Anexo Group, The Stag Hunt

A Deep Dive Into the Anexo Deal & Fair Value

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

Introduction

Today, I want to tell you about a stock trading at just 0.3x book and 3x earnings, with a 10-year book value CAGR of 15%. And yes—even better there is a live catalyst in play, in the form of a Stag Hunt Game. Okay, you got me—you read the title it’s another article on Anexo Group PLC. The UK-based credit hire legal firm now facing a takeover attempt from its founders and a major shareholder.

If you’ve been following along, you’ll know I already wrote an article on how shareholders can protect their minority rights against this pernicious offer. If you're a current shareholder, I recommend starting there:

In today’s piece, I’ll take a deeper dive into Anexo’s business and financials, share updated thoughts on valuation ahead of any fairness opinion, and explain why the stock is now particularly compelling from a risk-reward standpoint—especially given the proposed deal and the growing pushback from minority shareholders.

Here’s what I’ll be arguing in this article:

Anexo has a much stronger business model than most other law firms and should command a premium valuation because of it.

The company’s accounting is conservative, which makes it a reliable and important anchor for valuation.

At the current share price, Anexo is highly undervalued, offering significant upside.

The buying consortium made a major mistake by lowballing shareholders with a loan-notes-only offer—this move has backfired by galvanizing shareholder resistance, increasing the likelihood of a better outcome.

Anexo Group, Understanding Fair Value

Understanding Anexo's Business Model

1. Credit Hire - The Core Engine

2. Legal Services - Bond Turner

3. Housing Disrepair

4. What Makes This Model Attractive

Financial Analysis

1. Income Statement

2. Balance Sheet

Business Lines and Accounting

1. Credit Hire

2. Legal Services

3. Emissions Litigation

3.1 VW Case Economics (Illustrative IRR)

4. Housing Disrepair

5. Putting It All Together

6. Accounting: Conservative but Misleading (in the right way)

6.1 Understated Earnings

6.2 Understated Book Value

6.3 Why Anexo’s Cash Return on Equity Isn’t Worse Than Stated ROE

7. The Final Verdict

Fair Value Estimation

1. Comparable Transactions

2. Valuation vs. Peers

3. Book Value-Based Valuation

4. Fair Value Range

The Strategic Error: Loan Notes

1. A Stag Hunt

2. The Endgame: Where Things Stand for Minorities and New BuyersUnderstanding Anexo’s Business Model

Let’s start with the first claim: Anexo has a business model that’s better than most law firms.

Anexo operates as a vertically integrated legal services and credit hire company. Its key strength lies in combining a broad, physical referral network with in-house legal capabilities and a sharp focus on client acquisition. While the business has expanded into several legal verticals, the model remains consistent: Anexo puts up capital upfront, and only gets paid once cases settle—often months or even years later.

The company officially reports three business lines, but I believe there are actually four distinct segments worth understanding.

1. Credit Hire – The Core Engine

Anexo’s foundation is credit hire. This typically involves low-income individuals—often motorbike or car drivers—who get into accidents that aren’t their fault. These clients usually can’t afford a replacement vehicle, and their basic insurance won’t cover the cost.

Anexo reaches them through a wide network of independent repair shops and mechanics across the UK. These local operators are crucial: when a driver brings in a damaged vehicle, the shop refers them directly to Anexo.

Anexo then:

Provides a like-for-like replacement vehicle (usually hired from third parties like Hertz),

Fronts the legal costs needed to recover the money from the at-fault party’s insurer.

It typically takes about 18-24 months1 to recover these costs, meaning Anexo carries the working capital risk for both the vehicle and the legal case. But this is also where the economic engine starts.

2. Legal Services – Bond Turner

The legal side is handled by Anexo’s in-house firm, Bond Turner. Alongside vehicle-related claims, they also pursue associated personal injury or health-related damages, which increases the total recovery per case and allows Anexo to capture more value from each claim.

2.1 Emissions Litigation (Reported under Legal)

Anexo used its existing database of vehicle-owning clients to enter emissions litigation. These cases target manufacturers like Volkswagen, Mercedes, and BMW for misleading customers on diesel emissions.

