The Darkest Hour is Just Before the Dawn.

Why I still believe in Andrew

Warning: The following article is for informational purposes only and should not be considered as investment advice. The author is not a registered financial advisor and does not provide investment recommendations. Any investment decisions you make should be based on your own research and analysis.

Additionally, please be aware that the author may have a financial interest in the securities discussed in this article. The author reserves the right to buy or sell any security mentioned in this article at any time, without prior notice. Therefore, the information presented in this article should not be considered as a solicitation to buy or sell any security. Please consult with a registered financial advisor before making any investment decisions.

Andrew Austin the next Outsider

Austin had previously led Rockrose, an oil and gas investment vehicle that achieved an impressive 42x return in just 4.5 years.

In my last article, I mentioned that Kistos was a fascinating company with a healthy cash position and an “outsider” style chairman, but had hit a 52-week low due to unfortunate circumstances. This is still true, but since then, the stock has dropped by another 60%. A series of challenges, including the normalization of gas prices and some operational difficulties in its Dutch operations, even prompted the auditor to add a note to the annual report expressing concerns about Kistos as a going concern. With many retail investors abandoning the once wildly popular stock, this truly seems like Kistos' darkest hour.

But as the saying goes:

“The Darkest Hour is Just Before the Dawn.”

I believe that Kistos is significantly undervalued, at $122m market cap, due to investors overlooking a stream of high visibility cash flows that Kistos will receive in the coming years as well as a host of other more complex value accreditive events on the horizon. Below I’ve create a timeline of events for Kistos that illustrate the absurdity of the current market valuation and illustrate the the dawn should be near, leading to a significant rerating by the market. In the remainder of this article, I will walk through this timeline in detail creating clarity about some of Kistos’ more complex and overlooked elements.

How did we got here?

Let’s start by looking back to understand why Kistos has sunk so deeply. When Kistos acquired Mime, the transaction involved paying $1, issuing warrants at a price three times the current stock price, assuming $225 million in debt, and issuing a convertible bond of $45 million, payable by Q2 2025, contingent on offloading a certain amount of oil from the Jotun FPSO by that time [1]. In addition to this, Kistos used cash to buy back the last remaining Dutch bonds, which had restrictive covenants on capital redistributions [2]. They also purchased gas storage assets in the UK from EDF Energy for $30 million [3]. This left Kistos with “only” $194 million in cash on the balance sheet at the end of FY 2023.

However, due to past issues, UK auditors are cautious (Andrew’s words were that they are "scared of their own ghosts"[4]). This led Kistos' auditor to include a going concern note in the company’s annual report, warning about possible adverse scenarios where Kistos could breach the minimum liquidity threshold of $10 million, which is a covenant tied to the bonds assumed in the Mime acquisition [5].

This warning seems completely ridiculous, given the $194 million in cash on the balance sheet, and it is. However, there are some important details about this cash balance that need clarification. By the end of 2023, Kistos had significant current taxes payable, which the cash would be needed for. Additionally, the company had committed to substantial capex spending in Norway for 2024, which would further deplete the cash balance.

Even taking all of this into account, it would still be absurd to think that Kistos could breach the $10 million minimum cash covenant, considering its current cash flow profile and the various ways it could tap working capital if necessary. So, yes, Andrew was right—the auditors were "scared of their own ghosts".

This note by the auditor, combined with below-expectation performance from the Dutch Q10a field, uncertainty around the UK tax regime, a reduction in gas prices, and overall investor malaise, led to Kistos' share price falling from about 280p to 112p, at the current time of writing.

This brings us to the present, with the recently released H1 2024 results from Kistos. These results were largely similar to the FY 2023 report, still containing the going concern note. Capex and tax payments had indeed eaten into the cash pile, which was now down to $70 million. With the face carrying value of the bonds on the balance sheet at $236 million and a market cap of $122 million, this results in a Total Enterprise Value (TEV) of $286 million [6].

