Eurosnack a fat pitch

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

Executive summary

Eurosnack S.A. is a little-known Polish food company that operates in the nano-cap market and has an extremely narrow public float. The company specializes in the production and sale of chips and cookies, primarily in Poland. Despite its remarkable growth over the past five years, the stock trades at a low price-to-earnings ratio of 6-8 due to its illiquidity and communication issues. In addition, the company's gross margins have been adversely affected by inflation. However, if Eurosnack can maintain even moderate growth and improve its gross margins to the levels seen in previous years, it should be a multibagger stock.

Product and strategy

Eurosnack specializes in producing a diverse range of snack products that can be divided into two main categories: Baked goods, which includes two types of cookies (sold under the Aksamitki brand) , and Salty Snacks, which includes Gluten-free Corn Puffs sold under both the Eurosnack brand (Maxi & Chrupcie) and private label. While the company does not provide segment data, it is likely that the Salty-Snack business accounts for a significant portion of its revenue and profits. This conclusion is based on the observation that the product range of the corn chips is larger, and they are more widely available through various online retailers.

Eurosnack's business strategy is to offer premium quality snack products at premium prices, thereby focusing less on price competition. The brand's reputation for quality and uniqueness is reflected in its multiple important certifications, particularly for its chips, which are certified BIO and gluten-free. Through my research on the range of chips offered by Polish supermarkets, I found that Eurosnack is the only brand carrying these trademarks. This gives the company a slight advantage as supermarkets want to offer such products, but it is not a niche that the other major players are seeking to fill. I think it will take very long before we see Cheetos market itself as a BIO Gluten free option. The pricing strategy is smart in my opinion due to the fact that the Polish chips market is dominated by large international players, such as Frito-Lay, which is owned by Pepsi. These big players are known to consistently raise prices each year, often above inflation, which allows Eurosnack to also increase its prices and maintain its gross margins of around 50%. Overall, I think Eurosnack's quality pricing strategy has been successful, and its consistent high gross margins serve as evidence of its effectiveness.

The management of Eurosnack has been vocal about their efforts to expand the product line and diversify the customer base, as the company was heavily reliant on certain customers in the past. At one point, the largest customer accounted for 70% of the off take, but this figure has dropped to 30% in the previous year. This is still a relatively high level of customer concentration, but it demonstrates the management's successful execution of their strategy. Additionally, the chips section now offers a wide range of flavors and products, indicating that the management team has made significant efforts in this regard. Overall, I believe that the management has identified the right strategy and has executed it well.

Core financials

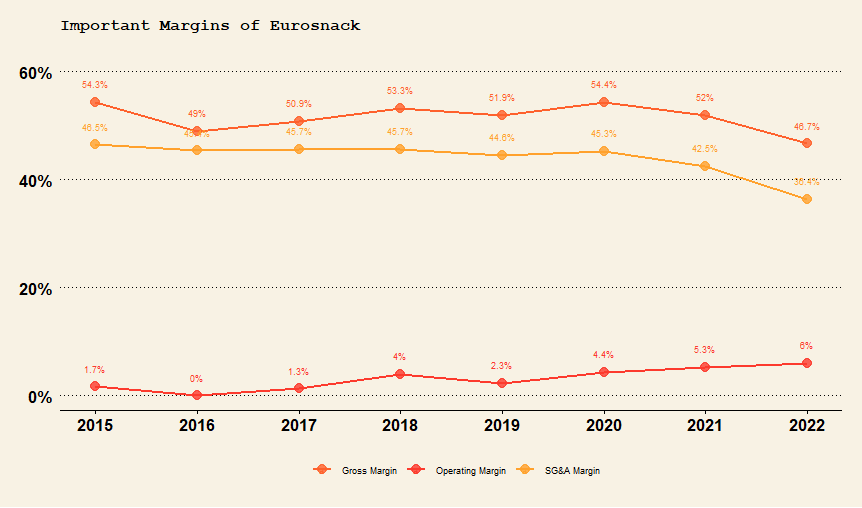

The approach outlined earlier has proven to be highly successful for the company in terms of financial performance in recent years. The company has achieved a Compound Annual Growth Rate (CAGR) of 40% in its revenue since 2014, and its gross margins have similarly progressed in tandem.