This business line requires heavy upfront investment—mainly in targeted marketing and outreach to sign up claimants—followed by what’s usually a multi-year legal process. Anexo indicates these cases should take 3-4 years2. The VW case defending 12,000 clients has already been settled successfully. The Mercedes and other cases are progressing well, with Anexo representing a portfolio of 37,00 claimants in their portfolio.

3. Housing Disrepair

Recent UK legislation has made it significantly easier for tenants in social housing to pursue legal action against landlords for substandard living conditions — including persistent issues like damp, water damage, and heating failures. This has created a new, growing legal segment, and Anexo has moved quickly to capitalize.

The company entered this space by reactivating dormant contacts in its CRM. Many former credit hire clients live in social housing, making cross-referrals both natural and cost-effective. In this way, Anexo was able to ramp the new business line without needing to build a costly sales infrastructure from scratch.

Critically, housing disrepair cases are far less capital-intensive than Anexo’s traditional credit hire or emissions claims. There are no vehicle hire costs and settlement times are much shorter — typically 6 to 9 months3. This makes the segment highly scalable, with fast cash conversion and strong incremental returns on capital.

Even more promising is the organic referral dynamic built into the sales model. Social housing tenants often face similar conditions within the same building or complex — if one tenant has black mold or persistent leaks, it’s likely their neighbors do too. When one person successfully takes legal action, others are inclined to follow. This word-of-mouth growth — “How did you fix your flat?” / “I used Anexo” — makes the segment unusually viral by legal industry standards.

In sum, housing disrepair represents a high-margin, capital-light, and fast-turnover business line that not only diversifies Anexo’s earnings but also strengthens its client acquisition engine — turning existing relationships into a repeatable, compoundable source of value.

4. What Makes This Model Attractive

There are several reasons this structure can be compelling from an investor’s perspective:

Limited price sensitivity: In the credit hire business, the party paying—typically an insurance company—is not the same as the party choosing Anexo. Similarly, emissions and housing clients are generally not shopping around based on legal fee comparisons. This provides Anexo with pricing flexibility and some insulation from competitive pressure.

Client inexperience: Many Anexo clients have never been involved in legal action before. Their primary concern is convenience and access to justice, not fee optimization. The role of trust—often through referral—is key, and this reduces the relevance of traditional price competition.

Standardized, repeatable cases: Unlike many listed law firms that rely on high-profile partners or bespoke legal work, Anexo focuses on high-volume, repeatable legal claims. This enables process-driven efficiency, scalability, and less dependence on individual talent or networks.

Combining these factors makes Anexo a structurally superior business model for public market investors. Most traditional law firms are optimized for insiders: they rely heavily on partner relationships to win bespoke, high-value cases. When these cases succeed, the partners—rightly—take a large share of the profits. In the worst-case scenario, however, these firms can unravel quickly. Both Rosenblatt4 and Ince Group5, two listed UK law firms, collapsed under this pressure. Notably, Seller and Moss—Anexo insiders—were significant shareholders in Ince and even attempted to rescue it with additional capital before it ultimately went into receivership6.

Anexo, in contrast, suffers from none of these vulnerabilities. It is not dependent on individual partners, and its business is both scalable and defensible. Rather than being lumped into the broad discount applied to most public law firms, Anexo’s unique model justifies a valuation premium.

This is the foundation for my first key claim:

Anexo has a much stronger business model than most other law firms and should command a premium valuation because of it.

Financial Analysis

So how does Anexo’s operating model translate into financial performance? Let’s take a look—starting with the income statement.

1. Income Statement

Revenue, gross profit, and operating income have all grown consistently over time. The only area showing some recent pressure is after-tax profit, mainly due to rising financing costs and the conservative accounting treatment of emissions litigation (more on that later).

2. Balance Sheet

Next, let’s take a look at how the balance sheet has evolved:

Anexo has a solid track record of compounding book value—driven by retained earnings, not dilution. While management is granted roughly 1% of the company annually in options, this is effectively offset by a dividend of similar size.