Q4 2024

First Norwegian cash back

The first major positive event on our timeline is expected to occur in December of this year, when Kistos will receive a cashback from the Norwegian government amounting to $84 million[6], for capex loss generate by Mime in 2023. Norway has a “hard” tax credit regime, where companies can receive tax losses generated by investments, even if they don’t owe taxes. This cashback is received in the final month of the year following the investment [7]. This cashback increase cash on balance sheet to $154.

Production 2024

Of course, Kistos is still producing in all three countries where it operates. I assume that for the remainder of this year, the capex spent in Norway and the cash flow from the producing assets will roughly cancel each other out, leading to no significant net cash inflows or outflows. With $154 million in cash on the balance sheet, the TEV will be $202 million.

Write-down of the Hybrid bond

Another important event will occur in Q4 2024, when Kistos will likely be allowed to write down the $45 million hybrid bond issued as part of the Mime deal. To protect itself from further delays and cost overruns related to the Balder X project, Kistos structured this $45 million hybrid bond such that it would not be payable if 500,000 barrels (gross) weren't lifted from the Jotun FPSO before May 31, 2025 [1]. On August 21, the operator of the Balder X project, Var, announced that the sail-away would be delayed. As a result, Kistos is confident that the $45 million bond will be canceled in full. While this delay does lead to an additional $40 million in capex (net to Kistos), due to Norway’s tax regime, the after-tax cost will be just $8.8 million, most of which is expected in 2025 [8].

Kistos had a $15 million provision for this hybrid bond on its Q2 balance sheet [6], which I believe will be written down to close to zero by Q4 2024. This would reduce the TEV by another $15 million, bringing it down to $187 million. I would also note that the value of canceling this bond is in my opinion significantly higher than the $15 million accounting gain, as the potential cash outflow would have been considerable compared to Kistos’s market cap and financial flexibility.

2025

Q10 Orion oil field FID

I believe the most important event for Kistos in 2025 will be the Final Investment Decision (FID) on its Orion oil field in the Netherlands. Many long-time Kistos shareholders have always seen this oil field as one of the major value drivers for the company. However, despite positive drilling results and flow tests in 2021 [9], it has taken a considerable amount of time for Kistos to develop the field. I now believe that the FID is only a matter of time. According to Andrew, the economics of the field are sound, and the delay is primarily due to finalizing the right export route [4].

The most likely export route is through the P15 platform, which Kistos already uses to export gas from the Q10a field. The platform’s costs are shared among a large group of users, making it critical for Kistos to understand the long-term throughput commitments from other parties. Andrew recently reported that all involved parties are finally aligned and sharing information openly [4]. Even if the P15 export route doesn’t work out, I still expect Kistos to move forward with developing the Q10 Orion field, given its better-than-expected flow test results and the fact that oil extracted from the Dutch North Sea is among the lowest-taxed barrels in the EU. Additionally, the Dutch government has already approved the oil field, a significant milestone that has largely gone unnoticed by investors [10]. As far as I know, this is the first new oil development greenlighted in the Netherlands in over a decade.

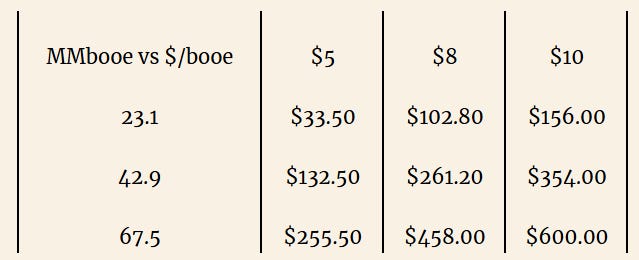

The FID on Q10 Orion would convert a significant amount of Kistos’s 2C resources to 2P reserves. The last independently verified estimates for net 2P reserves in the Orion oil field are as follows [11]:

Low: 23.1 MMboe

Mid: 42.9 MMboe

High: 67.5 MMboe

These are substantial amounts, and even in the low case, the reserves would roughly double Kistos’s current 2P reserves. It’s worth noting that when Kistos acquired this field as part of the Tulip deal, a contingent payment was agreed upon. Upon FID, a payment of USD 4.50 per barrel is triggered based on the net reserves at the time of sanction, capped at EUR 75 million ($82 million), payable upon first hydrocarbons [12]. Even in the low estimate case, the maximum contingent payment will be triggered.

