Interlife The Next Davis Double Play

From The Good, The Bad & The Ugly to The Good, The Great & The Wonderfull

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

Executive summary

Interlife is a company that trades for an estimated forward multiple of 3x market cap/EBIT and 66% of book value. These multiples seem completely ridiculous once you consider the company has compounded its share price at 19% since 2014 and has ample opportunity for growth and to keep redeploying capital. The business is founder-led and has consistently taken market share from its competition. So, what's the catch, you ask? Well, Interlife General Insurance SA is the only listed Greek insurance company, a microcap with low liquidity, and only has Greek financials. However, with a solid balance sheet, excellent owner-operator, and the potential to benefit from rising rates, I believe this presents a once-in-a-lifetime opportunity to purchase a compounding machine at a deep-value multiple. lets dive in:

History

Interlife was founded in 1991 by Ioannis Votsaridis(71) in Thessaloniki, Greece, and has since expanded throughout the country. The company has achieved successful vertical expansion, offering a wide range of non-life insurance products, with its largest sector being car insurance. As of 2023, Interlife is ranked as the 12th largest insurer in Greece based on premiums written, out of a total of 45 insurance companies in the country. Interlife operates through three offices and employs 152 individuals. Additionally, it has established partnerships with 1800 insurance agents who sell its products, following a similar model to insurance sales in the United States. The company proudly serves 444,787 private and professional clients, providing them with insurance coverage, from ships to drones.

In 2012, amidst the Greek crisis, Interlife went public by listing on the emerging companies exchange in Cyprus. Despite the economic turmoil and austerity measures in Greece, Interlife proved to be recession-resistant. While the Greek GDP plummeted, the company's equity grew significantly from 21 million in 2012 to 113 million by the end of 2022, showcasing a remarkable compound annual growth rate of 15%. Shareholders who held the company's shares in the long term were equally rewarded, with the share price compounding at a similar rate to the equity. Moreover, in 2021, Interlife achieved a dual listing for its stock on the main market in Athens, further solidifying its position in the industry.

Mr. Votsaridis and his family currently own 61.82% of the company's shares, indicating their substantial stake and influence in the business. Based on the available information, Mr. Votsaridis appears to be highly respected in the Greek insurance industry. He frequently writes articles and papers on the Greek insurance market. With his cunning demeanor, Mr. Votsaridis evokes the image of a sophisticated Bond villain, and I find this rather positive as it deviates from the stereotype of a pajama-clad tech billionaire looking to pilfer your money.

(Greek) Insurance, From The Good, The Bad & The Ugly

Insurance is a confusing business with very unique economics. Insurance is famous for building fortunes, such as that of Warren Buffett and Shelby Davis, the patriarch of the Davis family. However, nowadays many insurance companies are traded below book value, with all the returns that shareholders get being through dividend yield, while the stock goes nowhere. Both Buffett and Shelby have written about the good, the bad, and the ugly of the insurance industry. Let's look at some of their quotes to shed light on the unique strengths and weaknesses of the insurance industry:

The good

"Insurance companies enjoyed some terrific advantages, as compared to manufacturers. Insurance offered a product that never went out of style. They profited from investing their customers' money. They didn't require expensive factories or research labs. They didn't pollute. They were recession-resistant. During hard times, consumers delayed expensive purchases (houses, cars, appliances, and so on), but they couldn't afford to let their home, auto, and life insurance policies lapse. Because interest rates tend to fall in hard times, insurance companies' bond portfolios become more valuable.

These factors liberated insurers' earnings from the normal business cycle and made them generally recession-proof."

~ Davis Dynasty, page 96

The Bad

"In such a commodity-like business, only a very low-cost operator or someone operating at a protected and unusual small niche can sustain high profitability levels."

~ Warren Buffet, Berkshire annual report 1985

The Ugly

"[Insurance] is cursed with a set of dismal economic characteristics that make for a poor long-term outlook: hundreds of competitors, ease of entry, and a product that cannot be differentiated in any meaningful way."