We also see that Anexo began taking on more leverage starting in 2021. This was primarily to fund emissions litigation, but also to deal with longer settlement times in the credit hire business post-COVID. That delay has tied up more working capital. Combined with rising interest rates, this has significantly increased the company’s financing costs in recent years and reduced ROE.

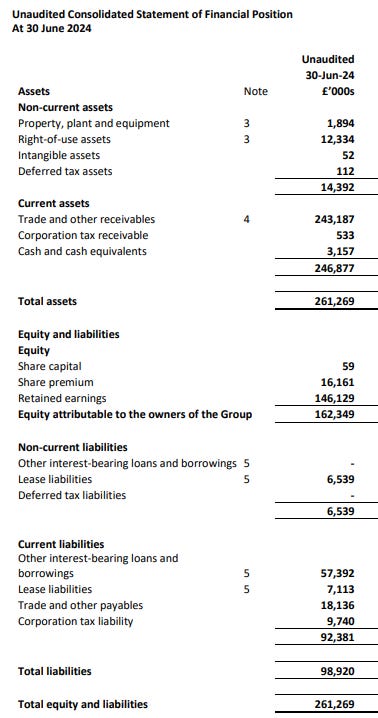

Looking at the most recent balance sheet:

Unsurprisingly, nearly all of Anexo’s assets are made up of trade and other receivables—claims that have been filed but not yet awarded. I’ll cover the accounting behind these receivables in more detail later, as it’s key to understanding the business.

On the liability side, Anexo currently carries about £57 million in interest-bearing debt and £162 million in equity—versus a current market cap of around £70 million.

Here’s the loan breakdown as of June 20247:

Invoice Discounting Facility: £27 million outstanding. (Interest rate not specified.)

Revolving Credit Facility (HSBC): £10 million current + £10 million non-current = £20 million total. Interest: 3.25% over the Respective Rate.

Blazehill Capital Finance Loan: £15 million outstanding. Interest: 13% above the central bank rate (currently 4.5%), so effectively 17.5%.

Shareholder/Similar Loans: ~£5 million outstanding. The disclosed shareholder loan carries 10% fixed interest, plus a share of any upside—other similar loans may vary.

As you can see, this layering of increasingly expensive debt—especially tied to the emissions litigation—has started to weigh heavily on the bottom line. The Blazehill loan, at 17.5%, is particularly aggressive. And while the litigation-related loans charge a lower fixed rate (10%), they also include upside participation, making them costly in the long run.

However, there’s been a positive development. In its H1 2024 report, Anexo noted that after the balance sheet date, the full Blazehill loan was repaid using a new facility from Callodine Commercial Finance. According to the company, this new facility provides additional headroom and significantly reduces the cost of capital8, a key step toward improving financial flexibility going forward.

Due to the way Anexo’s accounting distorts the cash flow statement, similar to a bank, I will not cover it here.

Business Lines and Accounting

Let’s now break down Anexo’s individual business segments and how each is accounted for. This is important, because Anexo’s financials—particularly profitability and book value—can only be properly understood when you understand how accounting differs across the business lines.

1. Credit Hire

The credit hire business9 has seen materially lower returns since COVID. This decline appears to come from a few key factors:

Higher interest rates — credit hire is working capital-intensive, and rising financing costs have eaten into returns.

Delays in the UK civil courts — court backlogs post-COVID mean cases take longer to reach a hearing date. Since insurers usually only settle once a court date is set, this delays cash recovery and extends the working capital cycle.

Accounting Treatment:

Revenue in credit hire is recognized daily over the hire period10. Then, it's discounted across the portfolio based on historic settlement experience. So while not overly conservative, revenue recognition here is cautious and grounded in real data. It reflects economic activity fairly, though working capital is still tied up for long periods, and one might need to do some minor adjustment to adjust for the fact these receivables do not have a time discount in them.

2. Legal Services

Legal services11 are the true profit engine of Anexo. The business is far more capital-light than credit hire and consistently earns strong returns on equity. Anexo’s model is clearly structured around sourcing credit hire claims that deliver acceptable ROEs—and then attaching legal services, which produce excellent ones.

This segment also includes emissions litigation (discussed separately below).