Here’s a rough estimate of the potential value of the Orion oil field net to Kistos, based on reserves and the valuation of these reserves minus the max contingent payment:

Even in the most conservative estimate, the net value of Orion would represent approximately 40% of today’s market cap and 20% of my expected enterprise value by the start of 2025.After discussing my cash flow expectations at the end of 2025, I will also calculate Kistos’s 2P/EV ratio for the end of 2025 to show how incredibly cheap Kistos will look.

It should be noted that the Dutch government has approved a relatively small project for the Orion field [10]. With Kistos being allowed to lift 500 tons (~3,200 BOE) per day, hence, I would say that the valuation are more in the top left of the value table.

GLA Area New Operator

Before we reach the end of 2025, there are some important developments expected on the UK side of Kistos’s business, specifically in the Greater Laggan Area (GLA). The UK operations have been something of an "ugly duckling" for Kistos, as the shifting tax regime and an operator unwilling to sanction new drilling have left the GLA somewhat stranded.

However, there's a shift occurring in the GLA with Total selling its stake to PRAX [13]. This change means that some of the existing reserves, including Glendronach, will likely be sanctioned for development. Additionally, Shell has bought into the Victory Gas Field, located near the GLA, and has approved a single subsea tie-back to the Shetland Gas Plant [14] . The sanctioning of the Victory Gas Field by Shell and the arrival of a new operator in the GLA will likely extend the useful life of the Shetland Gas Plant. The plant’s minimum throughput determines the economic life of the entire area, which is crucial to Andrew Austin’s specialty: decommissioning liabilities.

Kistos currently carries significant decommissioning liabilities related to the GLA area on its balance sheet. I expect these liabilities to be significantly reduced as a result of extending the area’s economic life. Moreover, Andrew Austin has stated that Total did not fully comply with UK regulations regarding decommissioning liabilities and security posting. As part of the transaction between PRAX and Total, it has been indicated that these liabilities will be reduced, leading to more flexibility on Kistos’ Kistos’ balance sheet [4].

The Glendronach field, in which Kistos holds a 20% stake, was discovered in 2018 and initially thought to contain 175 million barrels of oil equivalent (MMboe). However, a 2019 appraisal well reduced those estimates by 40%, bringing the field's total to 105 MMboe. This means Kistos' share of the field is now approximately 20 MMboe.

Given that this is UK gas, which typically trades at a slight discount compared to Dutch TTF gas, and considering the shifting tax regime in the UK, it is reasonable to assume these barrels should be valued slightly lower by the market. Therefore, the lower end of BOE estimates seems more appropriate for this asset.

Jotun FSPO Sail Away

While the sail-away of the Jotun FPSO is highly visible and well understood, I still believe it will represent a huge milestone for Kistos, truly marking the dawn after the dark hours of 2024 and the going concern note. Once the Jotun FPSO is in place, production in Norway will see a significant uplift, moving Kistos into a profitable position there. Kistos has provided the following guidance on expected daily production levels for the coming years, assuming the Jotun FPSO sail-away in Q2 of 2025 [15]. These figures are based solely on currently sanctioned fields, excluding potential future developments like Q10 Orion, Glendronach, and Edradour West. This guidance also forms the basis for the cash flow calculations in this article.

It’s important to note that this production forecast only goes to 2028. However, the currently sanctioned wells for the Balder X project in Norway are expected to produce all the way until 2040. Therefore, I believe that once the Jotun FPSO is operational, investors will feel much more comfortable with Kistos, as it will have a longer production profile and significantly reduced risk of timing or capex overruns.