Starting from 2017, the company has demonstrated impressive operating profitability, with its operating margins growing at a faster rate than its top-line revenue due to the activation of operating leverage. This is evidenced by a year-on-year increase in operating margin, accompanied by a reduction in SG&A margin, indicating the management's effective cost control measures.

The graph above illustrates the effective cost control measures and increased operating margins mentioned earlier. However, it also highlights an intriguing observation: the gross margins have significantly decreased this year. This compression can be attributed to a sudden surge in the prices of the commodities used as inputs for Eurosnack's products, specifically corn and energy.

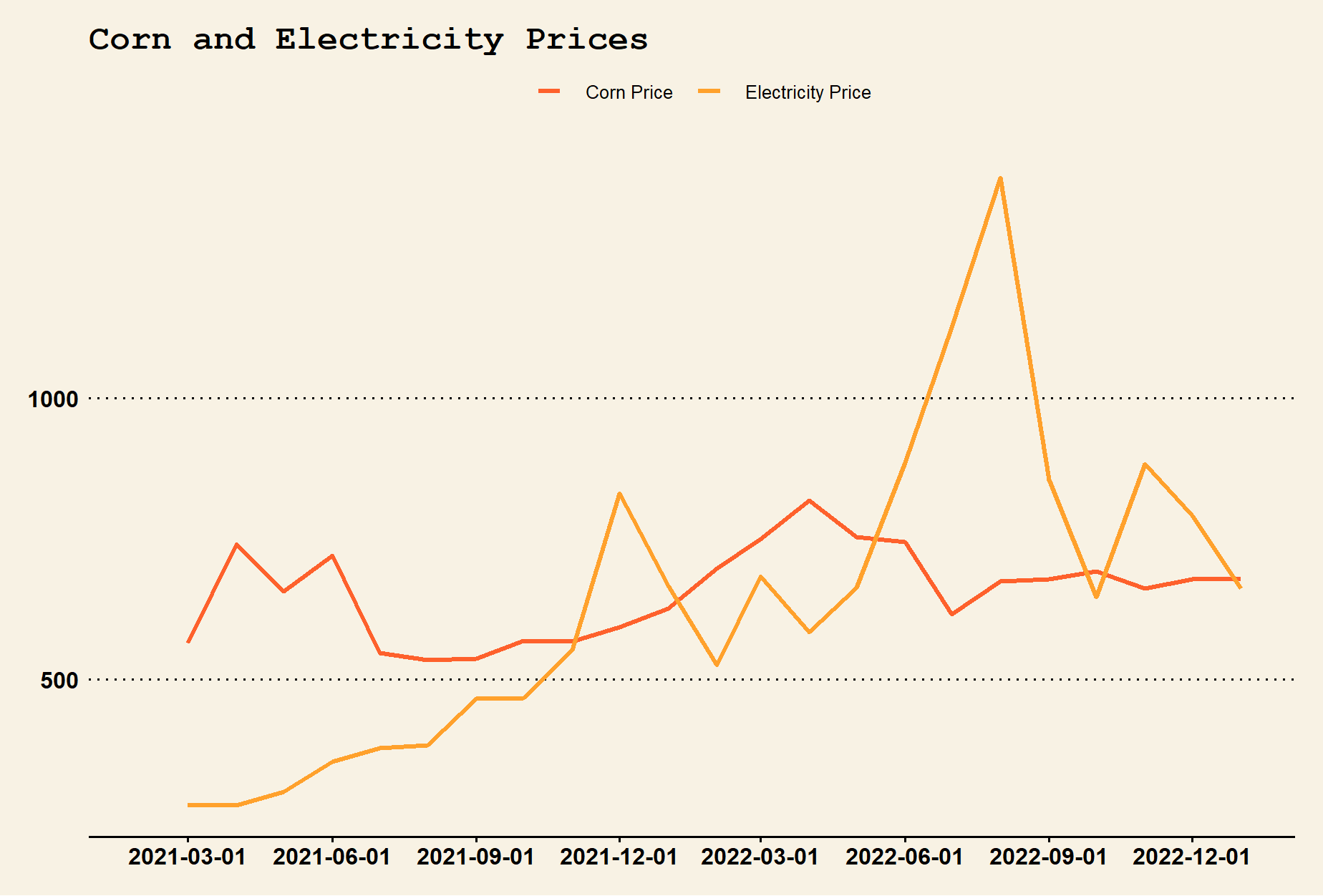

As we are aware, the global economy has experienced a significant degree of inflation in 2022. However, Eurosnack's business was especially impacted by the Ukraine conflict, which severely affected the country's corn production. Ukraine was the 6th largest corn producer globally, and corn prices have also risen due to increased fertilizer costs. Additionally, Europe has been grappling with an energy crisis following the reduction in Russian gas supply. Poland's energy supply primarily depends on coal, accounting for 71% of energy produced in 2020, with natural gas representing only 11%, and the remainder sourced from other sources.

Eurosnack typically maintains one-year fixed-price contracts with its customers and suppliers to ensure price stability in its store prices and input costs throughout the year. This business model is generally effective, as Eurosnack purchases commodities and sells branded goods, resulting in high gross margins (averaging 52% before 2022). However, the sudden and significant spike in inflation in 2022 resulted in the company being unable to maintain the same level of spread. Nonetheless, with the recent cooling of European energy prices and a similar trend in the corn market, I anticipate the company will once again achieve a similar gross margin within one to two years. An increase in gross margin from 46% in 2022 to 52% would result in an operating margin of 12%, even without any further operating leverage.

While I believe that the income statement captures the company's value, it's also essential to examine the balance sheet strategy. Eurosnack currently has a net debt of 3.14 PLN million, which is roughly 0.5x EBITDA. However, the company also leases its production facilities and machinery, which is not reflected adequately on the balance sheet. Nevertheless, the management provides detailed information on these