Prax DCU's a Gift for my British Readers.

Thanks to the Unique Mind of a Value Investor Wannabe

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

This is a short write-up of an investment idea that I believe is an safe 50% gain within 24 months with limited downside, purely because it is so overlooked and hard to trade. I would have bought in myself, but I couldn’t find a suitable broker for an EU citizen like myself to trade this instrument, as this instrument trades at a weird exchange called JP Jenkins. However, if you are domiciled in the UK, it should be relatively easy to trade. Given that country where I have the most followers is the UK (thank you

), consider this my little gift to the people of Great Britain. Let’s dive in.

Background

During an event I hosted for small-cap investors in the Benelux, one investor (Value investor wannabe @Sjoerds78 on X) told me about a highly undervalued instrument related to Kistos. This was after I had given my presentation on the stock, which also formed the basis of my previous article. The instrument is currently trading at around 1.5-2p and is expected to return roughly 3p in cash by March 2027 in four installments leading to an excellent IRR.

The special instrument he pitched me on was Prax DCUs1 (Deferred Consideration Units). These DCUs exist because Prax acquired the assets of Hurricane Energy. As part of this deal, all Hurricane Energy shareholders received DCUs with the following basic terms2:

Prax Exploration & Production PLC acquired Hurricane Energy plc in June 2023. Hurricane shareholders received a Deferred Consideration Unit (DCU) per share, granting 17.5% of net revenues until 31 Dec 2026, capped at 6.48 pence per DCU. Payments are biannual, 90 days after each period ends.

Payouts So Far

Receiving 17.5% of the revenue from Hurricane Energy’s assets alone is already substantial, and the DCUs have already made three payments:

September 30, 2023 (for March 30 – June 30, 2023): 0.309p per DCU

March 29, 2024 (for July 1 – December 31, 2023): 0.617p per DCU

September 30, 2024 (for January 1 – June 30, 2024): 0.756p per DCU

And one projected payment, you re not eligible for anymore if you buy the DCU’s now:

March 30, 2025 (for July 1 - December 31, 20243): 0.560p per DCU (projected)

With these four payments, the maximum remaining payout for new buyers before July 30, 2025 is 4.238p4 over the next four half-year periods. Based on past payouts and production guidance, it does not seem ambitious to say that these DCUs will pay significantly more than 2p.

The Real Upside: Additional Acquisitions

The most exciting aspect of these DCUs is that they are not only tied to revenue from Hurricane Energy's assets but also to any other acquisitions made via Hurricane (now renamed Prax Upstream)5.

And here’s the kicker: Prax recently acquired Total’s stake in the West of Shetland assets6, which it shares with Kistos. This doubles the barrels of oil equivalent (BOE) that Prax Upstream will produce. The deal is expected to close in Q1 2025.

If we factor in the additional revenue from this acquisition, the DCUs look very likely to pay out around 3p, making for an excellent IRR.

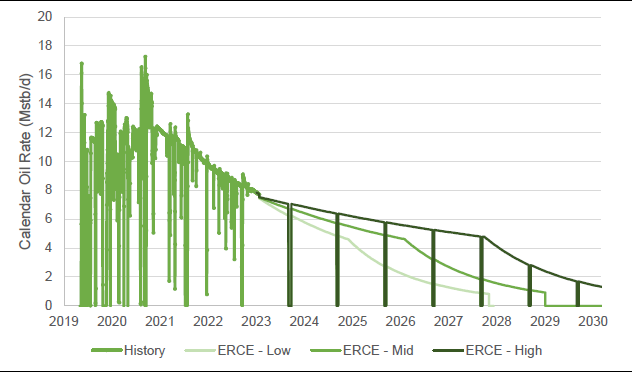

The underlying assets

The main producing asset Prax acquired from Hurricane is the Lancaster field, which produced roughly 8,000 BOE/day (HY 2024). This is in line with an independent study that provided the following production forecasts7:

Additionally, Kistos provided production forecasts for the UK assets that Prax acquired from Total8. Since Total owned double Kistos' stake, we double these estimates:

Total’s production adds another 7,500 BOE/day, which is 90% gas.

Natural declines in production are expected, as shown below..

Combining both production targets, the DCUs appear very likely to pay out around 3p, for a 50% gain in 24 months. As shown in my calculation below:

I think the assumptions in this scenario are relatively conservative, as they assume the currently projected decline of the field without any optimization or infill drilling, which seems unlikely.

Downside Risk

Of course, oil and gas prices can fluctuate. To illustrate how low the downside is, here’s a scenario where the DCUs only pay out the current price of 2p:

While there are countless combinations of oil and gas prices that could lead to a total payout of 2p, note that this scenario assumes:

Oil prices dropping by ~40%

Gas prices dropping by ~40%

This decline persists on average over the entire period

I think the combination of these 3 assumption or worse is very unlikely, limiting your down side.

Risks

Oil & Gas Price Declines – Since payouts are 100% determined by revenue from oil & gas extraction, price volatility is a key risk.

Operational Issues – The revenue is derived from a relatively small number of wells, so any significant issues could reduce production forecasts substantially.

Total Deal – The Total deal has not yet received regulatory approval, but given its small size, this is unlikely to be an issue. I assume that, once approved, it will be applied retroactively from January 1, 2025, as is standard in oil & gas transactions, though I have not found explicit confirmation of this.

Where to Buy

As I mentioned at the start, this is one of the most obvious investment ideas I’ve come across. However, I cannot find a broker that serves EU clients at reasonable conditions unless they have much larger funds.

Most JP Jenkins brokers that accept EU clients operate more like wealth management boutiques.

However, if you:

Are an EU investor willing to open an account with a boutique British broker, or

A UK investor, then JP Jenkins has a full list of brokers that trade on this exchange9.

Final Thoughts

For UK investors, this opportunity looks incredibly attractive. The structure of the DCUs offers a compelling risk-reward ratio, especially given the upcoming acquisition’s impact on revenue. While risks exist, the downside seems well-protected unless there is a major crash in oil and gas prices.

I hope this idea provides value—happy investing!

There are DCU I & DCU II, both are relatively similar with the exception of how they receive their payment. DCU II receives cash and DCU I receive C loan notes, redeemable in cash six months after issuance. You could research if one of the two options is more tax efficient for you.

The ex-dividend date for this payment was 31th of December 2024 so current buyer will not receive it. See “What date do I have to be on the DCU register to receive a DCU payment?” [link]

Max payment of 6.48p - 0.309p - 0.617p - 0.756p -0.560= 4.238p

"Since payouts are 100% determined by revenue from oil & gas extraction, price volatility is a key risk."

Revenue is price x volume.

Could volume be depressed by (scheduled) maintenance?

Ie, do maintenance within last few months of eligible period instead in the year thereafter