Another interesting development likely to occur is VAR’s expected sanctioning of a portion of the 2C resources Kistos acquired through the Mime deal. Kistos received 30 mmboe of 2C resources as part of this acquisition. Andrew has expressed confidence that VAR will begin commissioning a part of these resources once the FPSO is in place.

I agree with Andrew’s outlook. While I haven’t been inside the data rooms and can’t assess the exact potential of these 2C resources, VAR’s strong commitment and the incredible capex investment in the FPSO—now exceeding $4 billion—suggest they are highly confident in the Balder area’s prospects. VAR has already indicated that an investment decision for the next phase of resources, Balder Phase VI, will be made in the first half of 2025 [16].

This gives us another potential scenario for the value of these 2C resources, depending on their volume and the valuation investors place on them. However, it’s important to note that, although the development of these 2C resources is likely, their risk of being uneconomical is higher than that of the Orion Oil Field in the Netherlands. Norway does boast a remarkably high exploration success rate of 50%, which adds some confidence [17]. It’s also worth noting that VAR, the operator of these fields, currently trades at a ~10x EV to 2P ratio as of the time of writing.

Dutch Tax Liability

Kistos currently has a €45 million ($50 million) tax liability on its balance sheet, which it believes it does not need to pay. This liability relates to the windfall taxes for 2023, which apply only to entities that derive 75% or more of their earnings under Dutch GAAP from oil and gas production [6]. While Kistos’ Dutch subsidiary is indeed an oil and gas producer, due to the way the entity is structured in relation to its UK holding company, the Dutch subsidiary does not classify its profits as derived from oil and gas production under Dutch GAAP.

Kistos filed its tax return for 2022 in May 2024. If the Dutch government does not object to the way Kistos has filed its taxes by mid-2025, I believe the auditors will be compelled to give Kistos and its tax advisers credit for their position and derecognize the liability, resulting in a $50 million gain.

It seems to me that the market has given no credit to the potential removal of this liability, and once announced, it could result in a significant bump in Kistos' stock price. Additionally, if we consider Kistos’ current equity of $70 million and add the $50 million gain, this would bring equity up to $120 million. At such point, Kistos would be trading roughly at or below book value, which could attract additional bargain hunters.

Capital Allocation Share Buyback

Once the Jotun FPSO is operational, Kistos will no longer be committed to any significant capital expenditure (capex) and will have a more secure long-term production profile. The cash inflow from this production, combined with a strong balance sheet and the likely resolution of the Dutch tax liability, will place Kistos—and Andrew Austin, in particular—in an excellent position to begin deploying cash in ways that are most accretive to investors.

Assuming no attractive bargains appear in the North Sea, I expect Andrew to focus on two main strategies for using Kistos' cash.

First, I anticipate a tender offer to buy back 25% of the company's shares. During the last AGM, a buyback facility for up to 25% of the stock was approved[20]. Based on Andrew’s last interview[4] and my own analysis, it’s clear he believes Kistos’ stock is significantly undervalued. Given this, I expect him to fully utilize the buyback authorization. Due to the stock's limited liquidity, this is likely to take the form of a tender offer.

Since I strongly believe that Kistos is extremely undervalued, this tender offer will likely be highly value-accretive. Furthermore, even after completing the buyback, I expect Kistos to have ample cash remaining at the end of the year for other strategic uses.

Capital Allocation Bond Refinancing.

Second, I expect Kistos to reduce its net debt to a more manageable level. Although the company’s net debt is likely to be very small by this point, I don’t foresee Andrew eliminating it entirely. Instead, I expect him to reduce it to around $120 million, down from $200 million, and then refinance the remaining portion at lower interest rates.

