes & Noble Education) that are both priced more like long term options due to their high-risk, high-reward setup.

I might consider a general overview of my investment strategy or share insights on idea generation if people would be interested.

Expect deep dives on stocks from my watchlist and any new ideas.

I am happy to hear any though on future content in the comments.

Good write up Iggy! Every bit with you on CARD

Thanks for the update. Great read. Maybe write about your investment process? How to choose when to add a position relative to what you already own? When to sell, etc...