leases in the annual reports, including lease terms for even the SKODA company cars. The total value of these leases is around 15 PLN million. While this lease strategy introduces additional risk, it also enables the company to operate with minimal capital and expand rapidly. If Eurosnack were to outsource its production, it could potentially compromise product quality, which is a crucial aspect of the company's strategy. Therefore, I believe this lease strategy is justified.

Based on the information provided, the current number of shares outstanding for Eurosnack is 35,519,041. However, in 2019, the sales director was granted a substantial compensation package in the form of options to purchase 5 million shares at a strike price of approximately 0.3. These options are currently deep in the money, and it's expected that all of them will be exercised. One million options were exercised in 2022, leaving 4 million still outstanding. As a result, the total diluted shares outstanding for Eurosnack is around 40 million. Using this figure, we can estimate a total diluted market capitalization of 68 PLN million. Additionally, factoring in the net debt and operating leases, we can estimate a total enterprise value of 86 PLN million.

Based on the company's revenue of PLN 12 million in December 2022, it is assumed that the company will achieve revenues of around PLN 150 million for 2023, as the company has never earned less than the run rate December earnings for the next year. Assuming an operating margin of 6-8%, the estimated profit for 2023 is between PLN 9 million to PLN 12 million.

Using the current enterprise value of PLN 86 million, we can calculate the following metrics for the company:

TEV/revenues = 0.57

PE ratio = 7.6 - 5.66

TEV/earnings = 9.5 - 7.1

Polish retail landscape, customers/partners

For those who are not familiar with the Polish retail landscape, it's important to note that Eurosnack mainly sells its products to Polish retailers, with some of them being very large customers. To provide a quick overview of the market, I've put together a table of some of the largest players, along with my own observations on whether or not I believe Eurosnack products are sold at their stores.

Looking at the table, we can observe some interesting trends. Firstly, Biedronka is clearly the dominant player and the largest chain, owning the discount market. This company is owned by Jeronimo Martins, a publicly traded Portuguese company. While Biedronka's scale is impressive, it also means that any potential deal with them would be a massive opportunity for Eurosnack. Furthermore there is plenty of room for growth by signing on other retailers.