In his previous bid for Serica, Andrew was clear that under the current tax regime, it makes sense to maintain some level of debt in the capital structure to optimize returns. This is especially true with a 75% tax on profits, which makes using debt highly advantageous. Even with a 10% interest rate—now more typical for oil and gas companies—the after-tax cost of debt for shareholders would be just 2.5%, which is lower than the central bank's interest rate.

In summary, by Q3 2025, Kistos will be in an ideal position to execute a value-accretive tender offer and optimize its capital structure, positioning the company—and its shareholders—for long-term success.

2025 cashback

By the end of 2025, Kistos will once again receive a tax rebate from the Norwegian government, along with generating a significant amount of operating cash flow after capex spending.

First, Kistos will recover 75% of its 2024 capex spend through Norway's tax rebate system. I estimate Kistos will spend $110 million on capex this year. This figure might be slightly high, but if that's the case, it would actually be a positive sign, as it would mean Kistos should have already shown positive cash flow in 2024. With 75% of $110 million equaling $82 million, this rebate would bring Kistos’ TEV down to around $120 million, potentially placing the company in a slight net cash position.

2025 Cash flow from Production & 2P (under) valuation

In addition, Kistos' production is expected to rise in 2025 while its capex drops. Based on my best “guesstimate,” this will add another $45 million in cash flow, bringing Kistos’ TEV down to approximately $75 million. This suggests that Kistos would be trading at a TEV/FCF ratio of 2x.

However, this multiple doesn’t account for the likely addition of significant 2P reserves from the Orion oil field and Balder Phase VI. Once we start factoring in these reserves, Kistos’ valuation becomes even more compelling.

The picture above illustrates just how undervalued Kistos will be by the end of 2025. Even without factoring in any upside from the Orion oil field or Balder VI reserves, the stock has a potential upside of 94% simply by trading at a TEV/2P ratio of 8, which is a very standard valuation multiple. If we include the low-case scenario for Orion, with a BOE of 8, the upside jumps to 185%, effectively tripling the stock’s value. As we move further right and down in the chart, the numbers become so favorable that further elaboration seems unnecessary.

2026

While I expect many significant events to occur in 2025, it’s important to recognize that some developments, particularly the sanctioning of reserves, may take longer than anticipated and could spill over into 2026.

2026 Cashback

For the purposes of this article, I assume that 2026 will be a relatively uneventful year, but one characterized by incredible cash flows. First, we know that Kistos will still have a healthy amount of capex spending in 2025. As a result, I expect the company to receive approximately $38 million in cash flow from tax rebates on its investments in Norway for that year. Given that Kistos is projected to be in a profitable position by mid-2025 and into early 2026, this cash flow will likely arrive much earlier than December 2026.

2026 Operating Cash Flow

More importantly, according to the guided production levels, Kistos is expected to have its peak production year in 2026 with very limited capex. I estimate this will generate roughly $75 million in cash flow. Together with the cash back from the Norwegian government, this would bring Kistos’ TEV down to approximately -$31 million. Therefore, if Kistos retains its current market cap and meets its production targets, it will likely achieve a net-net position by the end of 2026.

2027

Respect for the Gas Storage Business

By 2027, I expect investors to finally recognize the value and profitability of Kistos' recently acquired gas storage and trading business. This business was purchased from EDF Energy for £25 million, a bargain price given that the cushion gas stored in the facility was worth more than the acquisition cost [4]. Essentially, Kistos could liquidate the asset today and make a profit.

However, Andrew, whom I respect greatly, seems to believe that this business has significant long-term potential. We already know that the gas storage facility generated $4 million in profit this year, a solid return on the $30 million purchase price. And generation 1.8m in revenue in the 2 months before the half year report, from trading activities.

Additionally, Kistos has increased the storage capacity shortly after acquiring the asset and is studying plans to expand capacity by another 70%. Initially, the market was confused by Kistos' acquisition of this asset, unsure of how to properly value it.

