Zombie Walking or Phoenix Rising: The possible Resurgence of Two Companies

Lee Enterprise and Barnes & Noble Education - Two Left-for-Dead Equity Stubs, I'll Be Watching Closely.

Introduction

Today, I'll be discussing two equity stubs that I've been monitoring for a short while. Currently, I don't own any shares of either company, but I'll be keeping a close watch on developments for both firms. Positive changes in their stories could lead to substantial gains and a phoenix-like resurgence, given both of them trade on back of the napkin math future PE’s of 1-2. Alternatively, the rollercoaster ride of tracking these two "falling knives" could provide an entertaining experience as these zombies could keep walking for a long time due to the structure of their liabilities.

I've chosen to write about Barnes & Nobles Education and Lee Enterprises together due to their shared characteristics:

Local Pseudo Monopolies:

Both companies exhibit characteristics of local monopolies within their respective markets.

Transitioning Legacy Business Models:

These companies previously sustained declining legacy business models that once generated stable cash flows. These funds were vital for their transformation into more modern, digitally-driven enterprises, as well as for managing debt-related expenses.

Accelerated Decline due to the Pandemic:

The decline of their legacy business models was expedited by the adverse effects of the pandemic.

Inseparable "Good-Co Bad-Co" Dynamic:

These companies display a unique dynamic where the positive and negative aspects of the business are intertwined and are challenging to separate.

High Debt Load Relative to Equity Value:

Both companies carry a substantial debt burden that far exceeds their equity value. This places their equity in a subordinate position to sizable debt obligations. Both stock potentially trade below 1x unlevered free cashflow.

Unique debt situation that give the companies more time to adjust than one would expected.

The debt situation of both companies is surprisingly more manageable than initial impressions might suggest. Creditors have extended more favorable terms than anticipated upon a cursory review of recent financials. This unique scenario provides these companies with a more lenient timeframe to make necessary adjustments.

Legacy boards and management teams with a history of poor value creation.

Both companies are burdened with a team that have demonstrated a lackluster track record over an extended period. There's significant ambiguity surrounding their capability to successfully guide the transition towards a more technology-forward approach.

Past VIC Write-Ups:

Both firms have been the subject of multiple high quality VIC (Value Investors Club) write-ups, although none have (yet) yielded substantial gains for long-term investors.

downturn of over 70% from their recent highs within the past two years.

Both companies have undergone a significant decline. While they once basked in periods of optimism, this hopeful sentiment has since given way to a state of complete despair.

Barnes & Nobles Education (BNED)

BNED is the education-focused subsidiary spun off from Barnes & Noble, the bookstore chain. The company operates both physical and virtual bookstores for college and university campuses, as well as K-12 institutions across the United States. Currently, BNED boasts 1,366 stores and reaches over 6 million students. Historically, this business was quite profitable with limited competition. Each campus store typically had only one major player, creating a nice and predictable economic environment due to their local monopoly status.

However, in recent times, this core business has encountered several challenges. University textbook prices have significantly outpaced inflation, prompting more and more students to seek alternatives such as second-hand books and digital piracy. The pandemic dealt a severe blow to BNED, as the absence of students on campus resulted in substantial losses. The pandemic also appears to have accelerated the trend toward piracy. Initially, BNED seemed like a classic retail reopening play, but even after the pandemic, the company continues to grapple with financial losses.

However, there is hope in the form of "First Day Complete" (FDC), which BNED refers to as their "equitable access program." In reality, FDC represents a superior business model where instead of leaving book purchases to individual students, the books are included in the course fee and rented out to the students, either in digital or physical form. This model is opt-out by default, meaning that all students in a course are automatically enrolled, and only a very few decide to opt out. The model offers lower pricing compared to traditional book sales, but its significantly higher sell-through rate results in better overall economics. With their most recent cohort of schools that have adopted this model, they've shown an impressive 82% increase in revenue and a 96% uptick in gross profit compared to the previous year.

Currently, the company operates 1,289 campus stores, after closing 117 unprofitable ones last quarter. In the last quarter, 157 stores were using the FDC model, which is more than 10% of stores following the initial trials that began in 2019. These stores also serve approximately 800,000 students out of their total 5.8 million.

The FDC program has shown impressive growth, and there's still room for further expansion. I believe there's a decent chance of a cascading effect, where many college campuses observe the success of the initial adopters and start switching to this model simultaneously. The FDC program seems to benefit most of the important stakeholders. Colleges can offer a discount to their students, and students have all their course materials on day one, a convenience that is often lacking. This has led significantly improved academic performance at colleges that have adopted FDC, something that college board care a lot about. Most importantly, if successful, FDC could eventually reduce the second-hand market as it reduces the supply of newly printed books, which is a significant advantage for the three major publishing houses dominating the textbook printing industry.