Secondly, Eurocash, Carrefour and Dino are some of the next biggest players in the market, and are also customers of Eurosnack. While this represents a significant customer concentration risk, it also presents opportunities for Eurosnack to further develop their relationship with these companies. I suspect Carrefour and Dino are the two biggest customers and that Eurocash only distributed Eurosnack products to a limited number of franchises.

Carrefour mainly operates larger format stores compared to the smaller format common in Poland. Eurosnack supplies Carrefour with the largest assortment of its private label chips in Poland. However, Carrefour does not currently carry any of Eurosnack's own brands, which represents a possible avenue for growth. The current relationship is likely relatively stable due to the fact that Eurosnack produces a wide range of chips for Carrefour. If Carrefour were to switch suppliers, it would mean slightly changing the look and taste of a wide range of crisps, which is generally a bad strategy in the consumer products industry that is mainly driven by habit.

Moreover, most of the Eurosnack products currently sold at Carrefour carry the Gluten-free certification, and data from the celiac society in Poland indicates that Eurosnack is the only chips producer of scale carrying this certification currently. This presents a significant barrier to entry for other producers looking to compete with Eurosnack for the private label brand they currently sell at Carrefour, as they would also have to go through a process of adapting their facilities to apply for the certification. (gluten is sometimes used in flavor agents; this would mean changing again the flavor of many products.)