Accounting Treatment:

This is where things get significantly more conservative12:

Before admission of liability: No revenue is recognized at all, despite legal work already being performed.

After admission of liability: Revenue is recorded only at the minimum recoverable amount per court guidelines—excluding any uplifts or success fees.

At final settlement: Additional revenue is recognized only when cash is received, not when the case is won.

So even when Anexo has strong legal claims, if those cases haven’t reached certain legal milestones, no value is recorded on the books. This materially understates the true expected value of the legal pipeline.

3. Emissions Litigation

The emissions litigation is both a promising and accounting-distorting part of Anexo’s business. Here's why:

Anexo expenses all costs upfront (including marketing and legal)13, but

It cannot recognize revenue until a case is fully settled14, and

Once settled, confidentiality clauses often prevent detailed disclosure of profitability.

For example, Anexo has only been able to confirm that the VW case generated £7.2 million in net cash—after fully expensing all associated costs and after paying litigation funders15.

We can back into an estimate of the returns on this case:

3.1 VW Case Economics (Illustrative IRR)

Anexo Group’s involvement in the VW Emissions litigation spanned several years and involved substantial upfront investment in customer acquisition and legal marketing. While the company expensed these costs as incurred between 2019 and 2023, its 2023 annual report disclosed a key figure:

“The agreement had resulted in a net positive cash position to Anexo of £7.2 million.”

This statement was the basis for estimating the internal rate of return (IRR) to Anexo’s equity investment in the VW case. Here’s how we interpreted the available information and constructed a cash flow profile.

Interpreting the Financials

Anexo’s total cash investment in the VW case from 2019 to 2023 was £10.3 million16.

In 2020, the company secured a £2.1 million litigation loan with 10% annual interest. The loan was to be repaid upon case settlement17.

Interest on the loan accrued (PIK-style) — it was not paid annually but rolled up and paid in full in 2023, together with the principal and a share of the case proceeds.

In 2023, the company reported a £7.2 million net cash inflow18, after:

Paying that year’s £4.3m investment

Repaying the £2.1m loan

Settling all interest and success-based fees

This implies the total gross cash inflow from the VW case must have been at least:

£4.3m + £2.1m + ~£0.7m (interest) + £7.2m = ~£14.3m

I modeled the investment and funding structure as follows:

Using the equity cash flow profile, we calculate an IRR of approximately 19.6% for the VW emissions litigation. This reflects the return on the company’s net cash outlay over five years, leveraging litigation finance to reduce upfront equity risk.

A nearly 20% IRR represents a strong, risk-adjusted return on Anexo’s investment — particularly given the long litigation cycle and structured use of debt to amplify equity outcomes.

Anexo represented approximately 12,000 clients in the VW emissions case. According to its 2023 disclosure, the company reported a net cash inflow of £7.2 million after repaying litigation funders and covering all related expenses, including a final £4.3 million investment in 2023.

However, based on my analysis, the gross proceeds from the VW case were at least £14.3 million, once we account for:

Final-year investment (£4.3m)

Debt repayment (£2.1m)

Accrued interest and success-based fees (~£0.7m)

Net retained cash (£7.2m)

This suggests that the actual profit per claimant was closer to:

£14.3 million / 12,000 clients = ~£1,190 per client

With Anexo now managing approximately 37,000 active emissions claims across Mercedes, BMW, Citroën, Renault/Nissan, and Vauxhall, this could imply potential gross proceeds in the range of:

37,000 × £1,190 = ~£44 million

None of this future value is currently reflected on the balance sheet.

Importantly, none of this future value is currently recognized on the balance sheet. However, Anexo still carries approximately £5 million in emissions-related debt, which would need to be deducted to estimate true net value — bringing the adjusted figure to around £40 million (more than 50% of the market cap).

4. Housing Disrepair

Housing disrepair19 is Anexo’s under-the-radar gem: small, fast-growing, and with exceptional economics.

The company only started breaking it out in 2021, but it has more than doubled in size since then, boasting:

50%+ margins

ROE > 50%

Significantly better working capital dynamics than credit hire

Unlike credit hire, there’s minimal upfront capital deployment—mostly just legal costs—and settlements come through faster in 6-720.