Regarding the students, the benefits of the program might seem somewhat limited to them. It offers convenience and is generally cheaper than buying new textbooks, but it might still be on par with purchasing the ebook version and probably more expensive than some second-hand books. Of course, it's more expensive than pirating, albeit slightly more convenient. However, it's crucial to note that the decision to switch to these models lies with the colleges, not the students. So, the fact that it's a positive move for colleges is the most important, along with the benefits for the publishers, who also play a crucial role in making this model work.

Okay, let's perform some quick back-of-the-envelope calculations. If BNED manages to convert an additional 50% of their colleges to the FDC model over time, this could lead to roughly a 50% increase in gross profit. This projection is based on the fact that FDC schools generally yield roughly double the gross margins.

This would mean a total gross profit of approximately $520 million once this target adoption rate is reached. Importantly, this transition to FDC doesn't significantly increase operating costs, and in fact, the company is actively working to reduce costs. We can use the current operating cost structure of $392 million. As a result, the stock could potentially generate around $130 million in EBIT (Earnings Before Interest and Taxes) at a 60% adoption rate for FDC. This outcome appears quite achievable, given the benefits the FDC model offers to important industry stakeholders

Okay, so why is this stock trading at such a low price, even though it's evident that it has the potential to consistently reach its own market capitalization within a year in the future? Well, the primary reason is the substantial debt burden carried by the company, which is currently operating at a loss, placing it in a challenging financial position. As I mentioned earlier, the post-COVID recovery didn't go well for BNED. Colleges experienced reduced enrollment and lower physical attendance. Additionally, BNED used to generate significant revenue from second-hand books, which they sourced through physical buyback events on campuses. However, due to the absence of such events in the last two years, this segment of their business failed to generate any profit, despite its usual importance to the company.

Before the pandemic, BNED had a relatively healthy balance sheet, with a significant amount of current assets due to the large inventory of books. They often delayed payments to major publishers until the books were sold, resulting in a substantial portion of current liabilities. The remaining working capital needs were typically financed with debt, including the use of a revolver to manage seasonal working capital requirements, especially during the fall rush at the start of the school year.

However, due to losses incurred during and following the pandemic, the debt has significantly increased, as have accounts payable to their suppliers. As a result, the balance sheet is currently in the worst condition it has ever been. Equity has declined from $450 million pre-pandemic to a mere $81 million in the last report. Debt has surged from $130 million to $270 million, and accounts payable have risen from $186 million to $275 million.

Considering recent performance and the strained balance sheet, BNED appears to be a prime candidate for bankruptcy if they do not take effective action within the next year and a half. The company has undergone numerous credit agreement amendments over the past years, with the latest being the eighth. Currently, they have two sources of liquidity: a credit facility with Bank of America and a term loan with TopLids LendCo ($30 million), LLC, and Vital Fundco. Of these, the most significant is the credit agreement, given its larger size and its critical role in sustaining the company's operations.

Presently, BNED can borrow up to $380 million under the asset-backed revolving credit facility and $100 million under the FILO facility. The current borrowings stand at $250 million under this agreement. Through amendments to the debt agreement, the maturity date has been extended multiple times, with the current end date set for December 2024. This extension is crucial because it provides the company with two fall-rush periods to demonstrate profitability, which I believe is essential for securing the refinancing of this agreement.

Previous amendments mandated special events, such as the sale of the digital student solutions part of BNED last year. Under the latest amendment, the appointment of two new independent board members was required to assist the company with strategic alternatives and restructuring. These individuals will ensure that the debt holders are somehow compensated. Possible courses of action include the sale of the wholesale business, an equity raise, or the company's reduction of expenses while simultaneously improving gross profits to achieve sufficient cash flows.

I'd like to highlight another crucial point: BNED serves as an intermediary between various players who can contribute to its survival. Firstly, publishers require a channel to sell books to students, and they generally have a dislike for Amazon. Therefore, they likely have an interest in keeping BNED afloat and might be willing to offer very generous payment terms. Secondly, the store leases with most colleges are more revenue-sharing agreements rather than classic lease terms. If BNED can't operate profitably, colleges will face even greater losses when running these stores themselves. This situation provides room for BNED to negotiate better revenue-sharing agreements with colleges (although the closure of 117 stores doesn't bode well in this regard). Lastly, Fanatics and Lids, which have taken over BNED's emblematic merchandising and acquired a stake in the company, have a significant incentive to sustain the current company. They've already loaned BNED $30 million and offered a higher percentage of emblematic sales for the coming year. So, there are various levers that BNED can utilize to improve cash flows.

