Monnari Trade a Polish gem

Asset play or turn around?

Monnari Trade Long

Company name: Monnari Trade S.A.

Ticker: WSE:MON

Price: 4,70 PLN

Market Cap 127 PLN million (29.08 USD million)

Disclaimer

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

Notes on this write-up

This article builds upon my previous submission for a stock competition for students hosted by Edwin Dorsey on his Bear Cave Sub-stack. It provides additional insights on recent financial quarters and delves deeper into the analysis.

Thesis summary

Monnari Trade is a small Polish company that has a market value lower than the sum of its current assets minus its total liabilities, and has had positive operating profits over the last decade, excluding the impact of the COVID-19 lockdowns. Monnari Trade's stock currently trades at a steep discount, with a 46% gap between its current market value and book value. The company also has a low price-to-earnings ratio of between 4-5. The management of the company has also taken an unusual step by showing willingness to buy back shares, which is not common in Poland. With multiple potential catalysts, the stock can easily be a multi-bagger within 2 to 3 years while having strong downside protection.

Company Overview

Monnari Trade is a women's clothing company headquartered in Poland that caters primarily to women over the age of 30. The company has a total of 244 stores, which includes 189 Monnari branded stores, 25 Monnari franchises, and 30 Femestage stores. Miroslaw Misztal, the CEO and founder, owns more than 30% of the company's shares. Despite experiencing consistent revenue and gross profit growth since 2014 (excluding covid), when Monnari Trade reached an operating income peak of 31.78 PLN million, the operating margins have declined from 16.7% in 2014 to 4.7% in 2019, resulting in a drop in the company's stock price. Nevertheless, Monnari Trade has reported profits every year since 2012, which raises the questions regarding the allocation of these profits.

Capital Allocation

he answer to the question is twofold. Firstly, the company has been returning capital to shareholders through dividends and share buybacks. Capital returns began in 2016, with a dividend of 6 PLN million and a similar-sized share buyback. The buybacks were conducted at prices that were nearly double the current price, and continued until 2020. Over this period, Monnari Trade repurchased 15% of its total shares. This is noteworthy as share buybacks are uncommon in Poland, even with a 19% dividend tax, which highlights the company's management's skill in allocating capital and their belief that the company is undervalued.

Secondly, a bigger factor to today's undervaluation is the company's strategic real estate investments. Monnari has retained a significant portion of its earnings and invested them into a real-estate project. The main investment is a 10.5 Ha piece of land known as the Geyer’s Gardens that was purchased for PLN 11 million in 2015, which was filled with rundown historic industrial buildings. The company has used excess cash to redevelop the industrial buildings on the lot into shopping and office space. Since 2015, Monnari has invested a total of 68.58 PLN million into real estate, including the initial cost of purchasing the lot.

The value of Monnari Trade's real estate investments has begun to materialise, with the company selling a portion of its undeveloped land in Geyer Gardens for 85 PLN million net. Monnari received 70% of the proceeds from the sale, as a portion of the investment property was sold to another firm called KBM Invest. This resulted in a cash inflow of 59.5 PLN million for Monnari. Additionally, the sale also included the settlement of debt owed to Monnari by KBM Invest, resulting in an additional 14.76 PLN million in cash. In total, Monnari received 74.26 PLN million in cash from this deal, which represents about 60% of the company's market capitalization. According to the company's H1 2022 report, the remaining portion of the Geyer Gardens is also finished and ready to be leased or sold. This remaining part is currently recorded on the books at 78.5 PLN million, however, it is likely worth much more as it is of similar accarage to the part already sold but contains already developed buildings.

Management's goal for real estate investments has been to achieve a 15% annualised return, and based on the current value of the investments exceeding 150 PLN million, it appears that this goal has been met. Additionally, the company's history of significant buybacks and cost-cutting measures during the COVID-19 pandemic further instils confidence in their ability to generate value for shareholders in the future. This fact is further underlined by book value per share compounding at a 16.1% rate since 2011.

Since receiving most of the proceeds from the sale of the land in Q2 2022, Monnari Trade has used some of its cash to grant a 6 PLN million loan yielding 8% that needs to be repaid by 2024 to another public entity in Poland, Rank Progress SA. Management has also stated in interviews that they might buy another entity. Under normal circumstances this could easily be accretive given the cheapness of the Polish market. However, given the cheapness of Monnari Trade a buy back would likely be even more accretive. The stock does right now suffer from being very small and illiquid so increasing the market cap might still drive value for shareholders although not from a fundamental perspective. Buying another company at the wrong price is, however, clearly the largest risk in the stock currently.