Accounting Treatment:

Like other legal services, accounting here is conservative: no revenue is recognized until liability is admitted, and only baseline amounts are recognized until actual settlement and cash collection21.

5. Putting It All Together

The shift in business mix—especially growth in Housing Disrepair—should improve both margins and return on capital going forward. Meanwhile, the resolution of emissions litigation should unlock hidden value, simplify the balance sheet, and reduce reliance on high-cost litigation financing.

If the emissions cases settle as expected and housing disrepair continues to scale, Anexo could earn:

>15% ROE

With less leverage than today

And normalized after-tax earnings of ~£24m, assuming historical 30% operating margins, £9m in financing costs, and a 25% tax rate

At today’s market cap (~£70m), that’s ~3x normalized earnings. That’s remarkably cheap.

6. Accounting: Conservative but Misleading (in the right way)

Anexo is a unique company with a very particular accounting approach — one that investors need to get comfortable with. In my view, the accounting is actually highly conservative. I believe both reported earnings and book value (specifically receivables) are understated, especially during periods of growth. Let’s unpack why.

6.1 Understated Earnings

Anexo operates across four business lines (including emissions litigation), each with different capital and revenue dynamics. But all share a key accounting feature: costs are expensed immediately, while revenues are only recognized once a case is resolved, which may be months or years later.

This creates a significant mismatch between when costs are recognized and when the corresponding revenues appear — particularly during periods of expansion. In accounting terms, this departs from the standard practice of matching costs with the revenues they help generate.

For example, let’s say Anexo signs 1,000 new cases in 2024. It incurs upfront costs like vehicle rental, legal staff time, and client acquisition — all booked immediately. But the associated revenue may not be recognized until 2025 or even 2026. Meanwhile, the revenue that does appear in the 2024 income statement comes from a smaller base of older cases, initiated in 2023 or earlier.

This leads to a systematic understatement of earnings while the business is growing. It’s not a reflection of poor performance, but of accounting timing. In a flat business, the effect washes out over time. But in a growing business — which Anexo has been since listing — this creates a consistent lag between reported profit and actual economic activity.

6.2 Understated Book Value

The second area of conservatism is Anexo’s treatment of receivables across its business lines. Let’s go through each:

Credit Hire (Prudent, but Less Conservative)

Revenue is recognized daily over the hire period — but only after verifying that a third party is liable. Even then, receivables are discounted across the portfolio based on historical settlement rates and claim characteristics. This process avoids overstatement, the only layer of conservatism a investor might want to add themselves is to time discount these receivables.Legal Services (Clearly Conservative)

Here the conservatism becomes much more apparent:Before admission of liability: No revenue is recognized, even if legal work has been performed and value created.

After admission: Revenue is recognized only at the minimum recoverable amount allowed under court guidelines — excluding potential "success fees" or uplifts.

At settlement: Only then are these uplifts recognized, and only once cash is actually received.

This means that a large portion of legal cases (especially early-stage ones) generate no recorded revenue or receivables, even when their ultimate value may be substantial and reasonably predictable. The accounting errs strongly on the side of caution, understating the true economic value of the legal services business.

6.3 Why Anexo’s Cash Return on Equity Isn’t Worse Than Stated ROE

At first glance, Anexo’s free cash flow may appear weaker than its reported net income, which could lead one to question whether its cash return on equity is overstated. But there are two key reasons why this concern is likely misplaced:

Growth from Retained Earnings Shows True Return Generation

Anexo has grown consistently over time, scaling both revenue and receivables — without heavy equity dilution or excessive debt. That kind of compounding suggests the company is generating real economic returns on retained capital. If cash returns were substantially below reported profits, this growth wouldn't have been possible.Book Value Overstates Cash Invested

The equity base — particularly receivables — includes embedded profit margins. For example, in credit hire, Anexo books receivables at the rate charged to insurers, not the lower cost it pays to suppliers. This means that the book value includes margin, and the actual cash invested is lower than what appears on the balance sheet.