~ Warren Buffet, Berkshire annual report 1988

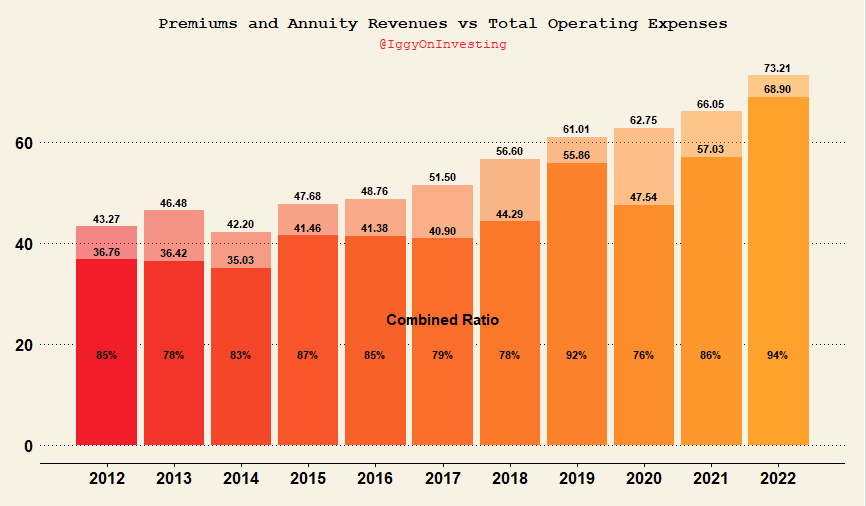

Okay, let's address these quotes. First, 'The Good' – some of this is clearly present in Interlife. Even with the Greek economy in a slump, the company managed to do very well. However, the Greek crisis was so severe that premiums in the country did drop significantly. Combined with a drop in the value of assets during the financial crisis, strengthened regulation, and a general trend of consolidation, the Greek insurance industry went from 106 companies in 2001 to just 45 in 2023. So, 'The Ugly' clearly applies much less to the case of Greek insurance. New entrants are basically nonexistent, with the industry having fewer and fewer competitors.

Consider that half of these are life insurance companies, meaning Interlife competes with just about 20-30 companies. In some specific lines, the competition is much less. This leads to pricing in Greek insurance being much more rational (some might even say cartel-like) compared to many other Western nations where combined ratios are around or above 100% most years. Yet, Greece has a 5-year average for non-life combined ratio of 90% (Interlife is significantly better with a 5-year average of 85%). So, clearly, the Greek insurance market is not characterized by cutthroat competition.

The bad: Due to the commodity-like characteristics of insurance, low-cost operators tend to thrive. Although Interlife does not have as large a cost advantage as, let's say, Geico, which benefits from significantly lower acquisition costs due to selling directly, Interlife sells all its policies through insurance intermediaries. However, being owner-operated and small at the time of the crisis, Interlife seems to have better cost control than the average Greek insurance company. The average expense ratio (policy acquisition cost + SG&A / Gross Premium) over the last 5 years for the Greek insurance industry is 48% (this is the highest in the EU), while Interlife's ratio is only 31%. So, Interlife enjoys a 17% cost advantage over the average Greek non-life insurer. This fact becomes even more remarkable when considering that Interlife has experienced growth in the number of policies written in the last 5 years. Acquiring policies, especially through brokers, is expensive, which means Interlife's expense ratio is actually overstated for a no-growth scenario.

So looking back at the quotes from Davis and Buffett, we see that the Greek Insurance Industry, and especially Interlife, isn't characterized by "The Good, the Bad, and the Ugly," but actually by "The Good" (recession-resistant), "The Great" (a huge cost advantage), and "The Wonderful" (an insanely uncompetitive landscape characterized by consolidation).

The Numbers

As stated before, Interlife has a great track record as a public company. It has compounded its book value, which is a shorthand for the value of an insurance company, at a 15% CAGR since 2012. This impressive growth rate includes last year, which was characterized by carnage in the bond market and a relatively poor underwriting year due to inflation. Despite these challenges, Interlife has managed to generate significant value. Additionally, Interlife has paid a small dividend most years, further highlighting its ability to generate returns for shareholders.

Interlife has grown its equity faster than written premiums, which has been part of their strategic approach. The management's goal was to reduce the risk associated with underwriting too many premiums against the surplus. As a result, Interlife has consistently seen its Solvency Capital Ratio and minimum Solvency Ratio rise, currently standing at 196% and 600%, respectively. This strong capital position allows Interlife to write the amount of business they deem optimal, rather than being forced to write more to stay profitable or write less due to insufficient capital.

This approach proved beneficial, particularly last year when their bond portfolio, like many others, experienced a significant decline due to rising interest rates. Instead of being forced to write less business, Interlife managed to write 17% more premiums in the first four months of 2023 compared to 2022. Being well-capitalized also provides insurers with greater flexibility in their investments.

At present, Interlife does not hold many shares, which make up only 17% of their portfolio. However, as an insurance company becomes more overcapitalized, it can start to resemble companies like Berkshire Hathaway or Markel. Although there is limited evidence suggesting that this is the future of Interlife and that they have the expertise to pick stocks, the overcapitalization provides both downside protection and optionality, which is advantageous.