Currently, management is guiding for $40 million in adjusted EBITDA for the current fiscal year. To me, this appears to be roughly breaking even or even incurring a slight loss. The real question will be whether they can achieve the right cost structure and acquire enough new FDC customers to generate strong cash flow by the fall of 2024. I will be closely monitoring a few key factors with this stock to determine if I can become more comfortable with this story:

Cost Reduction: Even with FDC growth, cost reductions are necessary to make this story work.

FDC Growth: Given the significantly better economics of FDC, it's crucial to improve cash flow.

Special Events: The potential sale of the wholesale business or an equity raise could also improve the balance sheet. However, this depends on the terms and conditions involved.

Credit Agreement Amendments/Extensions: Any further amendments or extensions of the credit agreement will be important to watch.

As of now, I do not own the stock, and I will only be monitoring the story. For the time being, BNED appears to be in a sea of trouble with no clarity on whether they can emerge successfully. I somewhat strongly recommend against owning the stock at the moment and suggest conducting very thorough due diligence if you consider buying it, as there are many moving parts not all covered in this write-up, and the debt level poses a very obvious risk.

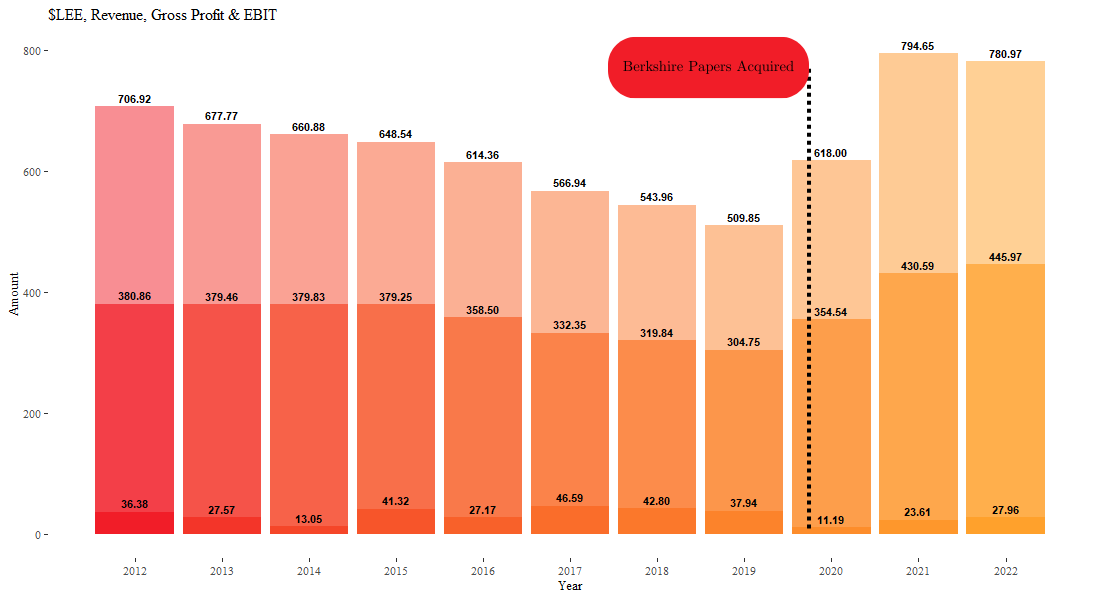

Lee Enterprises inc. $LEE

Lee Enterprises owns 77 local newspapers in mid-sized communities across 26 states in the US. Any value investor would recognize the historical success of local newspapers, exemplified by Buffett's ventures into buying local papers, including the well-known Buffalo News, now owned by LEE (more on this later).

However, with the advent of the internet, the landscape shifted, and most newspapers transformed from cash-flowing monsters with quasi-monopoly status to rapidly declining assets. Many value investors have attempted to capture these falling knives. So, why write about this now? Local newspapers have finally, albeit mildly, adapted to producing attractive and profitable digital offerings. Lee Enterprises is no exception to this trend, showing a significant and fast-growing digital revenue component in their business.