Valuation

To come to a proper valuation of the company I will do a quick sum of the part analysis. As stated above the clothing business has been somewhat troubled over the last few years with revenues and gross profits growing but operating margins strongly declining. This trend might, however, finally be reversed as a lot of cost-cutting in SGA was done during the corona pandemic. Much of this reduction is from reduced corporate overhead and some is from renegotiating renting agreements. In H1 2022 the operating segment of Monnari trade produced 12 PLN million in earnings or an operating Margin of near 10%. This is even more significant if you consider the operating margin tends to be much better for clothing stores in H2 given the better profitability of fall and winter clothing. If we assume the operating segment will be slightly more profitable in H2 then H1 25 PLN million in operating profit for the full year 2022 is easily achievable and even conservative. If we assume a similar gross profit to H2 2019 with the current cost structure the operating profit for H2 2022 could be as much as 30 PLN million for just the half year or 42 PLN million for the full year.

Monnari's target market is women over the age of 30, which makes the business less influenced by fashion trends and more predictable. However, considering the company's past challenges with managing costs, I do not think a high valuation is appropriate. A conservative estimate would be a multiple of 6 times EBIT. However, if the company can maintain cost control and expand its store network, it could warrant a more typical multiple of 13 times EBIT.

The operating business of Monnari appears to have an average of 20 million PLN in cash on hand. When considering the excess cash and financial instruments, the total amount is approximately 66 million PLN. Additionally, it is likely that Monnari has earned a significant amount of cash in the fourth quarter. A conservative estimate would add 15 million PLN to the current cash pile, assuming no reduction in inventory. This would bring the conservative cash total at the end of the fourth quarter to 81 million PLN. The remaining real estate is valued at 78.5 million PLN according to book value, but it is likely worth more. By considering the value of the land sold and the amount invested in redeveloping the old buildings, the value could be closer to 100 million PLN. Adding the remaining real estate to current assets we come to a current assets of 279 PLN million at the end of q4.

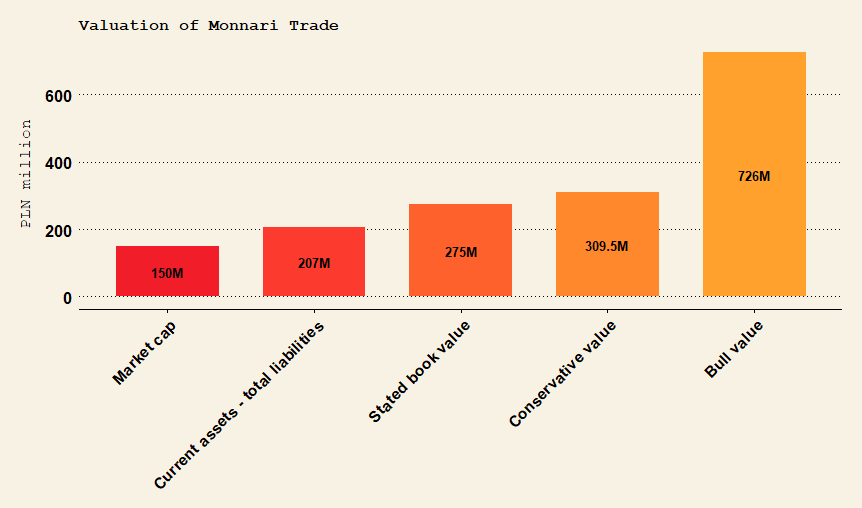

Here are the different ways to value to company:

Market Cap 150 PLN million

Downside scenarios

Current Assets - total liabilities 279-72 207 PLN million Stated book value 275 275 PLN million

Conservative value

Clothing business at 6x EBIT 6x25 150 PLN million

Excess cash and financials 81 81 PLN million

Remaining real estate Stated book 78,5 PLN million

Total: 309.5 PLN million

Bull value

Clothing business at 13 EBIT 13x42 546 PLN million

Excess cash and financials 81 81 PLN million

Remaining real estate 60 + 40 100 PLN million

Total: 726 PLN million

This investment can offer a very attractive return based even on liquidation value and a fairly extreme return of the Bull case plays out. Given the amount of downside protection inherent in the stock at current prices waiting to see how the operating business performs should not be too risky. One should further note that all these valuations are conservative in the sense that they do not factor in buybacks. The company currently has enough cash equivalents to buy back 64% of the shares or all of the shares if the remaining real estate is sold. If the company executes buybacks at attractive prices the laws of financial alchemy say this stock should go to the moon.

You mentioned: "Capital returns began in 2016, with a dividend of 6 PLN million and a similar-sized share buyback."

Has the CEO or press releases mentioned any dividend for 2023-2024?...it appears neither buybacks nor dividends have occurred from 2021 to 2023 present date.

A potential red flag could be lending out money, at an interest rate which is probably not considered high in Poland, given thaty it is not a financial company....?