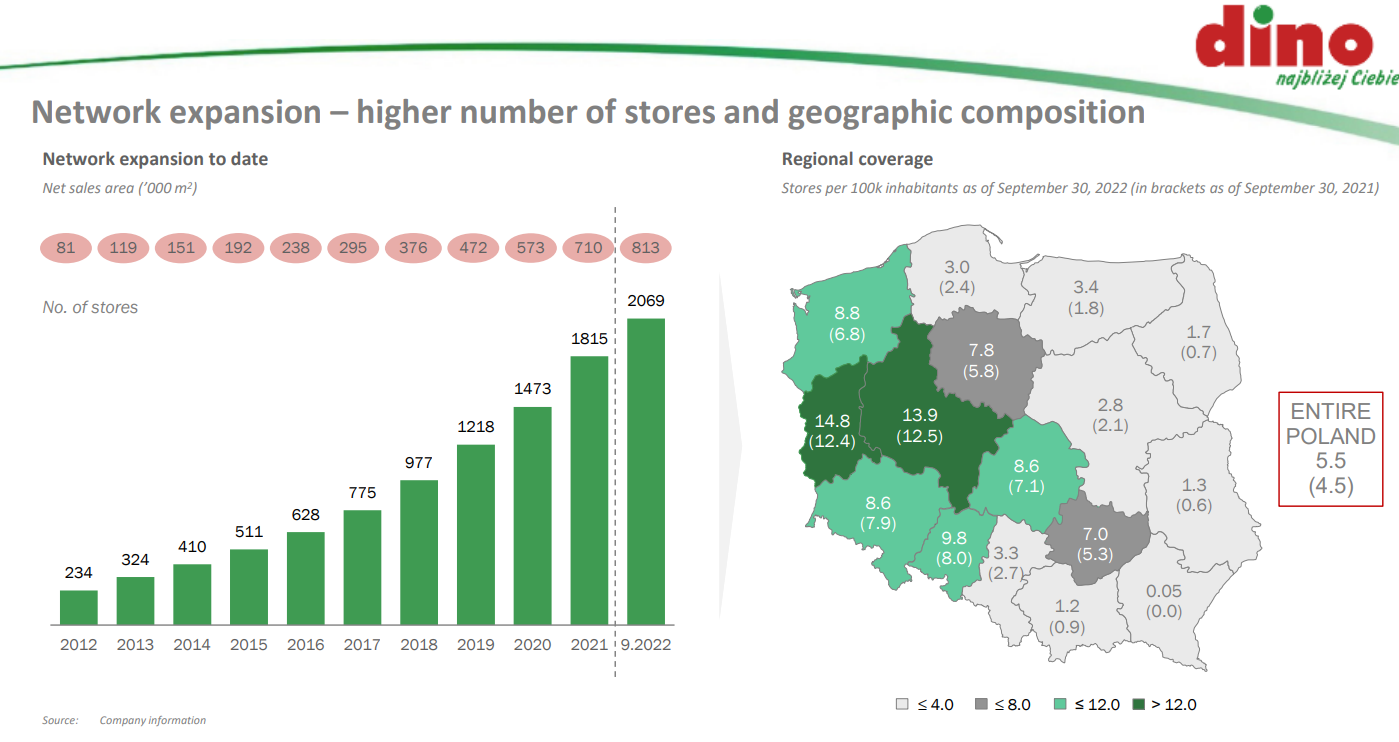

Eurosnack may consider Dino Polska as a more significant customer as it is the fastest-growing retailer in Poland. Dino Polska is a publicly traded company and an attractive stock on its own. SVN-capital has provided a comprehensive analysis of the company. Since 2011, Dino Polska has aggressively expanded its store bases, achieving a remarkable 30% compound annual growth rate. This is particularly impressive since the company purchases its land and owns its shops, avoiding leases altogether. The CEO, who is the majority shareholder, appears to be an excellent leader. Dino Polska primarily targets rural villages, where it competes with only one or two other stores.

According to the table above, Dino Polska still has ample growth potential. The company currently operates mainly in the western part of Poland and has the opportunity to expand towards the east while also increasing its presence in the west. Dino Polska aims to maintain a growth rate of 20% for the foreseeable future.

This expansion could prove advantageous for Eurosnack, as their products would be sold in more Dino Polska stores, providing more shelf space for Eurosnack's products. However, it's important to note that Dino Polska's increased scale could give them stronger bargaining power. Similar to Carrefour, it's unclear how strong the relationship between Dino Polska and Eurosnack is, and it's difficult to predict what it would take for Dino Polska to stop selling Eurosnack's products. However, it's unlikely that Dino Polska would sever ties with Eurosnack without serious harm to the relationship, as it would mean replacing several products that customers have come to expect from the stores.

Management & major shareholders, great alignment or great risk?

The current shareholder structure of Eurosnack is dominated by three major shareholders.

41.28% New Gym SA (Bogdan Małachwiej)

34.75% Marcin Kloocinski & s Private Investors Sp. z o. o

14.99% Tomasz Wlazlo

Eurosnack is predominantly owned by three major shareholders, with insiders holding around 91% of the company's shares. This ownership structure surpasses the threshold required delisting in Poland, which is set at 90%, but not for a squeeze out which requires 95% ownership. The company's free float is limited, accounting for only 9% or just 5.4 PLN million (equivalent to 1.21 million USD). As a result, Eurosnack, which is currently listed on the minor exchange in Poland (New Connect), cannot uplist to the Warsaw Stock Exchange (WSE), as the minimum free float requirement for the WSE is 25%.

Given the concentration of ownership among a small group of shareholders and the risk of a delisting or squeeze-out, it is necessary to evaluate these risks.

It is worth noting that both New Gym SA and Marcin Kloocinski have been shareholders of Eurosnack since its IPO in 2010. Bogdan personally owned 10% in 2011, and Marcin owned around 5%. Since then, both shareholders have increased their stakes by purchasing shares from other major shareholders and participating in capital raises. This demonstrates their long-term commitment to the company and their interest in its prospects.

New Gym is controlled by Bogdan Malachwiej, a Polish businessman with stakes in multiple private businesses. It's possible that he may not prioritize the public status of Eurosnack. Two representatives from New Gym, Katarzyna Borkowska and Wojciech Wesoly, are also on the board of Eurosnack.