Lee's physical print business has experienced a prolonged decline, only somewhat offset by a significant acquisition at the beginning of 2020. In early 2020, Warren Buffett bid farewell to his beloved yet financially draining newspaper business by selling all of Berkshire's remaining newspaper assets to LEE. As part of this departure, he also refinanced LEE's debt at remarkably favorable terms. Buffett refinanced all their debt with a fixed 9% loan that has a 25-year maturity—yes, you read that correctly, 25 years. Although the 9% yield might appear high, it's actually lower than the yield on LEE's previous debt. Considering the remarkable duration risk involved, I believe this was a sweetheart deal. Moreover, this debt comes with very few covenants. There are no performance or debt-to-EBITDA covenants, only a cash sweep provision that kicks in once there's more than $20 million in cash on hand.

This debt structure makes LEE particularly intriguing. Despite its high leverage, the combination of the extended maturity and the limited covenants provides the company with much-needed flexibility and time to execute its strategy. Additionally, the cash sweep feature ensures that any excess cash will primarily be directed toward reducing debt at a yield of 9%, which is a favorable outcome.

What adds to the appeal is that many of LEE's revenues should, to some extent, track inflation, particularly subscription and advertising revenues. Furthermore, the current EBITDA is roughly equivalent to the market capitalization, making the stock look like a highly compelling opportunity.

Lee is on the cusp of transitioning from a period of decline to one of growth. Currently, digital revenue accounts for 38% of their total revenue and has been experiencing rapid growth. Interestingly, digital advertising revenue has already reached the same level as physical advertising revenue, highlighting the well-known fact that digital advertising is far more effective.

However, it's worth noting that Lee's approach to targeting digital ads doesn't seem particularly sophisticated. This indicates that there is ample room for improvement in the targeting of their digital ads, which could potentially result in higher revenues.

Also, there seems to be a lot of nascent price power in the digital subscription side of Lee, as monthly digital subscription ARPU is only $7.8, but print subscription ARPU is $53.3. This is, of course, because Lee is still trying to get people to switch over; however, there is very little reason for this price gap to stay this wide, as digital is arguably a better product.

In the last twelve months (LTM), the company recorded $720 million in revenues and $420 million in gross profit, both down approximately 10% compared to the previous fiscal year (FY22). This decline was primarily due to a slightly faster contraction in the print business than expected and a weak local advertising market.

The company did manage to generate $50 million in operating income; however, this was offset by the $42 million in interest expenses owed to Berkshire and $11 million in Merger & Restructuring Charges, along with $14 million in asset write-downs. This resulted in negative earnings from continued operations.

We should also consider adjustments, such as depreciation and amortization, which amounted to $30 million, compared to only $7 million in capital expenditures and $8 million in lease expenses. This, in fact, translates to $15 million in cash flows (equivalent to a quarter of the market capitalization). Unfortunately, due to certain working capital movements, this cash wasn't used for debt repayments.

Looking ahead, we can reasonably expect the company to significantly reduce its debt in the coming year. As merger and restructuring charges decline, especially as they complete cost-cutting initiatives at Berkshire newspapers, there will be improved financial performance. Additionally, there is substantial goodwill and other assets that can be written down to minimize taxes, including offsetting the outsized depreciation charge.

The company has also announced its intention to sell non-core assets, with $30 million identified and $5 million already sold last year, indicating a potential $25 million in cash generated from these sales over the next 1-2 years. Management has claimed to have implemented significant cost reduction measures as well.

This is quite interesting because it appears to be the first stock that now trades at the newly created multiple known as "marcap/cost savings" of less than 1. I'd like to delve a bit more into how these cost savings translate into bottom-line results, but it does seem to set up an attractive scenario for the stock.

However, the success of this story largely hinges on how they manage the decline of the print business and the effective monetization of the digital side. Therefore, I'm not entirely comfortable just yet. These are the key elements I'll be closely monitoring:

Print revenue decline.

Cost reductions and management.

Digital subscriptions & ARPU

Digital revenues.

Monetization of non-core assets.

Debt paydown.

I still don't own the stock, but I'm incredibly interested in this story and will be keeping a close watch on it.

Concluding remarks

I would like to emphasize once again that this article offers a simplified overview of both situations, primarily designed to bring attention to them. Both cases involve even more complexities and details than I've covered in this article. If you're interested in these stories, I strongly recommend conducting your own due diligence. There are numerous comprehensive write-ups on both situations available on Value Investors Club (VIC), as well as insightful podcasts on Lee Enterprises.

I spent a lot of time on BNED but sold about a year ago. if you want my thoughts, I'm at mikekruger94 (@ google mail )

Thank you very much that opt out situation seems really interesting!