However, after two years of profitability and with the capacity upgrades in place, I expect investors to start valuing this asset within Kistos' portfolio more appropriately. While trading is inherently volatile, we know that other bidders were willing to pay more for this asset , but couldn’t complete the purchase because the trading firm they worked for didn’t want to manage and operate the business. Kistos, however, has partnered with this team, which now handles the day-to-day trading operations.

Given these facts, and considering the planned upgrade, I conservatively estimate the business is worth around $40 million—modestly higher than the purchase price but reflective of its true potential.

2027 Operating Cash Flow

In 2027, I also expect Kistos to generate strong cash flow, with production guidance of around 8,000 boepd, most of which will come from oil production in Norway. Assuming moderate capex levels, I project Kistos will generate approximately $50 million in cash flow for the year. This would bring the company's TEV down to -$81 million.

2028

2028 is the last year for which we have production guidance, and while it's still a bit far off, there's one optional play that Kistos is likely to explore — the development of the M10 and M11 fields in the Netherlands.

M10/M11 Fields

Kistos initially lost the licenses for the M10 and M11 fields when the Dutch government decided not to extend them, preferring a party that would actively explore their economic potential. However, Kistos successfully appealed this decision and regained the licenses.

This, of course, means that Kistos will now need to demonstrate its intent to explore the economic viability of these fields. The process is likely to be challenging and lengthy, primarily because the fields are located near a Natura 2000 nature sanctuary. As such, I believe any Final Investment Decision (FID) regarding the M10 and M11 fields will likely come around 2028.

Kistos has already started engaging with the local community to address concerns, and early feedback from community meetings seems positive, according to local news coverage [21]. Additionally, Kistos has published detailed information on what potential development might look like [22]. The current 2C resource estimates for the M10/M11 fields are as follows:

Low Case: 12.0 MMboe

Mid Case: 35.9 MMboe

High Case: 45.0 MMboe

It's worth noting that these fields were also part of the Tulip acquisition and come with a contingent payment upon first hydrocarbons. In this case, the payment is set at $3.5/booe, capped at EUR 75 million ($82 million). The graph below illustrates the potential value of the field:

As shown, even the mid-case scenario for the M10/M11 fields suggests that this single asset could be worth as much if not more than Kistos' current market cap.

Cash flow from operation 2028

In 2028 I expect around $40m of cash flow from the 5k of guide barrels. Bringing the TEV down to -$120m. Hence Based on current guided production and cashback I believe Kistos will have double the current market cap in net-cash by the end of 2028.

Beyond 2028

Production

While Kistos has not provided production guidance beyond 2028, that doesn't mean production will cease. The currently sanctioned Balder field in Norway is expected to continue producing into the 2040s, providing substantial cash flow well past 2028. It's reasonable to assume that Balder will generate around $25 million in cash flow annually for a significant period.

Additionally, as discussed throughout this article, several 2C developments, such as Orion, Balder VI, and M10/M11, are likely to come online, extending Kistos’ production timeline well beyond 2028 if any of these projects are sanctioned.

Liabilities

This extended production horizon is particularly important for understanding one area that hasn't been a primary focus so far—Kistos' $260 million in abandonment and decommissioning liabilities[6]. These liabilities break down as follows by my estimation:

Netherlands: The decommissioning of the Q10a field's wells and infrastructure, currently projected to occur in 5 to 8 years (estimated at $50 million).

UK: The group's share of the decommissioning of the Laggan, Tormore, Edradour, and Glenlivet wells, along with the Shetland gas plant, expected between 5 and 14 years (estimated at $100 million).

Norway: Decommissioning of the Balder and Ringhorn fields, planned for 25 years from the balance sheet date (estimated at $80 million).

UK Storage: Decommissioning of gas storage caverns and plant, projected for 20 years from now (estimated at $30 million).

While these liabilities are real, the timeline for addressing them is quite long, with the first decommissioning activities not expected to start until 2029. Moreover, several factors could push these dates even further into the future.