Marcin Kloocinski is another Polish businessman who manages an investment vehicle called Private Investors Sp. z o. o. He owns many publicly traded and private companies in Poland, including shares in Eurosnack both privately and through Private Investors Sp. He currently serves as the president of Eurosnack's board and also holds the position of vice-president of the board at PlastPack Company SA, a company previously associated with Katarzyna Borkowska, the other board member.

The third shareholder, Tomasz Wlazlo stands out as the vice-chairman of the management board and the company's sales director, who has been with the company since 2012 and became a major shareholder in 2020. With a large stock option package, he seems to be committed to staying with the company for the long term. Interestingly, the president of the management board, Andrzej Krakówka, has never owned any shares since he joined the company in 2016. The company has fared very well with Andrezej and Tomasz at the helm in the last 6 years with revenue growing at a pace of 30% per year.

So do I believe these three shareholders want to take the company private? Both New Gym and Marcin Klopocinski are not pure public market investors so they are not prohibited from owning private companies. However, I have found no proof or indication of them owning any private companies together. Although New Gym does seem to have some connection to PlastPack SA, the other company Marcin Kloocinski chairs, through Katarzyna Borkowska the board representative of New Gym. She had a role in the investment committee of PlatPack from 2015 to 2016. Then we get to the third shareholder Tomasz Wlazlo, his stock in Eurosnack seems to be his only business venture. I estimate Tomasz Wlazlo to be around 55 so if he would want to retire in about 10 years time he would greatly benefit from eurosnack still being public.

There are other factors which point at them not wanting to take the company private, mainly the dividend paid over the last two years. The company paid out 50% of the net profit out as a dividend in 2020 and 2021. If the shareholder would want to take the company private it seems unlikely they would take a shareholder friendly action in the form of capital returns. If they had planned to take the company private it would have been more logical to add the profit to the surplus and not draw any attention with a dividend. They could then take the company private and only pay out the surplus once the company is private.

Speculation arises as to whether these three shareholders intend to take the company private. While New Gym and Marcin Klopocinski, the other major shareholders, are not prohibited from owning private companies, there is no indication that they own any private companies together. Furthermore, Tomasz Wlazlo's stock in Eurosnack seems to be his only business venture, and as he is estimated to be around 55 years old, he may benefit from Eurosnack remaining public for his retirement in about 10 years.

Other factors suggest that these shareholders may not want to take the company private. Eurosnack has paid out 50% of its net profit as a dividend in both 2020 and 2021, indicating a shareholder-friendly action in the form of capital returns. If the shareholders planned to take the company private, it would be more logical to add the profit to the surplus and not draw attention with a dividend.

To summarize, I hold the belief that the significant shareholders are dedicated to the company for the long haul. While the possibility of a delisting or squeeze out cannot be entirely discounted, there are signs that this is not presently on the table. Additionally, I have observed that the management team has exhibited commendable proficiency over the past six years, which bodes well for the company's prospects going forward.

Valuation

It thinks companies should be clearly cheap when buying them and investors should not need to excel to show the undervaluation of a company. Given that Eurosnack has compounded it revenue at a 40% rate and grew 50% last year it is clear that it current valuation for 2023 of is very cheap:

TEV/revenues = 0.57

PE ratio = 7.6 - 5.66

TEV/earnings = 9.5 - 7.1

However, Eurosnack stock is so cheap that I think some excel thought experiments are warranted to illustrate just how cheap this stock actually is. Let's start with a downside scenario, the stock has very few hard assets and trades above book so we can not claim we are buying a net net here. However packaged consumer goods is a great business so this should never be our down side case. I think the most realistic down side case one ought to think about is what happens if the stock loses its biggest customer. We know the largest customer is less than 30% of sales, this sounds large but if we consider that Eurosnack has been growing revenues at north of 30% this means losing out on what is one year of growth not direct bankruptcy.

I consider three situations with different assumptions to illustrate just how cheap the company is at the current enterprise value of 80 PLN million. All situations assume 150 PLN million in revenue for 2023, as stated earlier this comes from the December 2022 run rate earnings.