So while free cash flow may be modest due to working capital investment, that capital is being recycled efficiently. If you compare FCF to actual cash invested, and net profit to stated equity, both tell a consistent story: the business generates solid returns, whether viewed through a cash or accounting lens.

7. The Final Verdict

Taken together, the analysis above strongly supports the view that Anexo’s accounting is not only reliable but highly conservative. The company excludes meaningful upside from both earnings and book value by not recognizing case uplifts until settlement and by applying cautious assumptions throughout. The only potential criticism is that receivables are not time-discounted — but this is a minor point given the broader prudence in revenue recognition. Overall, this reinforces Claim 2:

Anexo’s accounting is conservative and provides a dependable anchor for valuation.

The company’s accounting is conservative, which makes it a reliable and important anchor for valuation.

Fair Value Estimation

As discussed earlier, Anexo is a unique business with a distinctive, high-quality model that makes direct comparisons difficult. There are no other publicly listed pure-play credit hire firms, and most listed law firms have very different operating models. These tend to be more capital-light — focusing on segments like housing disrepair — but they’re also much more people-driven and less systematized than Anexo.

In my view, that makes them less attractive. Their economics often depend heavily on senior partners, who can extract large sums and destabilize the business if disputes arise — as seen in the case of Rosenblatt. Anexo, by contrast, operates a scalable and more process-oriented model.

To support a fair value estimate — and mitigate claims of bias — I’ll walk through several valuation approaches. The simplest is a price-to-book valuation, which is likely how most investors will assess Anexo.

1. Comparable Transactions

Even though Anexo lacks perfect peers, there are several instructive transactions worth reviewing:

Direct Line (DLG) Takeover by Aviva22 – 1.5x Book

At first glance, this might seem like a stretch — Anexo is not an insurance company. But the underlying economics are surprisingly similar. Insurers collect cash upfront and hope to avoid payouts for a year or two. Anexo spends cash upfront and aims to recover a larger sum after a year or two. Both rely on judgment-heavy balance sheets and working capital cycles.Aviva acquired DLG at 1.5x book23. And that was for a business with lower returns (DLG’s historical ROE was ~10%), lower growth, and more leverage. Granted, this was a strategic acquisition — but it still illustrates that complex, capital-cycle-driven businesses with adequate returns should not trade below book.

DWF Law Firm Take-Private24 – 15–30x Earnings

DWF was taken private for £342 million. In the two years prior, it reported net profits of £12M (2023) and £22M (2022), implying a P/E multiple between 15x and 30x25. Importantly, this excludes DWF’s substantial debt (~£140M), which would push the EV/EBIT multiple even higher. The takeaway: well-managed legal firms can command strong valuations, especially when acquired outright.DBAY’s 2021 Attempted Takeover of Anexo – 1.5x Book

Perhaps the most relevant data point is DBAY’s 2021 takeover offer26: £1.50 per share, valuing Anexo at £175 million. At the time, book value was only £128 million — implying a 1.3x book valuation27. Notably, the board rejected this offer without hesitation.Since then, Anexo has added a new business line (housing disrepair), scaled its legal operations, and is approaching a potential windfall from emissions litigation. On that basis, a higher multiple than the DBAY offer is warranted today.

IPO Valuation – 2.0x Book

Anexo IPO’d in 2018 at £1.00 per share for a £110 million market cap. Book value at the time was just £75 million, implying a 1.5x multiple. This wasn’t a hyped tech IPO — this was Seller & Moss selling a partial stake to DBAY and the public. In both the IPO and the DBAY offer, insiders were only willing to transact at material premiums to book.

2. Valuation vs. Peers

Below I compiled a list of publicly listed pears.28

Across these imperfect comps, Anexo looks materially undervalued on almost every metric — especially P/B and P/EBIT. Yet Anexo has delivered the strongest 10-year ROE and better growth than any of the companies listed above.

3. Book Value-Based Valuation

To value Anexo on a book value basis, we first need to update for time. As of H1 2024, book value was £162 million — but we're now nearly 10 months beyond that. To estimate current book value (H1 2025), let’s project forward:

H1 2024 net income: £8 million

H2 is typically stronger, so assume H2 2024 net income: £12 million

Assume a similar £12 million for H1 2025

Projected current book value: £162M + £12M + £12M = £186M

That’s 2.5x the current market cap.