Netherlands: The Orion oil development will use the existing Q10a platform, extending its operational life by at least 15 years, which means that decommissioning will be delayed, and there could be additional infill drilling opportunities.

UK: With renewed activity in the Greater Laggan area (e.g., Shell's interest in the Victory gas field and Praxis developing other assets), the Shetland gas plant is likely to remain operational for much longer. This will likely push back decommissioning for the entire GLA area.

Norway: Although decommissioning provisions are already projected far into the future, any additional field developments could reduce Kistos’ surety deposit obligations to its partner, Var.

UK Storage: Kistos is actively re-brining additional caverns to increase capacity, indicating that the asset is here to stay. I don't expect this segment to be decommissioned in the foreseeable future.

As a result, while these liabilities exist on paper, I expect them to require minimal cash outlay in the near to medium term. This reduces their economic impact on Kistos and makes them less of a drag on the stock or my valuation.

There’s also another major liability to address: Kistos' $150 million in deferred tax liabilities. Like the decommissioning provisions, these deferred taxes do not represent an immediate cash outflow. These taxes can be used as form of float, as you can pay last years taxes, by not paying this year taxes directly. Furthermore, future accounting losses can significantly reduce these liabilities over time.

In conclusion, while Kistos does have substantial liabilities on its balance sheet, many of them are unlikely to impact the company in the near term, and ongoing production—both from sanctioned fields and future developments—should generate strong cash flows for years to come.