Based on the information provided, Interlife is expected to write approximately 85 million in premiums for 2023, with 115 million in equity. The company's total assets amount to around 280 million, consisting of 193 million in financial assets, 26.5 million in real estate investments, and 32 million in cash. The remaining balance consists of operating assets. On the liabilities side, Interlife has approximately 165 million, with 118 million allocated to unpaid claims and 32 million to unearned premiums. The rest comprises operating costs and other smaller items. Therefore, the company has around 150 million in float (other people's money) and 115 million in equity. Based on these numbers, we can make some estimations regarding Interlife's earnings power:

Let's start with conservative estimations. The lowest combined ratio for Interlife was in 2022 at 94%. If we assume that in 2023 it writes business at a combined ratio of 94%, we can estimate underwriting profits of 0.06 * 85m = 5.1m. Considering the earning assets of Interlife, which include cash, real estate, and financials, amounting to 250m, the historic return on these assets has been only 2.5% (3.38% if we exclude the historically bad bond market of the previous year). If we multiply 0.025 by 250m, we get 6.25m in investing profits. Adding these two together, we have a conservative estimate of 11.35m in earning power. This implies a PE ratio of roughly 6-7 and a ROE of 10%. Not bad but I believe these assumtions are very very conservative.

Interlife has a historical combined ratio of 84%, and the higher combined ratio experienced last year was primarily due to inflation in the cost of paid-out losses. It's worth noting that Interlife has shown a growth rate of 17% in premiums for 2023, while the Greek insurance industry as a whole grew at 10% (compared to historical growth rates of 2-3% per year). This suggests that insurance costs are being adjusted significantly for inflation in Greece, further highlighting the uncompetitive nature of the industry. Given the uncompetitive nature of the Greek insurance market and Interlife's significant cost advantage, it is plausible that they can maintain a very good underwriting ratio of around 85% for a prolonged period. This would result in underwriting profits of 0.15 * 85m = 12.75m. Considering the low bond yields experienced throughout Interlife's operating history, assuming they can earn 4% on their earning assets does not appear overly aggressive. Their portfolio consists of a mix of government bonds, corporate bonds, shares, and some real estate (mainly hotels in Greece). Thus, we estimate investment profits of 0.04 * 250m = 10m. Combining the underwriting and financial profits, we arrive at 12.75m + 10m = 22.75m. This implies a PE ratio of roughly 3 and a return on equity (ROE) of 21%.

Just to have some fun, let's explore what Interlife could potentially earn in a year where volatility works in their favor. With Interlife's best non-COVID combined ratio of 78%, estimating 0.22 * 85m gives us 18.7m in underwriting profits. Additionally, Interlife has experienced years with financial returns exceeding 6%. If we calculate 0.06 * 250m, we arrive at 15m in estimated investment profits. Combining these figures, we get a total of 18.7m + 15m = 33.7m. This would mean you could wake up to this being a PE of 2. So you can say, like Buffett with Western Insurance, you bought a perfectly fine insurance company at the ridiculous PE of 2.

Valuation, The Davis Double Play

I cannot tell you exactly what Interlife is worth, but considering its conservative earnings power of 6-7 times and even 3 times my base case, along with its growth potential and ability to redeploy capital at attractive rates, I believe it should trade at a premium to book value, despite being a Greek financial company. Additionally, given its great underwriting profits, the PE ratio might be a better value metric.

Using the conservative earnings power of 11.35m and a multiple of 10x, the company would be worth 113m, representing about 1x book value and a potential 50% upside. If we use 10x my base case earnings of 22.75, the value would be around 230m, or 2 times book value, offering a potential 200% upside. It is possible to stretch the PE ratio even further, but that is not necessary to demonstrate that this stock is incredibly undervalued.

The real magic starts to happen when you consider earnings power as you project further into the future. If Interlife keeps compounding book value at a 15% rate over 10 years, we would reach an equity value of 457. Given its cost advantage compared to the competition, I believe it is reasonable to expect Interlife to still produce a 15% return on equity (ROE). This would give us an earning power of almost 70 million at a price-to-earnings (P/E) ratio of 10. Considering the company's compounding potential over 20 years, this P/E ratio would still be quite low. Therefore, we can estimate a value of 700 million, which is nearly 10 times today's price. This demonstrates the wonders of a Davis Double Play, where earning power improves and the multiple expands as well.

Good post. Interesting!

Stock performance might have to do with starting point (low valuation with IPO during crisis).

Fundamentals look strong, but my question arising from high profitability and not many employers and neither being one of the big players: are past earnings real (expected earnings) or too high, in the sense nothing happened to insured ships? ==> What are earnings (tomorrow) if sth happens? Do they make (good) use of re-insurance?

Greek, very high insider ownership. Why is such a small business listed?

Thessalie region has been devasted by historical flooding in early september. Interlife should be in the forefront as this seems to be close to their headquarter in Thessaloniki.

Share price has dropped. Worth to keep on watch list for potential second drop when they'll issue 2023 H2 financial results !