Now add the emissions litigation. If settlements total £40million in 2026, and we discount that back at 15%, the present value is ~£34 million. Including this:

Adjusted projected book value: £186M + £34M = £220M

That’s 3x today’s market cap

4. Fair Value Range

Even at 1x book, Anexo offers significant upside. But this would undervalue a business with:

A normalized ROE above 15%

Consistent reinvestment of earnings

No heavy dilution or excessive leverage

A 15% ROE business with moderate reinvestment should trade well above book. Valuing it at:

1.8x book implies a P/E of ~12

2.6x book implies a P/E of ~17.5 (UK long-term average)

Based on estimated book value of £220M, this implies a fair equity value between £396M and £578M — representing a 5.4x to 7.9x return on the current market cap.

A return of this magnitude is highly unlikely to be realised through a take-private deal, especially one structured around loan notes or unlisted shares. In contrast, remaining public preserves access to strategic optionality — including future monetisation of emissions cases, continued high-ROE reinvestment, and the ability for shareholders to benefit directly from any re-rating in valuation multiples.

Taken together, Anexo’s conservative accounting, strong historical returns, and deep undervaluation relative to precedent transactions all reinforce Claim 3:

At the current share price, Anexo is highly undervalued, offering significant upside.

The Strategic Error: Loan Notes

The buying consortium appears to have made a critical strategic misstep by proposing a loan-notes-only offer — a decision that has backfired by galvanizing shareholder resistance and significantly reducing the likelihood of a smooth transaction.

As discussed earlier, Anexo seems deeply undervalued. Any acquisition near current market prices would represent an attractive deal for the consortium. But rather than executing a straightforward and well-calibrated take-private transaction, the consortium overreached. By signaling their intent to pay shareholders with illiquid instruments — such as loan notes or unlisted equity — they triggered immediate backlash from shareholders.

Had the consortium instead tabled a standard cash offer, the shareholder base might have turned over to special situation or merger arbitrage investors, who are typically more willing to accept a modest premium for liquidity. Instead, the existing long-term shareholder base has remained intact — and is now demonstrably opposed to the likely terms.

Ironically, the consortium could have achieved a more favorable outcome by taking a subtler approach. For example, launching a cash tender offer followed by a delisting vote might have worked. With 63% of shares already under control, they would only need an additional 12% of shareholder support to reach the 75% threshold required for delisting. In that scenario, remaining minority shareholders would find themselves caught in a classic Stag Hunt Game — a well-known concept from game theory.

1. A Stag Hunt

In a stag hunt, two players can each choose to cooperate (hunt the stag) or act alone (hunt the rabbit). The stag provides the best reward, but only if both players cooperate. Hunting the rabbit is safe but suboptimal. In the context of Anexo, the stag represents holding out for long-term value, while the rabbit is tendering shares in the offer.

As the matrix illustrates, tendering offers a predictable but limited outcome. And because avoiding downside is a core investing principle, shareholders may choose to accept an undervalued offer simply out of fear that others will tender — pushing the consortium over the 75% delisting threshold and stranding non-tendering shareholders in an illiquid, delisted vehicle.

This dynamic is precisely why the consortium’s choice of loan notes was so damaging. It alienated minority holders to the point where they began actively communicating to protect their rights — a rare but powerful development in fragmented public markets. Such communication would likely never have occurred if a straightforward cash offer had been made.

Today, a growing group of shareholders — including a Twitter-based coalition representing approximately 15% of the register, along with an additional 6% known to oppose any coercive deal — brings the opposition to roughly 21%.

This 21% now forms a blocking minority. Under AIM rules, a delisting requires 75% of votes cast to be in favor. If the consortium’s 63% votes in favor, 21% votes against, and all other shareholders abstain, the outcome would be:

21/ (63 + 21) = 25% voting against

This is exactly what we need to block. This tally excludes some other large holders hence a larger group would be expected to vote against. Hence we satisfy claims 4:

The buying consortium made a major mistake by lowballing shareholders with a loan-notes-only offer—this move has backfired by galvanizing shareholder resistance, increasing the likelihood of a better outcome.