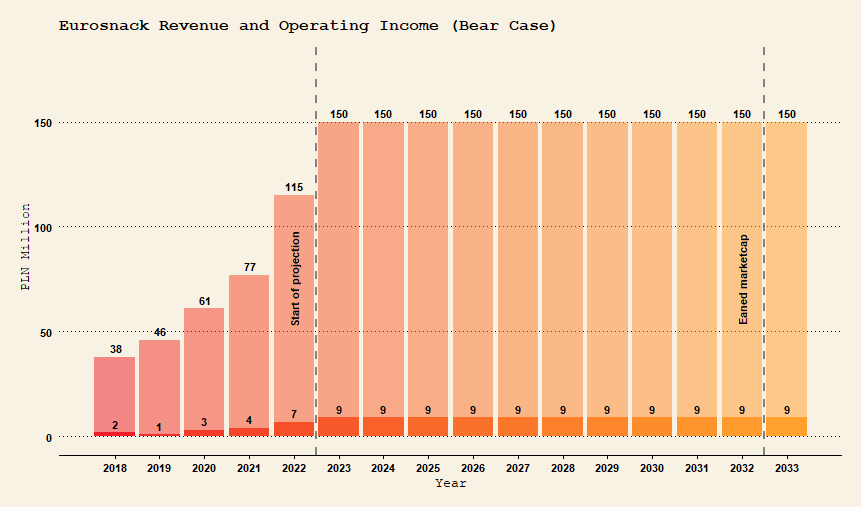

Thought experiment 1. the bear case

As stated above the real bear-case would materialize when one of the major customers stops its relation with Eurosnack. However, the impact of such an action would really depend on when this relationship ended. Instead I use the following assumptions:

No growth after 2023

6% operating margin

Exit multiple of 9x earnings

I believe these assumptions to be quite conservative given the company's explosive growth over recent years. The 6% operating margin is also conservative given that the current gross margin is so compressed. The exit multiple is low for a company with 50%+ margins in my opinion even with no growth.

Graph 6 above illustrates what the financial of the company would look like under such assumptions. The company would earn its current enterprise value by year end 2032. If we apply the 9x earning multiple year end 2033 we would have an exit value of 81 PLN million and the company would have earned 99 PLN million in profit of those 11 years. For a terminal value of 180 PLN million. At an 8% discount rate that would give us the current valuation. So the current valuation could be justified even with no future growth and permanently compressed margins. Giving us some downside protection.

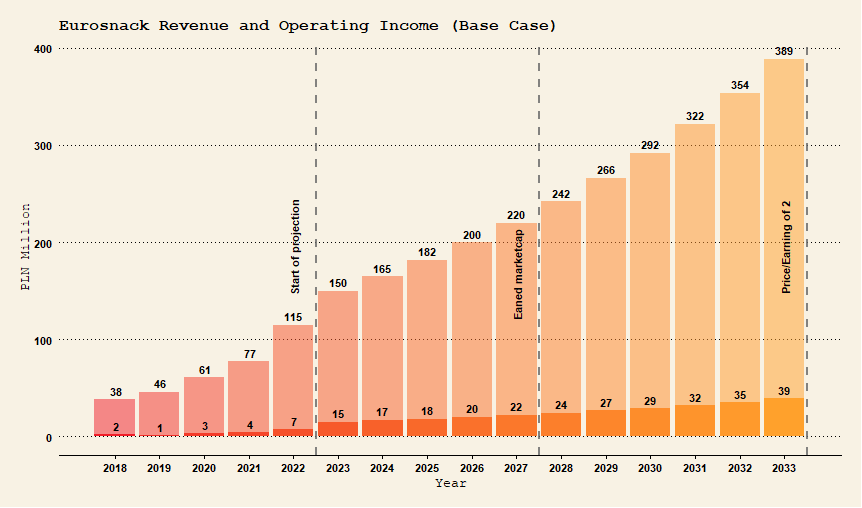

Thought experiment 2. the base case

In the base case I use the following assumptions

10% growth rate

10% operating margin

Exit multiple of 15

These are daunting assumptions for most companies but considering Eurosnack is still very small and has grown revenues at 40% over the last 8 years. And grew 50% in 2022 and will probably grow 50% again in 2023. These assumptions are relatively mild for eurosnack. Similarly the 10% operating margin seems very achievable. Given that the company would have had a 12% operating margin this year if it was not for input inflation.