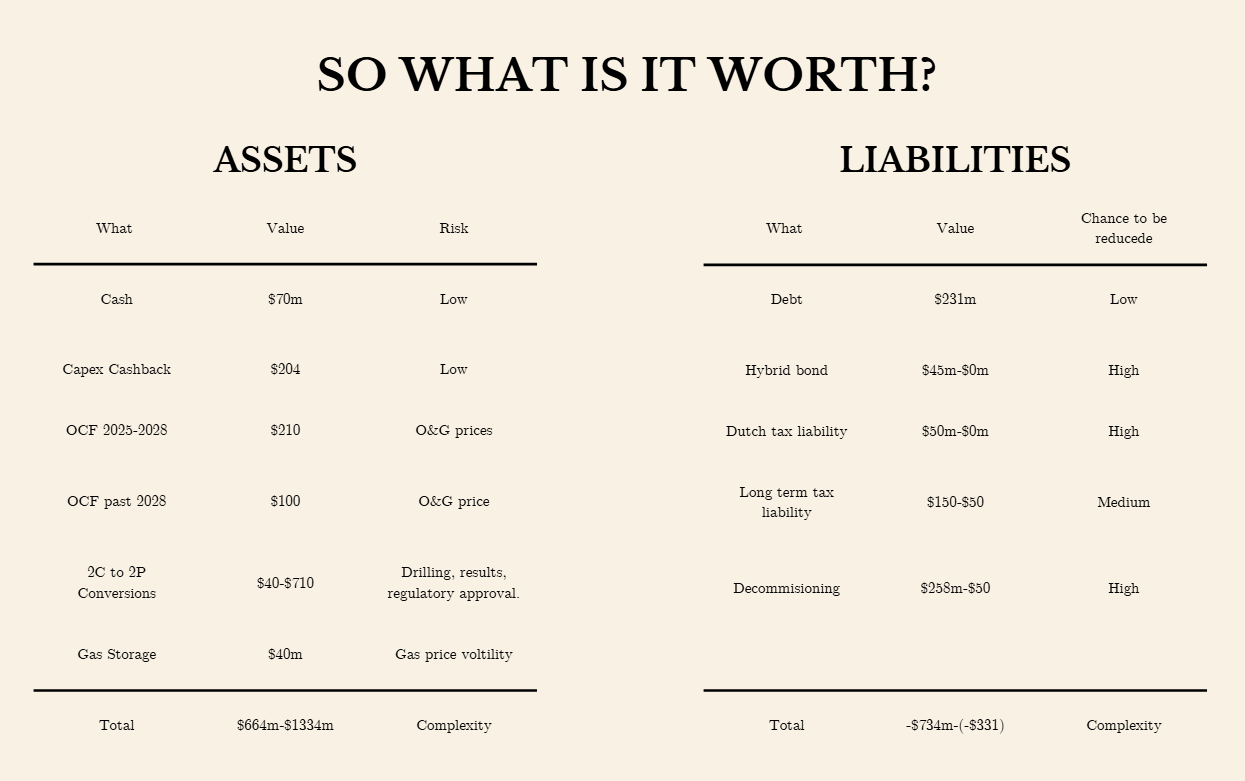

What is it worth?

Below I’ve compiled a list of all potential assets and liabilities, there are many moving pieces so it is hard to value. However I would note the huge time discrepancy between most of the large liabilities which are far in the future and most of the assets/cash flows which will be realized much sooner. Within this time delta I expect Andrew one of the best capital allocators I know to do wise thing with his and our cash.

Detailed Notes and sources

This section has links and notes with evidencing for the article to help you kick start you due diligence.

[1] Mime deal announcement and terms. [link]

[2] Announcement of the redemption of the remaining €76,832,000 of restrictive Dutch bonds. [Link]

[3] Announcement of the purchase of the UK gas storages assets for £25m ($30). [Link]

[4] Recent interview on Core Finance with Andrew Austin. [Link]

[5] For a the details on the going concern note and the assumption used for this assessment by the auditor see the Kistos annual report and account FY 2023. Note 1.2 on page 58 [Link].

[6] Kistos interim result 2024. [Link]

For more details on the face value and carrying amount of the bonds see note 5.1 on page 23.

For more details on the tax receivable for December 2024 see note 6.2.1 on page 23.

For more information on the Dutch windfall tax and why Kistos believes it does not have to pay it see note 6.3 on page 24.

For more information on the Decommissioning liabilities see not 2.5 on page 20

[7] Page on Norwegian oil and gas taxation system. See specifically the paragraphs on “Neutral tax system”. [Link]

[8] Balder X project update [Link]

[9] 2021 operational update on the drilling test of the Orion/Vlieland oil field. [Link]

[10] Approval of “mijnbouw” vergunning for the Orion Oil field by the Dutch government. [Link]

[11] Interim results presentation 14th September 2021. [Link]

For detailed information on the Orion/Vlieland oil field see slide 8

For reserve estimation of M10/M11 see slide 9

[12] Acquisition of Tulip Oil Netherlands B.V. [Link]

For detailed information on the contingent payment see 12. Principal terms of the Acquisition

[13] Energy voice “French Total sells West of Shetland assets to PRAX”. [Link]

[14] Development Approval for Victory Gas Field. [Link]

[15] 2024 Interim Results Presentation. [Link]

For production guidance see slide 3.

[16] Var Energy balder X update, including plans for Balder phase VI. [Link]

[17] Article by norskpetroleum.no on exploration activity on the Norwegian Continental Shelve. [Link]

[18] Article in regional news paper about meeting with local about Kistos’s plan for the M10 & M11 fields. [Link]

[19] Kistos information page plans for M10 & M11. [Link]

[20] Result of AGM Kistos 2023. [Link]

for the buyback see resolution 12.

[21] Local News on meeting with local about M10/M11 fields [Link]

[22] Kistos project page for M10/M11 [Link]

Thanks for the write-up. When a CEO dismisses a 'going concern'-note, I think investors would be wise to be sceptical. You can be sure that the CEO did everything in his powers to NOT have a 'going concern'-note, and as the auditor is paid by said CEO, you can be reasonably sure that they'll go very far so as not to include said note. I have no idea whether this works or not, but I think that's a big red flag and enough to keep me away either way. Best of luck!

Andrew also founded and led iGas before RRE. In case you want to use his background, it would be fair to look at the whole picture.