2. The Endgame: Where Things Stand for Minorities and New Buyers

So where does this leave the minority shareholders—or any prospective new investor today?

Given the level of shareholder resistance and the fact that some degree of communication among holders is now underway, it seems increasingly unlikely that the consortium can push through an exploitative deal. As such, they are left with two realistic options: either come forward with a genuine cash offer or allow the deal to collapse.

The “no deal” outcome presents a somewhat awkward scenario. It would leave Anexo publicly listed, but with 63% of the shares controlled by a consortium that has just experienced a standoff with its minority shareholders. This may seem unattractive to new investors. However, minorities are not without agency.

For instance, any shareholder or group holding just 5% of the vote has the power to call a special meeting to nominate a new board member. While such a nomination would still require majority approval, and thus support from either Seller & Moss or DBAY, this is not necessarily impossible. If Anexo remains a public company, the interests of DBAY, Seller, Moss, and the minority shareholders could become aligned. All parties would benefit from a higher share price.

It’s likely that Seller and Moss are frustrated that the value they've created is not being properly recognized. Meanwhile, DBAY holds Anexo in a legacy fund and has not yet exited the position, likely due to poor performance. With the bid failing—and any new attempt likely to meet similar resistance—the most straightforward path to unlocking value is for Anexo to succeed as a listed company.

For minority shareholders, this outcome is also clearly preferable. Electing a director backed by minority investors could serve as a symbolic truce and a signal of improved governance. In turn, this might act as a catalyst for a re-rating of the stock post-deal break.

All things considered, the minority—or any new investor—stands a strong chance of either receiving a more credible offer than loan notes, or benefiting from improved public market performance. With substantial opposition already in place, the downside risk of a forced delisting appears well protected.

Anexo Group Plc, H1 2023 Earnings Call, Aug 22, 2023, timing explained by comment from CFO.

Anexo Group Plc, H1 2019 Earnings Call, Sep 10, 2019, answer from Allan Sellers. It should be noted that the VW case took 5 years.

Anexo Group Plc, H1 2023 Earnings Call, Aug 22, 2023, timing explained by comment from CFO.

See Anexo H1 2024 Page 17 note 5 borrowings.

See Anexo H1 2024 Page 17 note 5 borrowings: “The Group has recently secured alternative funding from Callodine Commercial Finance LLC to repay Blazehill, provide additional headroom and which significantly reduces the overall cost of capital of the Group.”

More financial data on the Credit hire Segment:

See FY 2023 report, page 73 note on Revenue

More financial data on Legal Services:

See FY 2023 report, page, 67 accounting policies

Repeatably mentioned during transcripts

See FY 2023 report, page, 67 accounting policies

See CFO comment in FY 2023 transcript: “I'm not sure what accrued expenses mean. All of our costs were written off as incurred. So the GBP 7.2 million is, as we described in the note, the net cash generated from that particular settlement. And so I think lots of people are aware, we're bound by certain confidentiality rules around the VW settlement.”

This model is based on all mention of cost expensed for the emission cases.

2020 annual report

This is my interpretation of what the 7.3m inflow in 2023 annual report means.

More financials on Housing disrepair:

Allan Seller during 2021 earnings call

See FY 2023 report, page, 67 accounting policies

can of course be found in 2021 financials.

All valuation multiples are taken from TIKR.

Hi Iggy. A very clear discussion of the company. Thank you.

How do you think about the downside if the consortium manage to get 75% of the vote?

Well done on such a detailed write-up. I'm still not comfortable with the cashflow profile of Anexo. I'd disagee on your comment on the level of debt. From 2017 to 2023, the total liabilities tripled to £100m and the Cash from Operations over the same period totalled -£500k.

I get that they have a very long WC cycle as they're aggressively growing the business but at what point do shareholders get rewarded with reliable FCF. I guess the case for buying the stock will be if the Bond Turner side of the business grows big enough as this is the side of the business with better cashflows as you mentioned.