As graph 7 shows above if the company only executes moderately well compared to the recent past it could already earn its current total enterprise value by year end 2027 derisking the stock in 5 years. The stock would also have a TEV/earnings ratio of between 4 to 5 year end 2023. So it is very very cheap. The stock would earn 297 PLN million over 11 years, if we use the exit multiple of 15x earning we get the value of 583 PLN million. Add them together and we get 862 PLN million (or 10x over these 11 years). Use whatever discount rate you like and assumptions on how much earnings need to be reinvested but this stock is cheap.

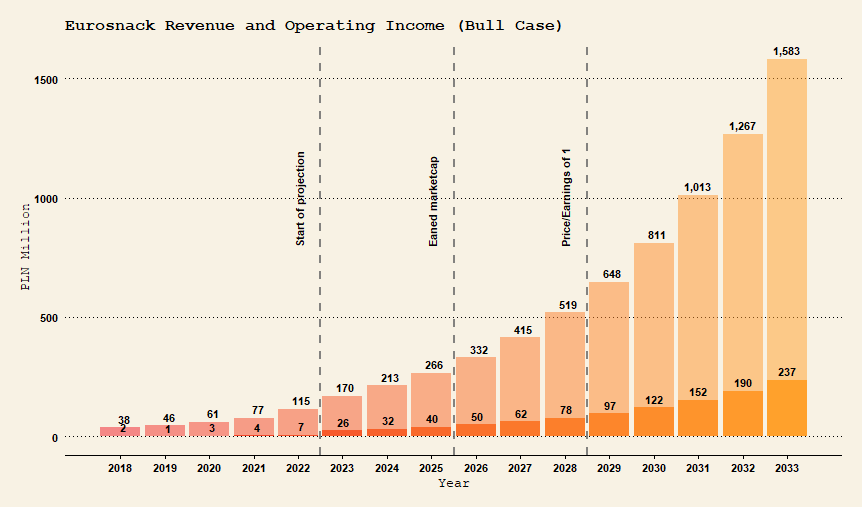

Thought experiment 3. the bull case

In the bull case I assume the management hits it out of the park and that the future is not much worse then the recent past. I use the following assumptions:

25% growth rate

15% operating margin

Exit multiple of 20x earnings

Even these assumptions do not seem that extreme given the company's recent performance but growing a company for 25% year in year out is really really hard. The 15% operating margins are at the upper end of what I consider possible for a fast moving consumer good company. The highest quality food companies seem to be around this level.

Lotus Bakeries: 16%

Pepsi co: 16%

Nestle: 15%

Unilever 16%

Coca cola: 22%.

As graph 8 shows above, under these assumptions the company is hyper underpriced. The company would earn the current enterprise value in 3 years, de-risking the investment. It would also be a P/E of 1 compared to the current market cap year end 2028. The company would have earned 1085 PLN million by year end 2033 or more then 10x the current market cap. If we exit the position at a 20x earnings multiple we get 5937 PLN million as an exit value. Adding these two together we get a total value of 7023 PLN million. Or a near 100 bagger. Again this is not at all the future I am currently expecting from this business, but it is important to realize how valuable this company could be if management keeps executing. This is not some quick double and sell.

Final valuation

Once we are done with the thought experiments, what do I actually think it is worth? In all honesty I have no clue. However, I believe you could go to the middle of the Baltic Sea and put up the whole company for sale and one of the giant food companies would probably swim there to pay you a multiple of 3 times revenue. So if we use that in 2023 earning 150 PLN million we get to a total value of 450 PLN million or 5 times the current value. However in reality I just plan to own the stock and watch it execute and adjust my price based on that. I do think it is clear that the company is cheap at current prices.

Catalyst:

-Value

-Continued growth

Risks:

-Customer concentration

-Take private

Nice find!

Well done, Sir.